Portugal’s first property sale in cryptocurrency might have looked unremarkable, but it didn’t feel that way to those who had been working for nearly a year to make it happen.

On May 4, in an office in the northern city of Braga, two men pulled up chairs in front of Apple laptops. João Marques, the seller, passed a crypto wallet address to the buyer, who made a transfer and became the new owner of an apartment in the city worth €110,000 — just under three bitcoin at the time. The president of the Portuguese chamber of notaries, Jorge Silva, watched on — as did Carlos Santos, chief technology officer at the Portuguese real estate company Zome, which brokered the sale.

The whole process took just a few minutes but it was the culmination of many months of discussions between Portuguese tax, financial and notary authorities to agree on how to allow property transactions to happen entirely in cryptocurrency.

Portugal, which does not have capital gains taxes for cryptocurrencies, has been a haven for crypto investors. In mid-April, Silva’s office issued guidance on how notaries should approach crypto transactions without the need to convert to euros before becoming legal. Silva says the move reflects a clear desire on the part of buyers: “Crypto is a reality,” he says, “and now you can do [crypto sales] in a legal way with transparency, complying with everything.”

Portugal is unusual in this respect. In most countries, the absence of resources to assess associated tax implications and risks, as well as the danger of money laundering, means conversion to fiat currency is still necessary at some point in the process.

That uncertainty has not deterred companies such as Zome that have taken the plunge and are attempting to work out what a more established crypto real estate market would look like. Zome began scoping out the possibility of cryptocurrency transactions last summer, says Santos, who sees potential to tap a new client base: “If we provide [crypto investors with] a convenient way, in their language, to allow them to do real estate business in Portugal, then we will attract these guys to us.”

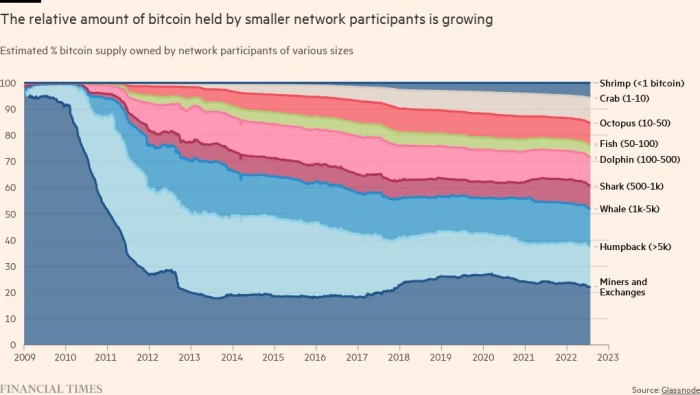

The pool of potential buyers is growing. There are now tens of thousands of bitcoin network participants who hold the equivalent of more than $1mn in their digital wallets. And a survey of US housebuyers commissioned by Redfin in December last year found that 12 per cent of first-time buyers planned to liquidate digital assets for a down payment — up from 5 per cent in the third quarter of 2019.

As trading in cryptocurrencies soared during the pandemic, some investors struck gold and found themselves with the funds to buy property for the first time. Those with established wealth also added crypto to their portfolios. The 2022 Knight Frank Wealth Report, a global survey of more than 600 wealth managers who manage individuals worth over $30mn, found nearly one in five clients now invest in cryptocurrencies, tokens and coins.

That reflected the peak of the market. This year, a crash in crypto prices brought on by rising interest rates has spooked investors and wiped around $2tn off the value of all cryptocurrencies. Yet enthusiasm for crypto property deals remains — and not just among buyers who are looking to convert their increasingly volatile assets into safer investments.

Safe as houses

While some Web3-savvy investors have dabbled in buying virtual properties in the metaverse with their crypto funds, many would prefer their digital wealth to translate into their physical lives.

Daniel Browne, a senior real estate associate at British legal firm Kingsley Napley, says he saw interest in buying property with cryptocurrency build in the run-up to bitcoin’s peak last November. Now, after months of market turbulence, the argument for turning to safer assets is becoming harder to ignore, he says: “People were looking at perhaps having an exit from something that is . . . known to be volatile and then putting money into something a little bit more well known . . . say bricks and mortar.”

Many of Browne’s clients are younger first-time buyers who “had legitimately profited through taking risks and, I guess, some luck along the way as well. And they’re now . . . venturing into something else.”

There is also interest from international buyers looking for second homes abroad. That is one reason why La Haus, a Colombian real estate company that has had backing from Jeff Bezos, has piloted bitcoin property sales in popular tourist locations such as Tulum, Mexico and Colombia’s Caribbean coast. The volumes involved are relatively small. Since its first transaction in January, the company has sold four properties totalling $800,000 in sales.

Doing deals entirely in cryptocurrency means international buyers don’t lose out on exchange rates and fees converting one currency to another, making the transaction process smoother across borders. Zome says it has sold four Portuguese properties in the past two months with buyers from the Netherlands, Canada and Portugal and there are nine more transactions in the pipeline.

Both La Haus and Zome price homes in a country’s government-issued currency and then partner with a crypto-exchange to convert the price into the relevant cryptocurrencies every minute, reflecting the sometimes wild fluctuations of digital coin prices. Over the month of June, for example, the price of one $9mn Los Angeles home ranged from 287 bitcoin to 452 bitcoin.

Sellers can choose whether to accept fiat or cryptocurrency as payment. Marques, the Braga seller, took his in bitcoin. An entrepreneur who runs a design company and a marketing and communications company, he flips houses and recently sold a chain of bakeries in Budapest. Marques started investing in crypto around five years ago. These days, he manages his crypto accounts by dividing them into two pots — one for doing business and the other to hold for the long term.

Despite the turmoil in crypto markets this year, Marques is undeterred. Santos says he has many clients who feel the same. “We asked the first ones, ‘Who wants to sell a house that could be worth double [the cryptocurrency] in three months? What’s the mindset?’” The answer, he says, was more or less uniform. Clients told him they were accustomed to violent price swings and untroubled by volatility: “These investments are for the next three to four years, not the next three to four days.”

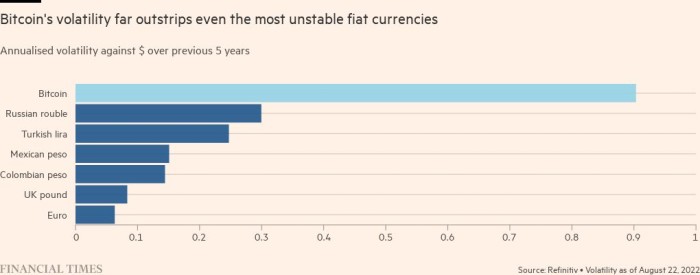

That mindset may prove harder to maintain. Bitcoin’s volatility is orders of magnitude more extreme than even the most unstable of fiat currencies. In June, prices fell below $20,000 (from a peak of $68,000 last November), causing the largest cryptocurrency exchange Binance to halt bitcoin withdrawals for several hours. Since then, Santos says, he’s noticed some buyers stalling in the hope that bitcoin will recover before making a purchase, but that has not dented his own optimism.

Selling crypto

The US crypto real estate market is still in its infancy. Features of the American system such as the requirement for a period of “escrow”, in which dollar-denominated funds from both parties must be held by a neutral third party, mean transactions carried out entirely in cryptocurrency are, for now, impossible.

US regulators have also taken a more hawkish view of crypto markets this year, as a series of high-profile bankruptcies of crypto lenders and hedge funds left investor assets frozen.

That has not prevented efforts to establish a crypto real estate sector. Christine Quinn, a realtor and star of the Netflix reality TV series Selling Sunset, which is set in a high-end real estate brokerage in Los Angeles, has been among the early movers. In April, Quinn started RealOpen, which lists properties and brokers transactions for would-be crypto buyers, with her husband, Christian Dumontet, a tech entrepreneur and co-founder of the delivery service Foodler.

Quinn’s view is that volatility has been a boon to the sector: “People are ready to diversify more than they ever were before because of uncertainty,” she says. “Uncertainty actually creates hype and then creates sales.” Speed is a paramount concern for crypto investors, who are often eager to keep their assets digital until the last possible moment, she says. Sales in crypto can happen more quickly since buyers tend not to have a lender involved and often are not as picky or concerned about the details: “They want it and they want it now. They don’t want to have to wait.”

One potential red flag for any seller is a buyer with a basket of assets that could crash mid-sale, forcing them to pull out. To address this, Dumontet created RealScore, a volatility model that looks at a clients’ distribution of crypto assets and comes up with an estimate of how likely it is they will drop below a point where a sale would fall through.

The most attractive buyers, Dumontet says, are those with a broad basket of crypto assets. Bitcoin and ethereum are the most common cryptocurrencies to transact in, though some of RealOpen’s buyers also hold stablecoins. RealOpen’s 16 exclusive listings total just under $160mn — including a four-bedroom Beverly Hills home listed as belonging to Slash from Guns N’Roses for $8mn (375 bitcoin or 4,890 ether). The company declined to say how many properties it had sold since its launch.

Mainstream participants in the US housing market are also getting in on the game. In June PMG, a national real estate developer, began accepting cryptocurrency for all condominium sales in the US, through a partnership with FTX, the three-year-old crypto exchange founded by Sam Bankman-Fried. Since its first crypto deposit in October last year, it has accepted pre-construction deposits for more than 70 condos including at its projects E11even Hotel & Residences and Waldorf Astoria Residences in Miami, Florida, totalling tens of millions of crypto deposits.

“If there’s a conduit out there to bring more dollars to the US and to buy US real estate, I mean, who wouldn’t be a fan of that?” says Ryan Shear, PMG managing partner. “It’s great for America, it’s great for the economy, it’s good for American real estate jobs.”

For buyers who want to hold on to their digital currency, Florida start-up Milo is offering US dollar loans guaranteed by crypto collateral. Milo has lent some $10mn in mortgages backed by its clients’ crypto holdings since April, ranging from $150,000 to $3mn per loan. If the value of a client’s collateral falls below 70 per cent of the loan value at any point, a margin call is triggered and more collateral must be pledged.

The volatility has some people nervous. “Financialising mortgages where it’s based on collateral of other assets that you’re not really sure that’s the true value of that asset — it gets dangerous,” says Daryl Fairweather, chief economist at Redfin.

US regulators are also urging caution. Back in March, US president Joe Biden signed an executive order directing federal agencies to deliver a plan on cryptocurrency regulation by early September. Gary Gensler, chair of the Securities and Exchange Commission, has called repeatedly for more oversight of digital tokens, making the case for applying pre-existing rules in traditional finance to crypto markets.

Following the money

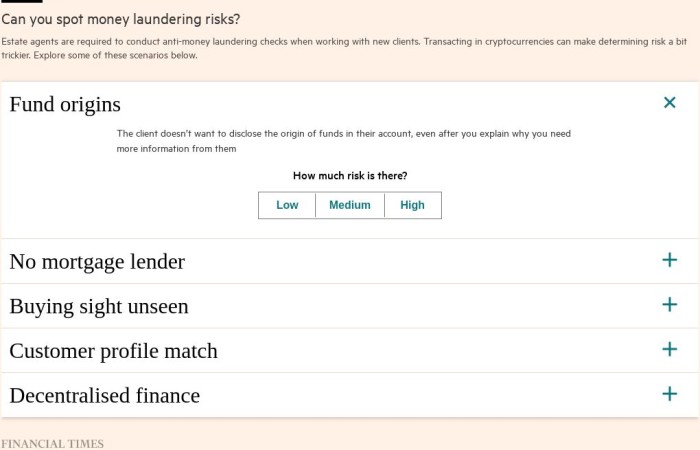

The global real estate market has long been fertile ground for money laundering — the scale of the transactions involved enables black money to be reintroduced into the legal economy while providing a safe investment for those eager to offload illicit cash. Apply that logic to the crypto sector, where regulation is already loose and enormous sums can pass briskly between digital wallets without ringing alarm bells, and the potential for trouble is obvious.

“The real estate market is already struggling in implementing money laundering regulations without cryptocurrencies,” says Ilaria Zavoli, a lecturer at the University of Leeds, who studies money laundering in the UK real estate market. “If you add on top . . . the additional challenges that [cryptocurrencies] bring — anonymity, the question of the lack of intermediaries like banks — this creates an additional burden.”

While all cryptocurrency transactions should, in theory, be transparent and traceable on the blockchain, criminals have been known to use decentralised “crypto mixers” to hide their tracks. Zavoli notes that, at present, many real estate agencies do not employ “personnel capable of understanding [cryptocurrencies]” or have systems capable to carrying out the requisite checks. Regulators need to understand what it’s like on the ground, she says: “You need to have a proper overview of the system.”

Some experts counter that crypto transactions aren’t necessarily riskier. “If there are proper regulations, then the risks could be contained and kept at the level not higher than the normal markets,” says Oleksiy Feshchenko, an adviser in the cyber crime and money laundering section of the UN’s Office on Drugs and Crime.

The United Arab Emirates announced new financial reporting requirements earlier this month aimed at property transactions (of over the equivalent of $15,000) made in cryptocurrencies or with funds derived from them. It is one of the first countries specifically to target real estate in its digital asset-related anti-money laundering efforts.

In anticipation of more regulation, third-party businesses around the world are moving in to offer vetting services. Kingsley Napley, the British law firm, has helped around 70 clients to buy property over the past year using either crypto or large sums of money liquidated from crypto assets with help from one such firm, which tracks the history of all transactions in a client’s wallet and reports back on any links to known scams or hackers.

But Zavoli says these businesses should themselves be vetted since standards vary across countries. In the UK, for example, many crypto companies still aren’t licensed with the Financial Conduct Authority despite the deadline for registration having passed in March.

Even with proper oversight, there are no guarantees that the nascent industry would survive a protracted cryptocurrency meltdown. But, for now, Zome says it has seven sellers on the books who say they will only accept crypto payments and a further 20 who would prefer to receive digital currency.

As for Marques, the seller of the apartment in Braga, he converted his bitcoin proceeds into the stablecoin tether 10 minutes after the transaction on May 4. Five days later, sensing trouble ahead via crypto forums and blogs, he converted his tether into euros. The timing was spot on: tether broke its peg to the US dollar on May 11, in an early sign of the rout that was to come in crypto markets.

Marques admits he was a “lucky guy”. But even though he now owns a little less cryptocurrency than he did before, he says he’d sell a future property in bitcoin.