")

A large portion of Toronto’s eclectic Kensington Market community is on the chopping block, with a group of properties hitting the market for a combined $24 million, and potential plans to redevelop the site with a new mid-rise building.

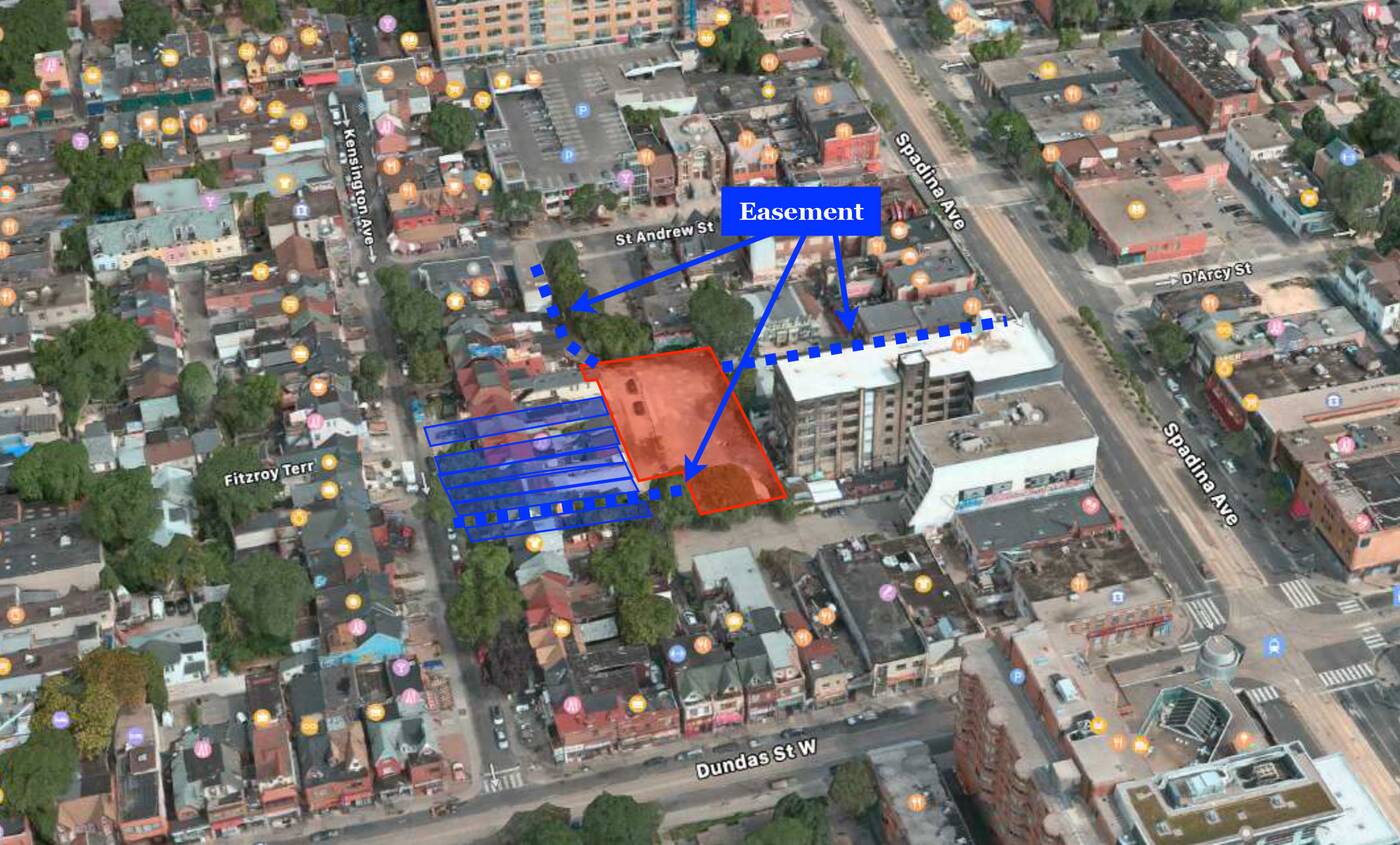

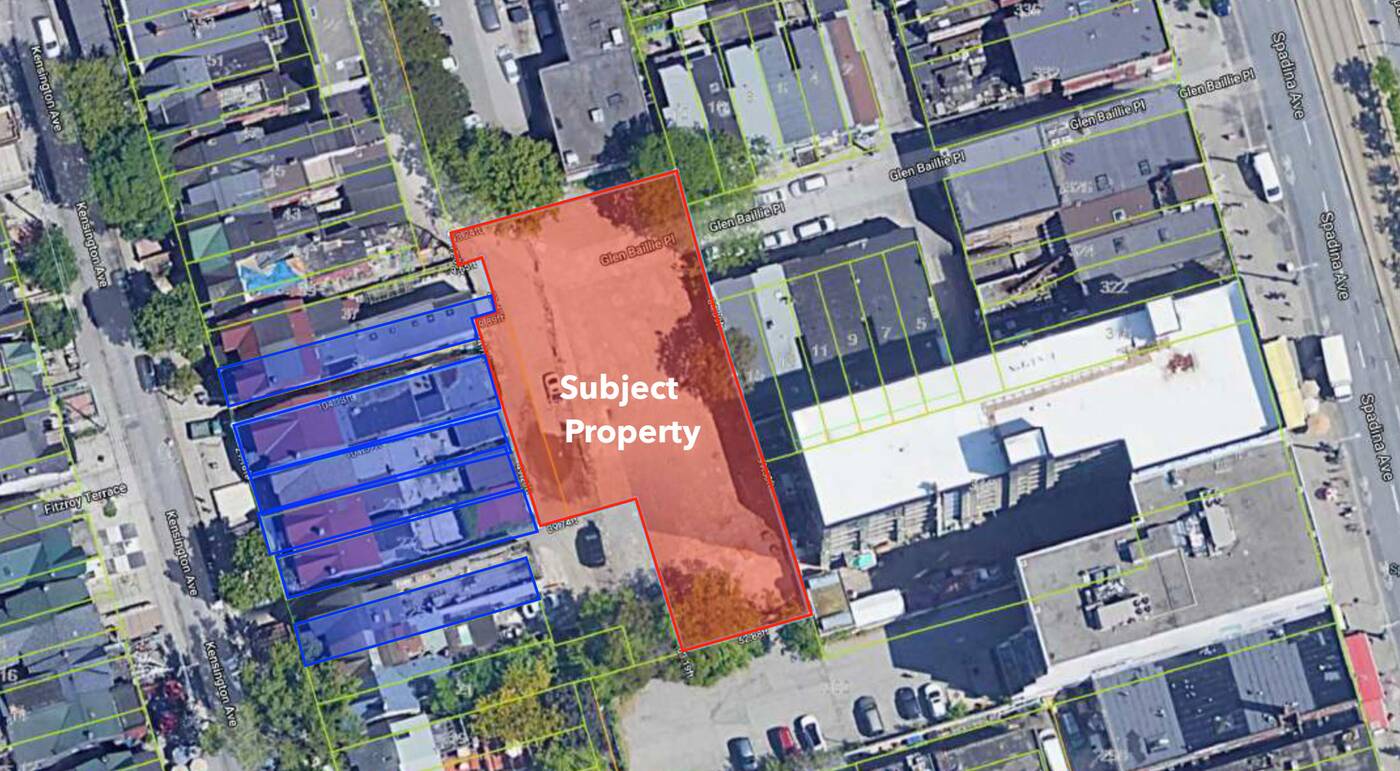

Realtors are shopping a group of seven properties around that includes 23 Saint Andrew Street plus 25 through 35 Kensington Avenue, located just northwest of the Dundas and Spadina intersection.

The document circulating mentions the possibility of purchasing additional properties at 21 and 23 Kensington Ave plus an easement lot attached to 23 St. Andrew, which would add 0.173 acres to the site and increase the developable footprint to 0.66 acres.

The site is currently home to a collection of Victorian semi-detached homes with commercial frontages and includes a handful of businesses such as vintage store Fashion Old and New.

If sold off, it is expected that the new owner of the properties would redevelop the site with a higher-density development, and the document specifically notes the potential for an eight-storey building on the land.

Toronto’s Official Plan does indeed designate this pocket of the city for mixed-use development, though, like pretty much everything else proposed under the city’s archaic zoning by-laws, any mid-rise plan would require a rezoning to move forward.

The site is located within the planned Kensington Market Heritage Conservation District (HCD), which aims to conserve the area’s cultural and built heritage. This would likely only prove a small speed bump in any redevelopment plans, as new development is still permitted in an HCD as long as it adheres to the surrounding style.