(Bloomberg) — Britain’s economy is showing signs of unexpected resilience in a batch of data published Thursday, firming up the case for another interest-rate increase.

Robust figures showing mortgage approvals bouncing back to a five-month high, stronger consumer borrowing and an upward revision to a closely-watched survey of purchasing managers all suggested an economy that’s likely to eek out more growth than expected. Separate figures on inflation expectations also indicated firms expect an even sharper rise in their own prices over the next year.

Together, the readings are likely to lock in bets on a quarter-point rate-hike from the Bank of England on May 11 and fuel speculation of further increases in the months ahead. That marks a sharp contrast with the US, where the Federal Reserve indicated Wednesday that it may pause a rapid series of rate increases.

In Britain, it’s the housing market that’s surprising on the upside. Economists had been expecting property prices to fall as much as 10% this year after a jump in mortgage rates. Instead, the BOE showed the number of approvals for new loans strengthened to a five-month high of 52,000 in March from 44,100 the previous month.

“The UK housing market continues its convincing rebound following the chaos of the mini-Budget,” said Tom Bill, head of UK residential research at Knight Frank. “Price declines appear to be bottoming out and transactions clearly hit their low-point in January. Buyers have accepted the new normal for mortgage rates as stability returns to the lending market.”

That forward-looking measure chimes with reports in the past few weeks from lenders Nationwide Building Society and Halifax showing prices are rising. While net lending for property purchases stalled in March after rising £700 million ($880 million) the month before, the approvals figure gives an indication of how activity may unfold in the months ahead.

The housing market is steady despite the average interest rate on newly drawn mortgages picking up to 4.41% in March, up from 4.24%, according to BOE data published Thursday.

What Bloomberg Economics Says …

“Mortgage approvals increased in March as some households took advantage of mortgage rates edging down from recent highs. While the collapse in the demand for homes may be bottoming out, approvals remain at levels that point to subdued activity and imply the correction in the UK housing market is not over yet.”

—Niraj Shah, Bloomberg Economics. Click for the REACT.

Imogen Pattison, economist at Capital Economics, cautioned that mortgage approvals are unlikely to rise further from their “still weak level.”

“We don’t think that mortgage rates can fall any further until the Bank of England cuts interest rates, which isn’t yet on the horizon,” she said.

Money markets are almost fully pricing in a quarter-point increase in the BOE’s benchmark lending rate to 4.5% on May 11 and a peak of 5% by September.

Other indicators released Thursday included:

- Consumer borrowing also grew strongly in the latest month, rising £1.6 billion in March, more than economists had expected. Those figures cover car loans, credit cards and personal lines of credit.

- The final estimate of the composite purchasing managers’ index pointed to the UK private sector growing at its fastest pace in a year. It rose further into growth territory to a reading of 54.9 in April, up sharply from the first estimate of 53.9.

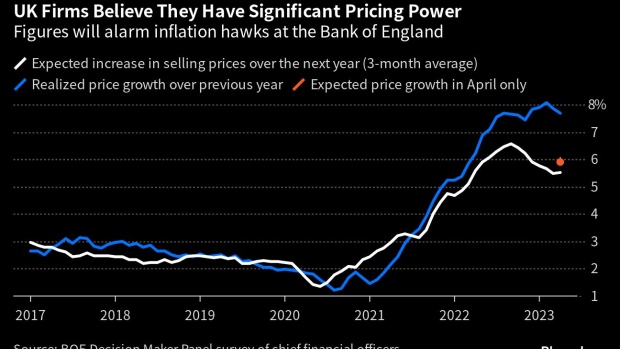

- The BOE’s monthly decision maker panel showed that chief financial officers downgraded their year-ahead inflation expectations despite predicting a sharper increase in their own output prices. Year-ahead output price inflation was expected to be 5.9% in April, up from 5.3% the previous month.

- Money supply figures continued to indicate weakness in the economy. The BOE’s M4 measure fell sharply in the month of March, reducing growth from a year ago to 0.4% from 1.1% the previous month.

Read more:

- Powell Opens Door to June Pause, Stresses Inflation Job Not Done

- UK House Prices Rise for First Time in Eight Months

- UK Economists See One More Rate Hike From Bank of England

- Thatcher Adviser Says BOE Is ‘Hopelessly’ Wrong on Inflation

–With assistance from Andrew Atkinson.