Henrik5000

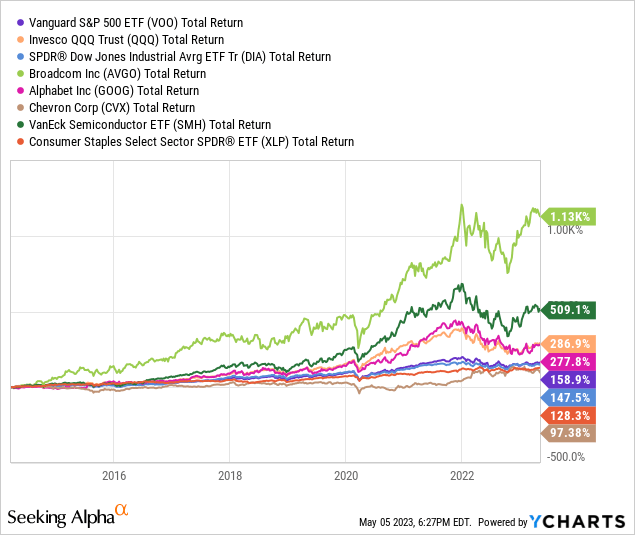

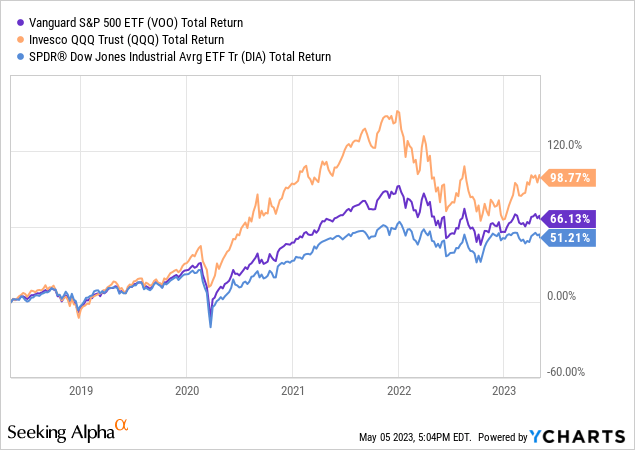

My followers know (or at least should know …) that I advise them to build a well-diversified portfolio and to hold it through the market’s up-n-down cycles. Research shows that is the best way for ordinary investors to achieve the strong returns the market has historically been more than willing to give them. But only if they are “in the market”. While my advice is simple, many investors cannot help themselves from getting in the way of the strategy. That’s because it is way too easy for humans to get side-tracked by short-term investment advice from “professionals” that appears to be a “sure bet” at the time. That has the ordinary investor trading much too often and frequently jumping in-n-out of the market and from sector-to-sector, typically at just the wrong time. However, the chart below should remind investors of my #1 Investment Advice: “Stay The Course”.

To put the chart into perspective, let’s review what has happened over the past 5-years:

- One of the greatest bull-markets of our lives was brought back down to Earth (hard!) by a global pandemic.

- Governments around the globe printed money to help citizens make it through the unprecedented uncertainly and challenges brought about by the pandemic and the human response to it.

- The market bounced back (hard!).

- The world was just beginning to recover from the pandemic when Russia invaded Ukraine – breaking the global energy & food supply chains and forcing inflation, already running hot, even hotter and harder to overcome.

- Central banks around the world have been raising interest rates in an effort to bring inflation back-down to the long-term target of 2%.

- As a result, the U.S. Federal Reserve has raised the Fed-funds rate 9-times over the past year, from 0.25% to 5-5.25%, the sharpest increase in U.S. interest rates since the late 1970’s.

- Partly as a result of these interest rate increases, several U.S. banks got caught sideways (borrowing short, lending long) and went into receivership and/or were sold (a polite way of saying their stock prices went to $0).

- Meantime, ChatGPT burst onto the scene and one can only imagine the various investment advice driven by the “AI is going to take over everything” narrative.

Yet, through all of that, and the short-term noise and investment advice that went along with these events, the chart above shows the 5-year total returns an ordinary investor could have reaped if he or she simply stayed in the three broad U.S. market indicators as represented by the Vanguard S&P 500 ETF (VOO), the Invesco Nasdaq-100 Trust (QQQ), and the SPDR Dow Jones Industrial Average ETF (DIA):

- S&P 500: +66.13%

- Nasdaq-100: +98.77%

- DJIA: +51.21%

And this is the primary reason why I wrote two previous and well-read Seeking Alpha articles on high-level portfolio construction and management:

I have no data to back up my next assertion, but my suspicion is – from writing a lot of articles on Seeking Alpha, and reading (and responding) to a ton of comments from Seeking Alpha users – that the majority of investors on SA would likely have done better over the past 5-years had they simply had a portfolio divided equally between these three funds and had held it throughout all the short-term developments and market “noise” (for lack of a better word).

Of course, there is no way to know for sure if I am right about that. Regardless, I watched as investors went from growth to only screening their investment decisions according to yield and dividend growth. I watched as investors loved technology one minute to being sure the 2022 bear-market in tech was “the end” similar to the dot.com era. I watched as investors were confident EVs would bring about an imminent end to oil, only to see 2022 turn into one of the biggest rallies in oil stocks over the past decade.

Timing the Market

What all these events had in common was that they helped drive short-term investment advice which drove many ordinary investors off their long-term plan. Many sold when they should have been buying and bought when they should have been selling. As I mentioned in the bullets, trying to time the market means you have to be right twice: when to get out, and when to get back in. Research shows this is not the way for ordinary investors to make money in the market and attain wealth. In fact, it is one primary reason why most ordinary investors would be better off becoming a Boglehead: simply investing in solid low-cost S&P500 ETF (like VOO), adding a little to it from time-to-time, and never selling a share. Indeed, research shows the S&P500 outperforms the vast majority of ordinary investors and even the majority of professional money managers.

That being the case, and as I have explained in my prior portfolio management articles on Seeking Alpha, the S&P500 is the cornerstone of my portfolio and its largest position. Further, I consider the S&P500 to be the benchmark for which I judge the returns of my personal portfolio.

Seeking Alpha

That said, and being an electronics engineer, I think the technology sector is the place to be in the 21st Century, so I also hold the triple Q’s ETF (QQQ), the VanEck Semiconductor ETF (SMH), Broadcom (AVGO), Jabil (JBL), as well as Google (GOOG)(GOOGL), Amazon (AMZN), and the Fidelity MSCI IT Index ETF (FTEC), for example. And that has me nicely exposed to “growth”. After all, “Seeking Alpha” implies we want to beat the market (i.e. the S&P500). However, most ordinary investors would be wise to make sure they are at least achieving returns equal to the S&P500 before they break-out on a grand strategy to “beat the market”. Because, fact is, most don’t. But once you are on the threshold of doing so, then you can begin allocating a higher percentage of the portfolio toward the “growth” and “speculative growth” categories knowing you have a well-diversified portfolio as a foundation in case those allocations end up going sideways on you.

Last year, many thought energy stocks were the key to beating the market going forward. And the energy sector certainly did beat the market – at least in 2022. But that was on the heels of the “lost decade” in which the energy sector was the worst performing sector – by far – year-in and year-out during the biggest bull-market of our lives.

I tried to put the point into perspective last October with the Seeking Alpha article: Q3 Surprise: Google Generated $3.7 Billion More FCF Than Chevron. Don’t get me wrong, I consider Chevron (CVX) the best integrated international oil company on the planet (although that may be changing now that Tiny Engine #1 Has Fixed Exxon (XOM)…), and I own Chevron stock (and Exxon). But the point of the article was that investor sentiment on Google was so low, and on Chevron so high, and that even during the so-called low in the digital advertising cycle, and arguably the high in the energy cycle, Google was still delivering superior free-cash-flow as compared to Chevron – on both an absolute and as a percentage of revenue basis. Many investors were likely very surprised by that observation, and many still don’t understand the reason why I was comparing two totally different companies in two totally different sectors. Hopefully, you get the point. And not to belabor it (even though I will …), note that in Q1 Google generated $17.22 billion in FCF (24.7% of revenue) while Chevron generated $4.2 billion (8.6% of revenue). That is, the delta in FCF between the two companies expanded from $3.7 billion in Q3 last year, to a whopping $13 billion in Q1 FY2025.

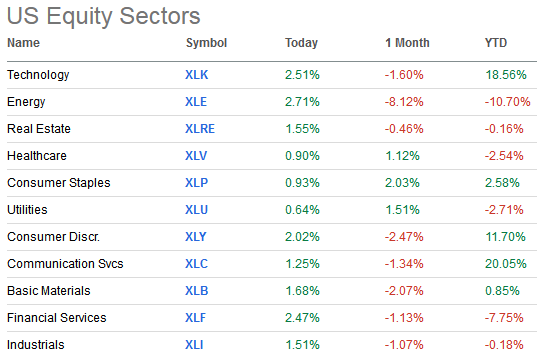

Indeed, I warned investors during the bear-market in the technology sector last year not to sell out of big-tech because they were cash-rich, still delivering strong free-cash-flow, had great global brands, and the U.S. dollar was falling – removing a huge 2022 headwind. Many comments back to me were along the lines of: “you just don’t understand Mike, technology is dead – it’s all about hard assets and yield”. And of course, many “investment professionals” were saying the exact same thing. My reply was “you might be right, but you might also be wrong.” And, as the chart below shows, they were wrong, at least on a YTD basis. And note the strong earnings that Apple (AAPL), Microsoft (MSFT), Google, and Amazon recently delivered.

Seeking Alpha

As you can clearly see in the graphic above, YTD the two best performing sectors of the market have been tech-based: the SPDR Technology ETF (XLK) and the SPDR Communication Services ETF (XLC). Meantime, the worst has been the SPDR Energy ETF (XLE).

Stay The Course

The point here isn’t that I was right, but that I admitted I truly didn’t know. What I did know was selling out of technology last year would be a mistake (indeed, I was adding to my holdings in Broadcom, FTEC, SMH, and JBL last year). What will happen from here to the end-of-the-year? For the next 5-years? I honestly don’t know, and your guess is likely as good as mine, or even better. But what I do know is this: I want to hold a well-diversified portfolio so that I have exposure to the market no matter what happens. That’s because the simple truth is this: over time, the market moves from the bottom-left of your screen to the upper-right.

Another point: had an investor already built a well-diversified portfolio going into bear market last year – including sectors like the SPDR Consumer Staples (XLP), energy, and healthcare – as well as a smattering of I-bonds and precious metals, they likely wouldn’t have been in such a panic to sell a portfolio that may have become considerably over-weight in technology stocks (and sinking rapidly …).

Summary & Conclusions

I am going to leave this article here, short-n-sweet, so that investors can focus on its primary theme: build a well-diversified portfolio that will give you exposure to the gains the market is more than willing to give you. Then, hold that portfolio during the market’s up-n-down cycles. For me personally, I take a top-down approach to allocating capital into broad market ETFs and into the various sectors and stocks that I want exposure to. That is, “Stay The Course” and don’t let short-term emotions and “professional advice” have you jumping in-n-out of the market and switching from sector-to-sector.

Lastly, over the years I have found that during significant market down-turns I am much better at adding to existing portfolio positions as opposed to starting new positions.

I hope you find this investment advice to be helpful and I wish you great success going forward!

I’ll end with a 10-year total returns chart that (hopefully …) adds additional support to my investment advice: