Hi everyone, I just realized that it’s been a while since I put together a good read from the personal finance community post, probably because it takes me a while to put together such articles. Anyway, it’s time to resurrect the good reads articles again.

People have been talking about the pending recession for over a year now. Some people believe that high inflation and high interest rates will trigger the global economy to slow down. Somehow, both the US and Canadian economy remain resilient so far in 2023.

As a reminder, some factors that can trigger a recession include:

- high inflation

- increasing interest rates

- reduced consumer confidence

- higher unemployment rate

- reduced spending and investment activities

The biggest question is if the economy can continue to grow at a modest rate, instead of shrinking.

Despite the US and Canadian economies remaining quite resilient, we’re seeing some signs that a recession may be coming…

- Companies are trimming forces – my company included

- Overall economic outlook softness

- A slowdown in consumer spending… many retailers have reported this in their earnings

- A higher percentage of household income is going toward paying off debt

For people that are still in the accumulation phase, a recession may not necessarily be a bad thing – it will create buying opportunities; for people that are retired or close to retirement, a recession can be more problematic. This is why increasing your cash reserve, reducing equities exposure, and increasing bond exposure are recommended if you are retired or close to retirement.

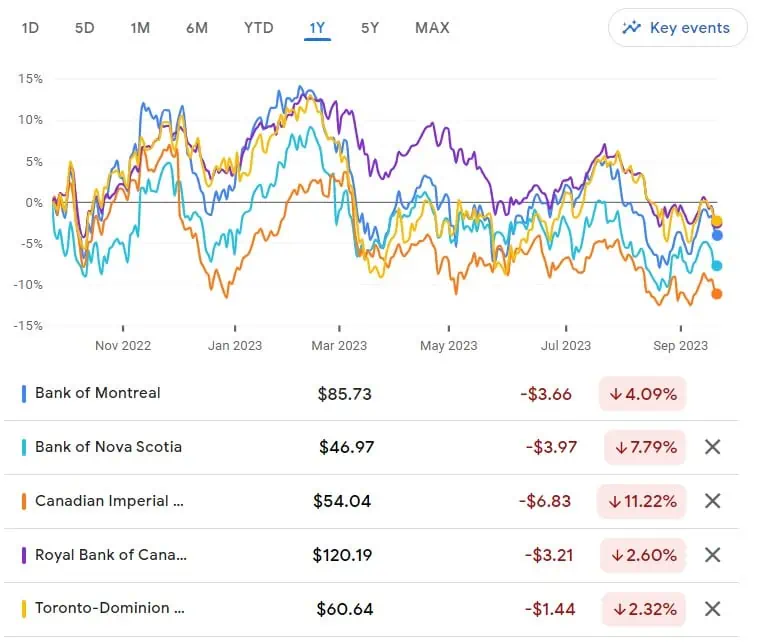

Many dividend investors are curious whether or not Canadian banks will cut dividends. The Canadian banks have not been performing all that well the past year due to concerns over the Canadian real estate market and mortgages.

In preparation for a potential economic slowdown, Canadian banks have been boosting provisions for bad loans. This is exactly what the Canadian banks did during the early days of the COVID-19 pandemic.

If a recession does happen and people default on their mortgages, will the Canadian banks cut dividends?

Difficult to say.

My view? Canadian Big Five banks didn’t cut dividends during the financial crisis, they also didn’t cut dividends during the COVID-19 pandemic. Chances are, they will hold off on any dividend increases until the dust settles.

I believe the Canadian banks won’t cut dividends. Instead, I believe they’ll simply hold the payout steady.

But my prediction can only be 50% correct at best. I can be completely wrong!

So, what can dividend investors do? First, don’t put all your eggs in one basket. Make sure you are not over-exposed to Canadian banks. Diversification is important.

Since the Canadian economy is heavily tied to the financial and oil & gas sectors, it’s important to invest in other sectors like consumer staples, high tech, and consumer discretionary. Investing outside of Canada, therefore, is extremely important.

Good reads from the PF community

Here are some fantastic personal finance/investing related articles that I came across recently.

Mark at My Own Advisor wondered, Should you have 100% of your portfolio in stocks? – “DIY investors, readers and passionate investors know from my site that there is no universal answer for every investor, so it’s important to think through both the upsides and downsides when it comes to your investing plan… While a 100% equity investment portfolio could make sense for younger investors, decades away from retirement, keeping 100% of your portfolio in stocks as you enter retirement or remain in retirement could introduce unnecessary risk.”

Joseph Carlson discussed things that you need to do before you sell a stock

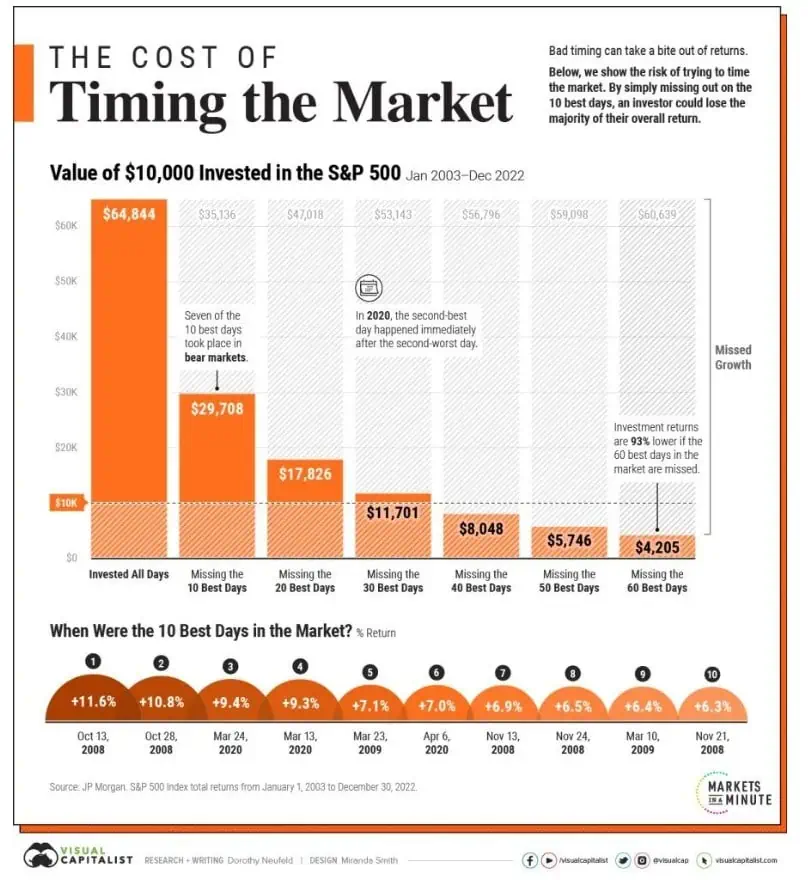

GYM recently turned 40 and shared 40 Financial Lessons She has learned in 40 years – “Time IN the market is better than timing the markets. Stay invested, stick to your plan. This Visual Capitalist chart illustrates the pitfalls of timing the market. If your money wasn’t invested in the 10 best days of the market, you could lose more than half of your overall return on investment. From 2003 to 2022, $10,000 invested in the S&P500 would yield almost $65,000 but if you missed the 10 best days (which were mostly in 2008 and 2009), you would miss out on more than half of your investment returns than if you kept your money invested.” Congrats GYM on turning 40, you certainly shared similar 40 lessons that I’ve learned.

Mike at The Dividend Guy Blog came up with an interesting Retirement Withdrawal Strategy to avoid panic and enjoy life – “It’s no secret that utilities, REITs, and communications companies, especially telcos, are generous dividend providers. Utilities and telcos are usually mature businesses with stable streams of income, making wealth distribution logical. REITs are obligated to distribute most of their income. Add a few Canadian banks in the mix, you’d already have enough sectors to invest easily 60% of your portfolio, while complying with the “don’t exceed 20% in one sector” rule.“

I really like the 17 Questions That Changed My Life from Tim Ferris – “The question I found most helpful was, “If I could only work two hours per week on my business, what would I do?” Honestly speaking, it was more like, “Yes, I know it’s impossible, but if I had a gun to my head or contracted some horrible disease, and I had to limit work to two hours per week, what would I do to keep things afloat?”

I thoroughly enjoyed The paradox of the “perfect life” from Rad Reads – “Consider this thought experiment. You and I both aspire to lead rich and fulfilling lives. Good lives. Some might even say perfect lives. Let’s imagine that you worked assiduously to get that perfect life. You have the perfect job. Impactful, high-paying and the ability to be hybrid. You had the perfect home. Massive square footage, impeccably furnished and immaculately clean. You had the perfect spouse. Smart, sexy and a wonderful co-parent. You had the perfect body. Low BMI, 6-pack abs and a full head of hair. Things are perfect. Or are they? Just like the guy with $70 million who’s scared that he’ll have to fend off gold diggers – have you created a new set of worries?“

With GIC rate at 5% or higher, is it a good idea to “invest” in GICs? Ben Felix explained why cash is a terrible long-term investment

Katie at Money With Katie explained How to avoid lifestyle creep, don’t live beyond your assets – “It wasn’t until I found myself in a peculiar economic position that a more helpful version of this rule emerged for me: Don’t live beyond your assets.Once I found myself graduating from a median income to a higher one, I straddled the line between two worlds: Do I maintain my exact same lifestyle and invest everything extra, or do I recognize that I can afford a little lifestyle creep?The hard part? There’s no rule of thumb for how to handle such a situation. I felt silly skimping on brand name orange juice, but I was also terrified of backsliding into the old, spend-y habits that used to drain my checking account every month.Just because I was making more money didn’t mean I was wealthy, and I struggled to find balance.”