Since retirees and active plan members are fundamentally different, should their investment options reflect that distinction?

That’s the question confronting defined contribution plan sponsors as they explore the relatively new world of in-plan decumulation. As of January, when the Ontario government passed a series of new regulations under the Pension Benefits Act, the majority of Canadian jurisdictions now allow DC plan sponsors to offer variable benefit accounts, with the exceptions of New Brunswick and Newfoundland and Labrador.

Since 2006, members of Saskatchewan’s Public Employees Pension Plan have been able to enroll in these accounts upon retirement. The plan offers the same investment lineup to both its active and retired members: they have the choice of six asset allocation funds, ranging from conservative to aggressive in construction, as well as two specialty funds designed for capital preservation — a bond fund that invests exclusively in long-term fixed income products and a money market fund that invests in short-term income-producing investments. Members can select up to three funds, but only one can be from the asset allocation group.

According to Dara Sewell-Zumstein, retirement information consultant with the province’s Public Employees Benefits Agency, which administers the plan, the continuity was meant to allow members to invest in a way that best suits their lifestyle.

“It really depends on their stage of life, their investment knowledge [and] their goals to determine how they want that money invested. It’s not right to say someone who’s 25 has different options than someone who’s 80. It will depend on their own personal risk tolerance, other forms of income, their spousal situation — all of those things are going to come into play when they make the decision of how to invest their money.”

There’s no inherently right or wrong answer to the question, says Zaheed Jiwani, a principal at Eckler Ltd. Whether plan sponsors elect to keep their existing lineup or look at a new one will depend on their underlying investment philosophy.

“There’s a debate [over whether] you introduce new options in decumulation given that it’s a different state for the plan member. If you offer new options — again, tying this back to your investment beliefs — why does that make sense in decumulation but not accumulation? Some plan members will ask and it’s a discussion plan sponsors need to have.”

Uncharted waters

Don’t follow the crowd

While plan sponsors looking to set up variable benefit accounts may consider consulting what’s being done in other decumulation vehicles such as group RRIFs or LIFs, doing so may give them flawed data, says Eckler’s Zaheed Jiwani. For example, retirees in their mid-70s and beyond have invested heavily in guaranteed income certificates, but not as much in target-date funds. “Most of those members who are later on in decumulation never actually had access to target-date funds in accumulation. During their peak earning periods or if they were working in the ‘80s, GICs were much more popular than they are now. Industry data is not necessarily a good indicator of what you should do.”

The choice is slightly complicated by the reality that variable benefit accounts are still quite new. While they’re usually administered through record keepers, Jiwani notes many are only starting to set them up or aren’t planning to do so until there’s more interest from plan sponsors. Among record keepers that are going ahead, some are planning to offer the same menu they do during accumulation.

Jillian Kennedy, partner and leader of DC and financial wellness at Mercer Canada, says the country’s DC decumulation marketplace — whether for variable benefits or even group registered retirement income funds or life income funds — is where accumulation was 20 years ago. “You still have your 150 funds to pick from [and] you don’t have some of the services left over for you; it’s really a drop into a retail-type market. What we need to do is take that institutional footprint we’ve put into the accumulation world and transport it into the decumulation world.”

But the industry may be at a turning point, says Lauren Bloom, Canadian head of DC sales and intermediaries at T. Rowe Price Group Inc. “[I’ve] spent a lot of time in the marketplace in Canada speaking with consultants and advisors in the DC space and it seems as though conversations are starting to happen, a majority of the time with larger plan sponsors. I think those are [the ones] that will move the dial and lead to more options becoming available.”

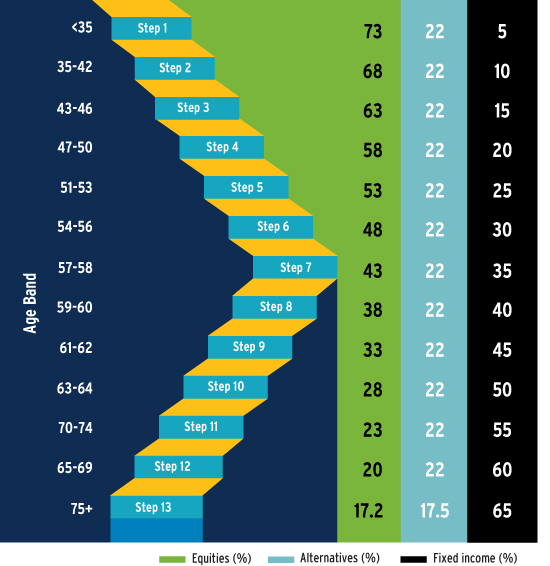

What’s in a target-date fund?

The PEPP’s default, a target-date fund with 13 investment phases, is very popular with active members and retirees. They enter the fund at the step that correlates with their age and it becomes more conservative as they get older. It was built for the PEPP’s average investor, based on the demographics of the plan’s membership.

“We have changed [the asset allocation] over time — people are living longer, people are working longer, so there are other factors that are going to come into play,” says Sewell-Zumstein. “We’re always monitoring it to make sure it matches the demographics of our current membership.”

Target-date funds are typically the core vehicle for members who stick to the default, so it’s important that plan sponsors looking at introducing variable benefits understand what they’re offering to members, says Jiwani. He notes each target-date manager has an underlying glide-path methodology that covers their overall goal for the fund, how they’ve modelled the path in both accumulation and decumulation and what asset classes they offer. “You really need to understand what that overall investment process and philosophy is on the glide path before you even entertain looking at the glide path.”

The main difference for target-date funds in the decumulation stage is whether they glide up to or through that period. Those that glide up to retirement flatten out in the decumulation phase and keep the investment mix constant, says Jiwani, while those that glide through continue de-risking during the member’s retirement, ultimately levelling out much further into that life stage.

“You really need to understand why each manager has had that approach and has come up with that investment philosophy and if that aligns with what you believe, as a plan sponsor, is appropriate for your plan members,” he says. “It’s even more of an important discussion now that plan sponsors are looking at variable benefits and other decumulation vehicles.”

Constructing the portfolio

While many retirees will stick with a target-date fund, some will opt to choose their own asset mix, so plan sponsors will have to consider what to offer. For example, some vehicles designed for capital preservation can have heavier risk exposures, which should be made clear to members, says Jiwani.

“Some fixed income might have more credit risk and some might have more currency or interest rate risk. While on the surface you think you’re providing additional choice to members and that’s a good thing, you may be introducing additional risk, even when you’re talking about something that is supposed to be lower risk.”

On the flip side, plan members also need access to viable equity options to hedge against the risk of outliving their assets. Plan sponsors may also have members with a previous defined benefit pension and whose variable benefit account may not be their main source of retirement income, says Michael Oler, vice-president and retirement income product manager at T. Rowe Price.

“They may be able to satisfy their retirement income goals [from] their DB and state-funded pensions and don’t need a lot of extra income from their other portfolio. If that’s the case, you may be able to structure programs that provide a little bit more risk because they know that they’ve got their minimum income supported by these . . . income streams.”

Alternative schools of thought

While alternative assets provide members with the benefit of diversification in the accumulation stage, making them available in decumulation presents new considerations. Offering alternatives as a sleeve within a multi-asset fund would give members other sources of liquidity should they need it, but a stand-alone fund could significantly hamper their ability to access funds.

“Not all of these alternative asset classes or funds are highly liquid,” says Jiwani. “I’ve seen a few real estate funds on the record-keeping platforms that are closed to new withdrawals because of the current environment. That would be something that’s highly stressful for plan members looking to decumulate.”

The PEPP recently adjusted its six asset allocation portfolios to introduce real estate, liquid alternatives and infrastructure. The plan is currently in the process of implementing those options, notes Sewell-Zumstien, because investing in private equity is a years-long process. “Ideally, we want to provide our members with a good investment that has a good growth rate with lower risk and that’s where the alternative investments came in.”

The level of alternatives is consistent across its six funds, regardless of their risk level. “The idea is that, if we have the same amount through each one of the asset allocations, then when someone moves from one fund to another we’re not concerned with having to sell that asset class, because it is more of a long-term investment,” she says.

Innovation on the horizon

Outside of the decumulation part of a target-date fund’s glide path, investments that are purpose-built for the retirement phase don’t exist in Canada, says Jiwani. Even then, some target-date managers have just left retirement as “the end of the glide path and it’s not explicitly modelled in terms of how they designed the target-date fund.”

But the decumulation side of the glide path will become more important in the coming years. Currently, glide paths are designed to be broadly applicable, but retirement is unique, from the time plan members choose to leave the workforce to what they want to do with those years. Pointing to more developed DC markets in Australia and the U.K., Kennedy suggests Canada could start to see glide paths that would allow members to de-risk at the time they chose to retire, rather than just ones that assume the same retirement age for everyone.

Also within the U.K. market, she highlights investment products that have “target-return outcomes,” which pool longevity risk and allow members to make selections based on their desired income stream and lifestyle. They can pick a more aggressive portfolio knowing they won’t need to access funds for a long time or a more conservative one if they know they need liquidity.

“There are a lot of really nice products we’ve seen around the globe and the targeting return also allows pooling of longevity within a product,” says Kennedy. “All of these things exist, it’s a matter of making sure employees can choose something that aligns to their risk profile.”

According to Jiwani, Eckler has spoken to several investment managers that are currently designing built-for-retirement products to take into account factors such as longevity and shortfall risks, the variety of plan members’ needs and lifestyles in retirement and tax concerns.

Fees are also an important area of the innovation conversation, he says. While DC plans’ institutional power has brought down fees on investments in accumulation, the same isn’t true of the decumulation space, with variation between record keepers. “The fact that we’re going to have access to variable benefits and an increased focus on decumulation vehicles means we need to make sure we’re not eroding plan members’ savings in decumulation.”

Long-term thinking

Key takeaways

• DC plan sponsors that are implementing variable benefit accounts will have to consider whether their investment lineup should be different in the accumulation and decumulation phases.

• It will also be important to become familiar with the investment philosophy behind plan sponsors’ chosen target-date funds, especially how the manager chooses to model the retirement part of the glide path.

• Built-for-decumulation investment products that are currently in development will take into consideration factors such as longevity and shortfall risks, retirement needs and lifestyles and tax concerns.

Of course, DC plan members have to put a lot more thought into their investment strategy during retirement than if they’re retiring with a DB pension, so education will be a key component of a variable benefit offering, says Oler. “Plan sponsors need to take members on that journey — what they should think about, the different ways to think about it in terms of their own stated preferences and how to make that choice. That becomes something where you need to engage them in simple ways.”

Indeed, plan sponsors can’t forget that entering a new life stage doesn’t inherently make plan members savvier investors, says Jiwani. “Plan members exhibit as high a degree of inertia in decumulation as they do in accumulation. . . . [But] people might start to pay more attention to it, so you want to make sure the offerings are very easy to understand and . . . are not going to overwhelm members.”

In terms of products, Kennedy believes this mindset will drive the development of investment options. “I think the variable benefit account is a product that will force us to think more about, ‘Well, maybe as I go into retirement and I’m going to draw on income here, I should have a strategy that aligns to that, [which is] different from the menu of funds that I had while I was working.’ That hasn’t happened yet in our market.”

Kelsey Rolfeis an associate editor at Benefits Canada.

NEW YORK (AP) — Shares of Tesla soared Wednesday as investors bet that the electric vehicle maker and its CEO Elon Musk will benefit from Donald Trump’s return to the White House.

Tesla stands to make significant gains under a Trump administration with the threat of diminished subsidies for alternative energy and electric vehicles doing the most harm to smaller competitors. Trump’s plans for extensive tariffs on Chinese imports make it less likely that Chinese EVs will be sold in bulk in the U.S. anytime soon.

“Tesla has the scale and scope that is unmatched,” said Wedbush analyst Dan Ives, in a note to investors. “This dynamic could give Musk and Tesla a clear competitive advantage in a non-EV subsidy environment, coupled by likely higher China tariffs that would continue to push away cheaper Chinese EV players.”

Tesla shares jumped 14.8% Wednesday while shares of rival electric vehicle makers tumbled. Nio, based in Shanghai, fell 5.3%. Shares of electric truck maker Rivian dropped 8.3% and Lucid Group fell 5.3%.

Tesla dominates sales of electric vehicles in the U.S, with 48.9% in market share through the middle of 2024, according to the U.S. Energy Information Administration.

Subsidies for clean energy are part of the Inflation Reduction Act, signed into law by President Joe Biden in 2022. It included tax credits for manufacturing, along with tax credits for consumers of electric vehicles.

Musk was one of Trump’s biggest donors, spending at least $119 million mobilizing Trump’s supporters to back the Republican nominee. He also pledged to give away $1 million a day to voters signing a petition for his political action committee.

In some ways, it has been a rocky year for Tesla, with sales and profit declining through the first half of the year. Profit did rise 17.3% in the third quarter.

The U.S. opened an investigation into the company’s “Full Self-Driving” system after reports of crashes in low-visibility conditions, including one that killed a pedestrian. The investigation covers roughly 2.4 million Teslas from the 2016 through 2024 model years.

And investors sent company shares tumbling last month after Tesla unveiled its long-awaited robotaxi at a Hollywood studio Thursday night, seeing not much progress at Tesla on autonomous vehicles while other companies have been making notable progress.

TORONTO – Canada’s main stock index was up more than 100 points in late-morning trading, helped by strength in base metal and utility stocks, while U.S. stock markets were mixed.

The S&P/TSX composite index was up 103.40 points at 24,542.48.

In New York, the Dow Jones industrial average was up 192.31 points at 42,932.73. The S&P 500 index was up 7.14 points at 5,822.40, while the Nasdaq composite was down 9.03 points at 18,306.56.

The Canadian dollar traded for 72.61 cents US compared with 72.44 cents US on Tuesday.

The November crude oil contract was down 71 cents at US$69.87 per barrel and the November natural gas contract was down eight cents at US$2.42 per mmBTU.

The December gold contract was up US$7.20 at US$2,686.10 an ounce and the December copper contract was up a penny at US$4.35 a pound.

This report by The Canadian Press was first published Oct. 16, 2024.

TORONTO – Canada’s main stock index was up more than 200 points in late-morning trading, while U.S. stock markets were also headed higher.

The S&P/TSX composite index was up 205.86 points at 24,508.12.

In New York, the Dow Jones industrial average was up 336.62 points at 42,790.74. The S&P 500 index was up 34.19 points at 5,814.24, while the Nasdaq composite was up 60.27 points at 18.342.32.

The Canadian dollar traded for 72.61 cents US compared with 72.71 cents US on Thursday.

The November crude oil contract was down 15 cents at US$75.70 per barrel and the November natural gas contract was down two cents at US$2.65 per mmBTU.

The December gold contract was down US$29.60 at US$2,668.90 an ounce and the December copper contract was up four cents at US$4.47 a pound.

This report by The Canadian Press was first published Oct. 11, 2024.