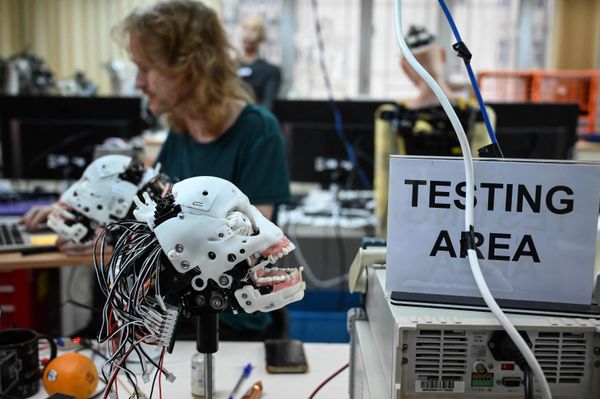

This photo taken on May 10 shows a robot being assembled at Hanson Robotics, a robotics and artificial intelligence company which creates human-like robots, in Hong Kong.PETER PARKS/AFP/Getty Images

I am usually skeptical of hot new technological trends. That’s because, many times, I have seen “the next big thing” not work out, or end up having far different effects and outcomes than first touted.

Furthermore, most companies that are early entrants into new technologies fail, and most early investors see their money and dreams of riches disappear into the ether.

But I think artificial intelligence – the technological trend everyone is talking about these days – is different. It will change investment management. Those that embrace it, and adapt, are likely to prosper.

For instance, AI is fantastic news for the so-called quants – workers whodesign and implement complex models that allow financial firms to price and trade securities. They will be able to spend more time thinking about problems to solve and new methodologies, and less time crunching numbers and writing code. AI will be able to do the work of thousands of quants, so the technology will be quickly able to capitalize on market inefficiencies before others discover the market anomaly. When these types of asset mispricings are discovered, they tend to disappear.

By contrast, AI will be absolutely terrible news for stockbrokers who pitch their high-priced “investments de jour” to their clients. AI will take robo-investing – which has already eaten a lot of the traditional broker’s lunch – to an exponentially higher level. Not only will an AI program be able to buy and sell investments, but it will be able to optimize risk-return levels and even research potential investment methodologies with billions of inputs and parameters within the blink of an eye. Everything from idea generation to back-testing performanceto disaster planning can be handled.

AI is also not subject to emotion, which is the greatest enemy of traders and portfolio managers. And AI will not pull a Bernie Madoff Ponzi scheme (unless programmed to), or blame others during periods of underperformance.

The primary components of AI are generalized learning, reasoning and problem-solving. It is perfectly suited for investment management because those components must be followed in a systematicway by professionals working in the industry. Even the greats like Warren Buffett have to initially learn, use reason and problem-solve. The advantage of AI is that it can follow a systematic process faster and with far more inputs than a human ever can. It can also learn from its mistakes – an ability I wish more of my former colleagues had.

Of course, there could be some hiccups at the start of an AI program’s initial programming. But strategists and the programs themselves will learn.

AI should not be a cause for fear and loathing. It is merely a logical continuation of human progress.

I have seen new technologies profoundly affect investment management over the years. Their arrival was met by fears of massive job losses and economic collapse – but those things never materialized.

My first job was as a junior analyst. I went through company financial statements with a brand new electric calculator, which would advance the paper feed without me manually pulling a crank. I was actually elated when IBM visited my company a few years later, introducing me to MultiPlan, one of the first spreadsheets. It made my work far more efficient and easier to check. Eventually, I did not even have to manually type in the data thanks to the copy-and-paste function.

New developments in data management helped to quickly verify if the investment claims of analysts, fund managers and investment gurus were valid or nonsense. Case in point: Some investment professionals assured the investing public that they were great performers because they bought stocks with low price-to-earnings ratios. But more advanced data helped to verify the efficient-market hypothesis – that share prices already reflected all available information – and refuted simple fundamental strategies. When subject to scrutiny, technical analysis was also shown to not be the holy grail its proponents suggested. The performance of many investing superstars correlated negatively with advancements in data analysis.

Far from eliminating jobs, this type of technology helped investment companies to flourish.

While AI may initially be expensive for a company to adopt, it does not need to be paid an annual salary to carry mortgages on a 5,000-square-foot home in a tony neighborhood, a cottage on a lake and a condo in Palm Beach. AI does not spend its time whining for larger bonuses, undermining the reputations of other AI programs or attending conferences in Las Vegas during Super Bowl weekend.

AI will eventually be able to do everything from learning optimal strategies to learning about individual clients’ risk-tolerance levels based on their actual behaviour. It will also be able to undertake tasks such as buying investments, placing them in clients accounts, sending statements out, paying out cash directly to bank accounts and generating tax reports. Increasingly, much of this has already been done by computer. AI is merely the next step of a continuing process.

AI may eventually even replace most central-bank functions with money algorithms that are more trusted by market participants and the public. For instance, setting the Fed funds rate based on economic data, or automatically supplying short-term liquidity if needed.

If I were recruiting new professionals for an investment counsellor or bank, I would pass on my annual spring visit to Harvard Business School and instead visit the Massachusetts Institute of Technology. The two institutions may be only about a mile away physically, but they may as well be on different continents given where the future is taking us.

TORONTO – Canada’s main stock index was down more than 200 points in late-morning trading, weighed down by losses in the technology, base metal and energy sectors, while U.S. stock markets also fell.

The S&P/TSX composite index was down 239.24 points at 22,749.04.

In New York, the Dow Jones industrial average was down 312.36 points at 40,443.39. The S&P 500 index was down 80.94 points at 5,422.47, while the Nasdaq composite was down 380.17 points at 16,747.49.

The Canadian dollar traded for 73.80 cents US compared with 74.00 cents US on Thursday.

The October crude oil contract was down US$1.07 at US$68.08 per barrel and the October natural gas contract was up less than a penny at US$2.26 per mmBTU.

The December gold contract was down US$2.10 at US$2,541.00 an ounce and the December copper contract was down four cents at US$4.10 a pound.

This report by The Canadian Press was first published Sept. 6, 2024.

TORONTO – Canada’s main stock index was up more than 150 points in late-morning trading, helped by strength in technology, financial and energy stocks, while U.S. stock markets also pushed higher.

The S&P/TSX composite index was up 171.41 points at 23,298.39.

In New York, the Dow Jones industrial average was up 278.37 points at 41,369.79. The S&P 500 index was up 38.17 points at 5,630.35, while the Nasdaq composite was up 177.15 points at 17,733.18.

The Canadian dollar traded for 74.19 cents US compared with 74.23 cents US on Wednesday.

The October crude oil contract was up US$1.75 at US$76.27 per barrel and the October natural gas contract was up less than a penny at US$2.10 per mmBTU.

The December gold contract was up US$18.70 at US$2,556.50 an ounce and the December copper contract was down less than a penny at US$4.22 a pound.

This report by The Canadian Press was first published Aug. 29, 2024.

The crypto market has recently experienced a significant downturn, mirroring broader risk asset sell-offs. Over the past week, Bitcoin’s price dropped by 24%, reaching $53,000, while Ethereum plummeted nearly a third to $2,340. Major altcoins also suffered, with Cardano down 27.7%, Solana 36.2%, Dogecoin 34.6%, XRP 23.1%, Shiba Inu 30.1%, and BNB 25.7%.

The severe downturn in the crypto market appears to be part of a broader flight to safety, triggered by disappointing economic data. A worse-than-expected unemployment report on Friday marked the beginning of a technical recession, as defined by the Sahm Rule. This rule identifies a recession when the three-month average unemployment rate rises by at least half a percentage point from its lowest point in the past year.

Friday’s figures met this threshold, signaling an abrupt economic downshift. Consequently, investors sought safer assets, leading to declines in major stock indices: the S&P 500 dropped 2%, the Nasdaq 2.5%, and the Dow 1.5%. This trend continued into Monday with further sell-offs overseas.

The crypto market’s rapid decline raises questions about its role as either a speculative asset or a hedge against inflation and recession. Despite hopes that crypto could act as a risk hedge, the recent crash suggests it remains a speculative investment.

Since the downturn, the crypto market has seen its largest three-day sell-off in nearly a year, losing over $500 billion in market value. According to CoinGlass data, this bloodbath wiped out more than $1 billion in leveraged positions within the last 24 hours, including $365 million in Bitcoin and $348 million in Ether.

Khushboo Khullar of Lightning Ventures, speaking to Bloomberg, argued that the crypto sell-off is part of a broader liquidity panic as traders rush to cover margin calls. Khullar views this as a temporary sell-off, presenting a potential buying opportunity.

Josh Gilbert, an eToro market analyst, supports Khullar’s perspective, suggesting that the expected Federal Reserve rate cuts could benefit crypto assets. “Crypto assets have sold off, but many investors will see an opportunity. We see Federal Reserve rate cuts, which are now likely to come sharper than expected, as hugely positive for crypto assets,” Gilbert told Coindesk.

Despite the recent volatility, crypto continues to make strides toward mainstream acceptance. Notably, Morgan Stanley will allow its advisors to offer Bitcoin ETFs starting Wednesday. This follows more than half a year after the introduction of the first Bitcoin ETF. The investment bank will enable over 15,000 of its financial advisors to sell BlackRock’s IBIT and Fidelity’s FBTC. This move is seen as a significant step toward the “mainstreamization” of crypto, given the lengthy regulatory and company processes in major investment banks.

The recent crypto market downturn highlights its volatility and the broader economic concerns affecting all risk assets. While some analysts see the current situation as a temporary sell-off and a buying opportunity, others caution against the speculative nature of crypto. As the market evolves, its role as a mainstream alternative asset continues to grow, marked by increasing institutional acceptance and new investment opportunities.

:format(jpeg)/cloudfront-us-east-1.images.arcpublishing.com/tgam/OEEXQ73EE5PIRGOEL6FXE46MJE.jpg){kind=link}