The average price for real estate in Mississauga fell to its lowest mark in two years last month as increased borrowing costs continued to drive prices down.

The latest monthly GTA real estate market statistics from the Toronto Real Estate Board (TRREB) showed an average sale price for all dwelling types combined of $920,587 in January. The last time Mississauga’s overall average was lower than that was in January 2021 at $890,020.

Real estate prices nearly doubled in four years, climbing from a combined average of $644,834 in February 2018 to a peak of $1,225,339 for all dwelling types combined in February 2022.

Since then, the market has gone into a steep decline, losing 24.9 per cent in value in just the past 11 months.

Detached and semi-detached homes have seen the sharpest declines

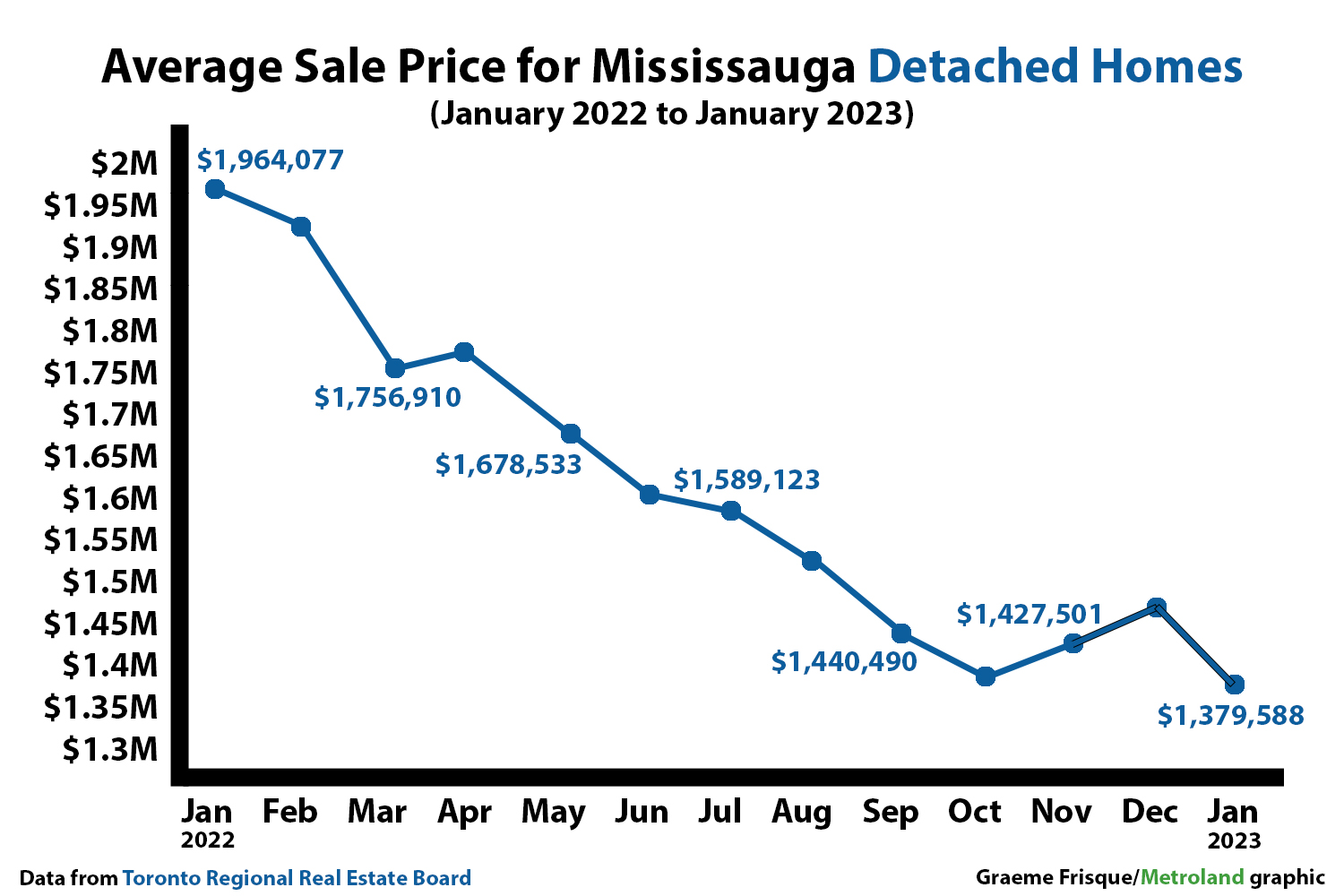

The average price for detached homes peaked out at an average price of $1,964,077 in January 2022. Last month’s average of $1,379,588 represented a 29.7 per cent year-over-year drop. The last time the average price for detached homes in Mississauga was below $1.4 million was in November 2021 at a monthly average of $1,318,779.

The average price for semi-detached homes peaked in February 2022 at $1,314,703 and has fallen by $398,759 — or 30.3 per cent — to an average of $915,944 last month.

Townhouse-style condominiums also peaked in February 2022 at $1,012,860 and have since fallen by 21.2 per cent to a January average $797,702. Likewise, apartment condos fell from a February 2022 peak of $736,006 to $626,401 last month, marking a 14.9 per cent drop.

While those price declines have led to the lowest combined average real estate price seen in Mississauga for two years, it hasn’t translated to an increase in sales — quite the opposite.

Real estate sales in Mississauga last month were by far the lowest January total since TRREB started sharing records in 1996 at just 262 total transactions. The lowest January sales total prior to last month came in 2009 with 311.

TRREB has attributed the drop in sales and prices to the Bank of Canada (BoC) raising its benchmark interest rate from 0.25 per cent to 4.5 per cent since March of last year.

“Home prices declined over the past year as homebuyers sought to mitigate the impact of substantially higher borrowing costs,” said TRREB chief market analyst Jason Mercer in the organization’s monthly analysis.

“Home sales and selling prices appear to have found some support in recent months. This coupled with the Bank of Canada announcement that interest rate hikes are likely on hold for the foreseeable future will prompt some buyers to move off the sidelines in the coming months,” added TRREB president Paul Baron.

However, in the wake of the BoC’s most-recent 0.25 per cent rate hike on Jan. 25, BoC governor Tiff Macklem warned that the central bank foresees continued downward pressure on the housing market through at least the first half of the year. And that the rate increase pause is dependent on higher interest having the desired effect of slowing the economy and taming inflation.

“We are pausing interest rate hikes to assess whether we’ve raised interest rates enough to get inflation all the way back to target,” Macklem said while speaking to reporters in Quebec.

“The fact that we’ve paused may bring people back into the market. These are things we’re going to have to watch,” he said.

Despite recent declines in prices, home ownership in the GTA remains out of reach for most without qualifying for and assuming significant debt far above and beyond what has been traditionally considered financially prudent.

Regardless, both TRREB and the BoC are counting on increased immigration to increase housing demand again as early as the second half of 2023.

“Record population growth and tight labour market conditions will continue to support housing demand moving forward,” said Baron.