(Bloomberg) — Bank of Japan Governor Haruhiko Kuroda said the central bank will keep close coordination with the new government led by Prime Minister Yoshihide Suga to pull the pandemic-hit economy out of its slump.

Kuroda, speaking to reporters Thursday, sought to reassure investors that the BOJ will keep easing in pursuit of its 2% inflation target and maintain its close relationship with the government after its first leadership change in almost eight years.

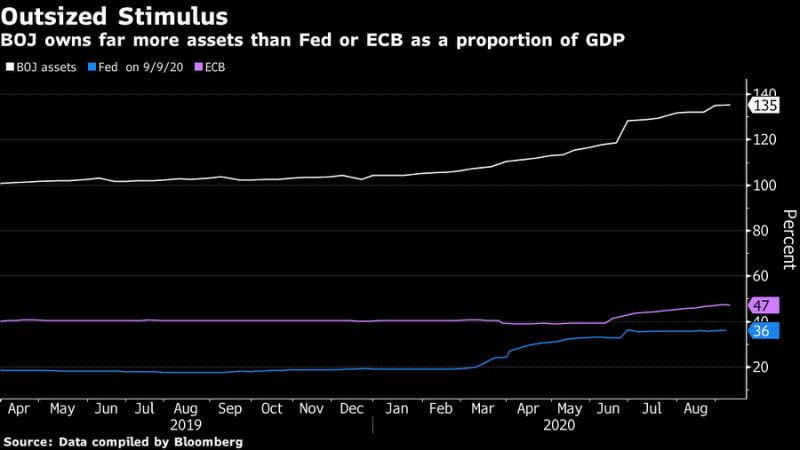

The BOJ earlier stood pat on its key interest rate and its asset purchases, a result expected by 95% of 44 economists surveyed by Bloomberg. The bank also upgraded its economic assessment for the first time since the virus hit, reflecting a bottoming of Japan’s slump.

Suga, who was elected Wednesday for Japan’s top job, has indicated he sees no need for any immediate changes in BOJ policies that have helped keep financial markets stable and get credit to companies amid Covid-19.

The Tough Job Facing Japan’s Next Prime Minister in Five Charts

The BOJ’s decision and Kuroda’s comments reinforced the message that little change was likely for the time being, barring any sharp worsening of the pandemic or a run on markets.

“The BOJ will continue to solidly cooperate with the government as it manages policy,” the BOJ governor said, adding that the current crisis shouldn’t stop structural reforms, an area where Suga has placed emphasis.

“The need for deregulation is widely recognized and the BOJ stands ready to continue to provide a sort of safety net through monetary easing,” Kuroda said, indicating his willingness to support Suga’s goals without waiting for a complete economic recovery.

What Bloomberg’s Economist Says

“The economy is going the right way for the Bank of Japan — prompting it to upgrade its assessment for the first time since the pandemic struck. A recovery is underway, and the economy has lifted off a trough, but while the BOJ kept the parameters of its massive stimulus unchanged (as expected), it can hardly let its guard down.”

Yuki Masujima, economist

Click here to read more.

At its meeting, the BOJ raised its assessment of the economy, saying it had started to pick up with activity resuming gradually, though the pace of improvement was only likely to be moderate with the pandemic continuing to impact countries worldwide.

Analysts see gross domestic product rebounding an annualized 15.1% this quarter, a big jump, but not enough to make up for the record contraction in the three months through June.

Kuroda also went out of his way to defend the importance of the BOJ’s 2% inflation target. Temporary price impacts from the government’s stimulus measures aren’t overly concerning, he said, but the bank will not hesitate to ease if it sees the labor market hurting prices.

Suga Keeps Pressure on Japan’s Telecoms Ahead of Elections

Suga’s vocal campaign against high cell phone fees for consumers has been seen as a sign that he’s less concerned about inflation than his predecessor, Shinzo Abe.

The BOJ decision came just hours after the U.S. Federal Reserve unveiled its latest policy guidance, committing to inflation that averages 2% over time and forecasting near-zero rates to continue through 2023.

“The BOJ is already acutely aware that it can’t raise rates until at least 2023 or before the Fed,” said economist Yoshimasa Maruyama at SMBC Nikko Securities. “The yen isn’t going to shoot up significantly because of any policy difference between the Fed and BOJ as they are basically doing the same thing.”

(Adds Kuroda comment on supporting structural reform.)

<p class="canvas-atom canvas-text Mb(1.0em) Mb(0)–sm Mt(0.8em)–sm" type="text" content="For more articles like this, please visit us at bloomberg.com” data-reactid=”48″>For more articles like this, please visit us at bloomberg.com

<p class="canvas-atom canvas-text Mb(1.0em) Mb(0)–sm Mt(0.8em)–sm" type="text" content="Subscribe now to stay ahead with the most trusted business news source.” data-reactid=”49″>Subscribe now to stay ahead with the most trusted business news source.

©2020 Bloomberg L.P.