(Bloomberg) — Three years after the first case of Covid-19 was reported in Wuhan, Chinese policymakers must now grapple with how to live with the virus while keeping the economy growing fast enough to stave off public anger.

With the Covid Zero policy being rapidly dismantled, the threat of economic disruption remains high. Infections are likely to surge, forcing workers to stay home, businesses may run out of supplies, restaurants could be emptied of customers and hospitals will fill up. Even though there’s optimism the economy will recover as China opens up to the rest of the world, the next six months could be particularly volatile.

Goldman Sachs Group Inc. expects below-consensus economic growth in the first half of next year, saying the initial stages of reopening will be negative for the economy, as was the experience in other East Asian economies. Morgan Stanley predicts China’s economy to remain “subpar” through the first half of next year. Standard Chartered Plc said growth in urban consumer spending will still lag pre-pandemic rates next year given the hit to household incomes during the pandemic.

The economy was already in bad shape this year because of the Covid outbreaks and a property market crisis. While China’s zero tolerance approach to combating infections has kept infections and deaths relatively low for most of the pandemic, the rapid spread of the highly infectious omicron variant exposed the challenges of maintaining strict controls. From snap city-wide lockdowns to almost-daily Covid tests, the restrictions have taken a heavy toll on people’s lives and the economy.

That discontent manifested in mass unrest at the end of last month. People in Beijing, Shanghai and elsewhere started to reject demands for quarantines or lockdowns of their housing estates, and between Nov. 25 and Dec. 5, at least 70 mass protests occurred across 30 cities, according to data compiled by think-tank Australian Strategic Policy Institute.

Authorities have moved to quell public anger by relaxing some Covid requirements around testing and quarantine — although the sudden and confusing changes to the rules over the past few weeks have injected more uncertainty about the economy’s outlook.

Here’s a deeper look at the economy’s downturn and the challenges it faces as China exits Covid Zero.

People have been cooped up in their homesChina’s cities have been hit hard by Covid restrictions, with mobility across the country’s 15 largest cities plummeting in recent months, according to congestion data released by Baidu Inc.

Major hubs are showing strain, including the capital Beijing, as well as Chongqing and Guangzhou. Trips there have plunged in recent months below levels in previous years, according to subway data compiled by Bloomberg.

Few have borne the brunt of China’s Covid Zero policy more than the financial hub of Shanghai, a major epicenter for recent protests. After a two-month lockdown this year to tackle a major outbreak, China’s richest city is still struggling to get back up off its knees.

Malls have seen a surge in vacancies, consumer spending has plunged, and spending in areas like food and beverages has been depressed, mirroring the national trend.

Lack of spending has hit the economy hardCovid restrictions have battered the economy, with consumers pulling back on spending and business output plunging. Retail sales unexpectedly contracted 0.5% in October from a year earlier, with economists surveyed by Bloomberg predicting an even worse outcome of a decline of 3.9% in November.

The government is expected to miss its economic growth target of around 5.5% by a significant margin this year. The consensus among economists is for growth of just 3.2%, which would be the weakest pace since the 1970s barring the pandemic slump in 2020.

With onerous testing rules, flare ups in holiday spots, and official advice discouraging travel, holidaymakers have stayed home, adding a further drag on retail spending. Tourism revenue declined 26% to 287 billion yuan ($40.3 billion) over the week-long National Day holiday in October compared to the same period last year. Flight travel also dropped to its lowest levels since at least 2018.

Youth unemployment is near a record high

That’s all combined to drive growing economic malaise among the country’s youth, with the unemployment rate among 16-24 year-olds soaring to a record high of about 20% earlier this year. Joblessness among young people is more than triple the national rate, with many graduates struggling to find work in the downturn, especially in the technology and property-related industries.

Unemployment will likely get worse next year, when a new crop of 11.6 million university and college students are expected to graduate, adding to pressure in the labor market. Factories are still struggling to cope with Covid outbreaks

So far during the pandemic, the industrial sector has held up better than consumer spending since factories were protected from Covid outbreaks and global demand for Chinese-made goods was strong. That’s changing now.

Export demand is plummeting as consumers around the world grapple with soaring inflation and rising interest rates.

The disruption at a major assembly plant in Zhengzhou for Apple Inc.’s iPhones and violent protests there last month also show the damage that outbreaks can have on production.

The housing market crisis continues to simmer

China’s ongoing real estate slump has also been a source of unhappiness for homebuyers. The property market, which has long been a major driver of the country’s economy, is in its worst downturn in modern history, with sales and prices plummeting. Cash-strapped property developers struggled to finish building homes, prompting mortgage boycotts by thousands of buyers in the summer.

Despite authorities introducing a spate of measures recently to help make borrowing easier and ease tight cash flows for developers, the economy’s downturn and lack of confidence mean the housing market continues to be depressed. The slump is not expected to end soon, with Bloomberg Economics expecting a 25% drop in property investment in the coming decade.Local governments are struggling to fund their spending

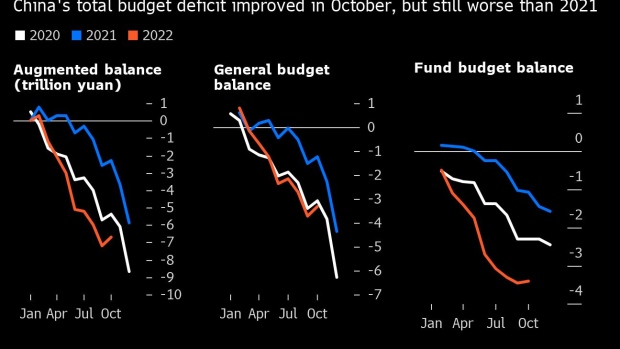

Government finances have come under severe pressure as the economy slumped. Land revenues have plummeted and local governments have had to boost spending on Covid control measures. The broad measure of the fiscal deficit in the first 10 months of the year is nearly triple the amount it was in the same period last year.

Relaxing testing and quarantine rules will help ease pressure on local government finances. However, it remains to be seen how far and fast authorities will go in dismantling Covid Zero if a surge in Covid cases puts strain on the healthcare system, a likely outcome given that a significant portion of the country’s elderly and vulnerable population are still unvaccinated or lacking booster shots.

–With assistance from Kevin Varley, Jin Wu, Danny Lee and Fran Wang.