")

Mongkol Onnuan

Author’s note: All financial data in this article is presented in Canadian dollars.

Enbridge Inc. (NYSE:ENB), a North American energy transportation and distribution giant is currently finding itself near a 52-week low. Income investors may see the rising dividend yield, now at 7.1%, as a reason to scoop up shares. Interestingly, Enbridge has an extensive offering of corporate debt, and the longest dated maturity of 2083, is currently priced below par and offering a yield of greater than 7.6%. While many high yield investors may not be interested, it’s important to note that Enbridge holds an investment grade credit rating, which typically offers fixed income returns of almost 200 basis points lower.

FINRA

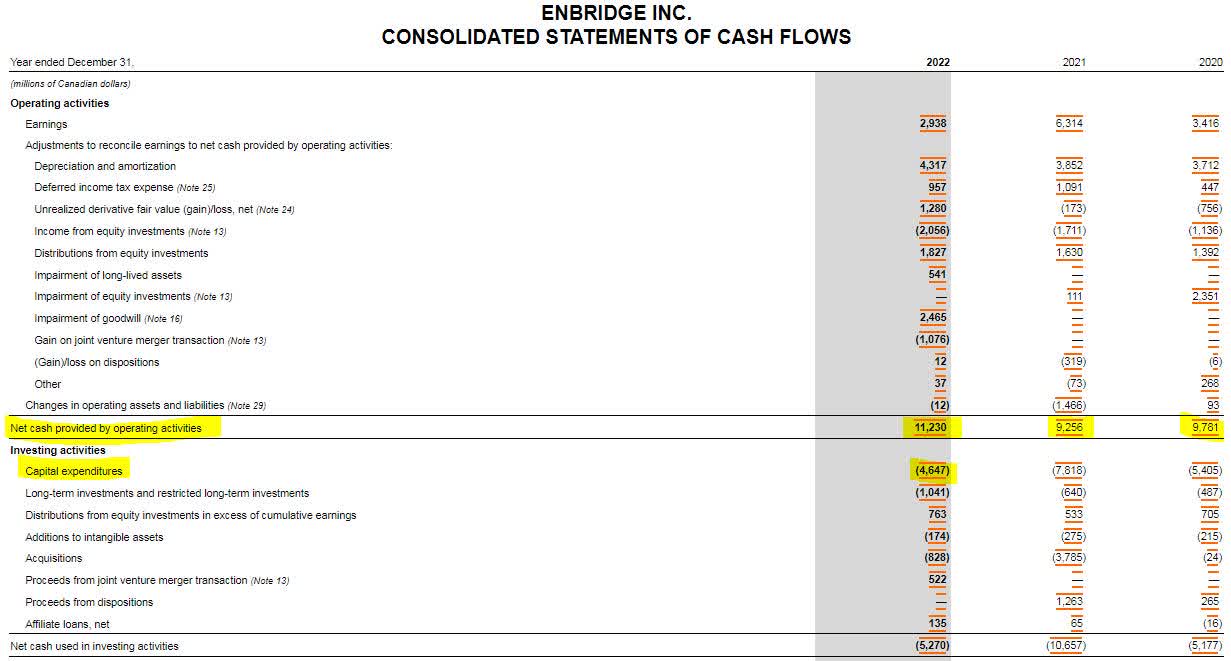

Enbridge’s operation continued to grow in 2022 with revenues up $6 billion from 2021. The company’s expenses outpaced revenue growth, but that was mainly due to the $3 billion write off of assets and intangibles. Had the write offs not occurred, operating income would have been higher in 2022 than in 2021, but nevertheless, the $5.2 billion in operating income was sufficient to cover the company’s interest expenses.

SEC 10-K

While earnings of Enbridge looked healthy last year, the balance sheet tells a slightly different story. The business increased its total debt by more than $5 billion and shareholder equity declined by $1 billion. The company did succeed in building up some cash, but its current liabilities are $8 billion higher than current assets. This working capital deficit will likely lead to new debt issuance or refinancing in the next 12 months.

SEC 10-K

From a cash flow standpoint, debt investors need to see that Enbridge can generate the cash needed to pay down debt. In 2022, Enbridge grew operating cash flow by $2 billion and generated an impressive $6.6 billion in free cash flow. If Enbridge generated so much cash, why did debt increase in 2022? The answer lies in a combination of investing and financing activities. Enbridge invested $2 billion in investments and acquisitions that were not related to capital expenditures. On top of that, the company shelled out $7.3 billion in preferred and common share dividends, and redeemed $1 billion in preferred shares. The culmination of these activities led to the company needing to borrow more than $3 billion. (Note: I believe $2 billion in additional debt was placed on the balance sheet from other investing activities)

SEC 10-K

SEC 10-K

Under Enbridge’s current operating structure, additional capital is needed by either borrowing or selling assets to maintain the common share dividends. While the dividends on the preferred shares are very safe, they are actually yielding less than the coupon yield on the 2083 notes. Investors in long-term debt of Enbridge are getting a safer security for more income.

Seeking Alpha

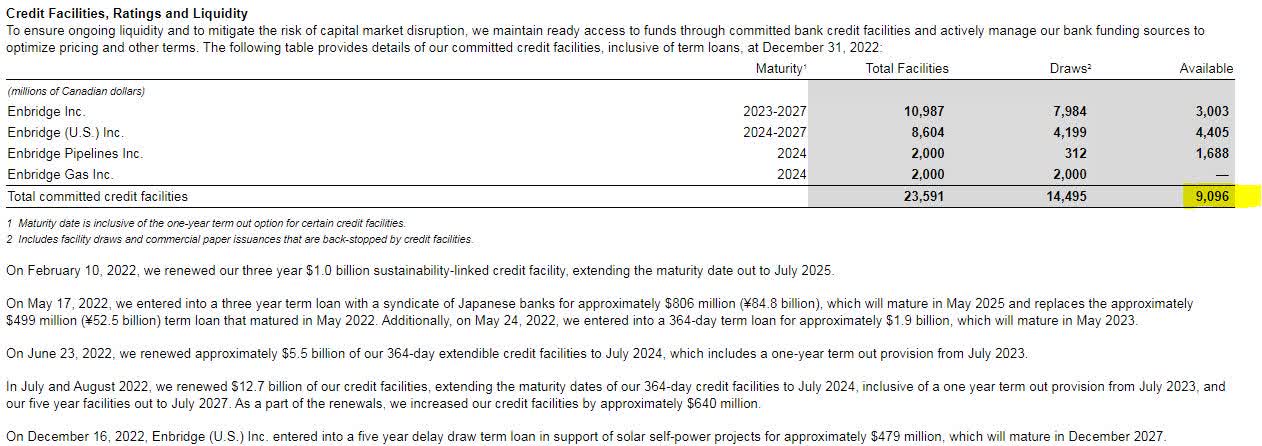

Complicating Enbridge’s future further is the fact that the company has over $14 billion worth of debt maturing over the next 2 years. The need to refinance this debt in a higher interest rate market combined with a working capital deficit is going to put pressure on the dividend. Enbridge may have to choose between its existing dividend and maintaining its credit rating. Fortunately for debt holders, the company does have over $9 billion in liquidity to work with among its existing credit facilities.

SEC 10-K

SEC 10-K

Even if Enbridge is downgraded into junk territory, the company’s 2083 notes are still trading at a higher return than the benchmark BB corporate yield. As in any case in life, there is a catch to what may be considered a “too good to be true” trade. These long term notes were underwritten with an automatic conversion covenant. In the event of a bankruptcy or related event of insolvency, the 2083 bonds would be automatically converted into preferred shares. This strange provision is the likely contributor behind the higher return on the notes.

2083 Notes 424B Filing

While swings and uncertainties in the energy markets over the next several years could greatly change the risk landscape for Enbridge, I believe the company’s strong free cash flow makes it capable of weathering bear markets. Should the company need additional cash flow, it could reduce common share dividends and not impair the value of its bonds.

Note: These notes are not available with all brokerage sites, but they have been traded in increments as low as $5,000, therefore they are available to retail holders.

CUSIP: 29250NBP9

Price: $99.00

Coupon: 7.625%

Maturity Date: 01/15/2083

Yield to Maturity: 7.63%

Credit Rating: (Moody’s/S&P): Baa3/NR