Europe’s Economy Set to Outpace U.S. in Upending of Past Roles

(Bloomberg) — The euro area economy is for once set for a sprightlier recovery from crisis than the U.S., thanks to starkly different responses to the coronavirus.

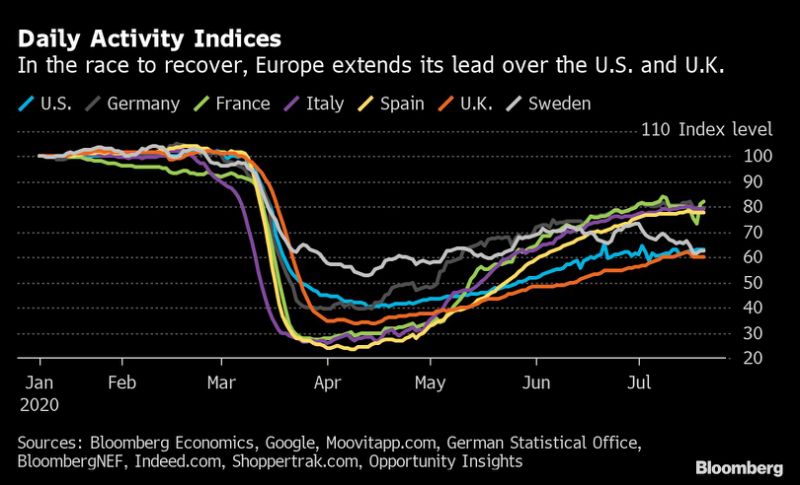

America’s failure to get a grip on the pandemic is putting the brakes on its rebound compared with Europe, where many former virus hot spots managed to resume economic activity without causing a similar surge in infections.

Crucial for a sustainable recovery is confidence that the virus is no longer out of control, and Europe’s relative success may help encourage shoppers to spend and businesses to invest, further propelling demand and growth. The region has also done a better job of protecting jobs and incomes, at least for now, with furlough programs keeping millions of workers on payrolls.

According to JPMorgan Chase & Co., Europe will do better because it has “broken the chain” that links mobility and the virus. Goldman Sachs Group Inc. has cited effective virus control as one reason it expects a “steeper and smoother rebound in the euro area than elsewhere.”

“It’s very clear that the euro area turned down more sharply but we also expect it to bounce back more sharply,” said Jari Stehn, chief European economist at Goldman Sachs. “It’s pretty rare that the euro area would outgrow the U.S. over a horizon of one to two years.”

Since 1992, the U.S. has outperformed the euro area in all but eight years, according to IMF data. Although the euro area managed to grow when the financial crisis hit in 2008 and the U.S. shrank, in 2009 the U.S. contraction of 2.5% was far shallower than the euro area’s 4.5%.

Aggressive lockdowns mean the euro area is set for a sharper second-quarter contraction than the U.S., something that will be seen in GDP figures due this week.

The euro-area economy probably shrank 12% in the three months through June, according to a Bloomberg survey. The U.S. contraction, on an annualized basis, is forecast to be 35%, or a roughly 10% decline quarter-over-quarter.

But high-frequency data suggest Europe is on the mend faster, and Bloomberg Economics estimates that the lead has widened recently.

“Having been hit hardest it’s pretty impressive that we think that Europe will recover more fully,” said Bruce Kasman, chief economist at JPMorgan. “They’ve broken that link — the mobility numbers are going up” without a resurgence of the virus, thanks to better contract tracing, mask-wearing and social distancing measures, he said.

JPMorgan expects the euro area’s economy to shrink 6.4% this year, slightly worse than the 5.1% contraction seen for the U.S. But for 2021, the bank forecasts a 6.2% rebound for the euro area, more than double America’s 2.8% growth.

In the U.S., a jump in cases across the South and West has led several states to halt or even reverse reopening plans. Measures of mobility and restaurant bookings have plateaued, and more than 1 million applications for unemployment benefits continue to be filed each week.

Meanwhile, euro-area purchasing managers indexes jumped more than forecast in July, while numbers for the U.S. came in lower than expected, especially for services, which make up a much larger part of the economy than manufacturing.

The U.S. economic situation could worsen if lawmakers don’t extend — in some form — the extra $600 per week in unemployment benefits that have supported incomes and spending in recent months.

The divergence is reflected in markets. European stocks and bonds have benefited from renewed investor popularity, thanks to the bloc’s agreement on a historic 750 billion-euro ($860 billion) accord. The euro has risen more than 6% against the dollar in the past two months, and could have further to run.

In Europe, generous loan and furlough programs prevented an immediate surge in unemployment, which is also helping the near term. Many were modeled on Germany’s renowned Kurzarbeit and largely proved efficient at getting aid to workers.

But it’s early in the recovery phase, and countries can’t keep funding support indefinitely. If demand doesn’t come back strong enough, companies may eventually have to cut costs, meaning Europe may only have delayed a damaging increase in joblessness.

Just because Europe is in a relatively better position to come out of this in the second half of the year, “doesn’t mean the U.S. can’t catch up,” said Michael Gapen, chief U.S. economist at Barclays Plc.

In the U.S., the $2 trillion rescue package that Congress passed in March ranks among the most aggressive in history, but the distribution has been patchy and uneven. Unemployment offices were overwhelmed with claims, and many jobless Americans have still yet to receive the unemployment benefits they’re owed.

At the same time, the allocation of loans to small and medium-sized businesses had its own challenges, resulting in a chaotic scramble among business owners to get government assistance. Even so, the Paycheck Protection Program helped save as many as 3.2 million jobs, according to a study by Massachusetts Institute of Technology and Federal Reserve researchers.

High-frequency data suggests “things have stalled out, either because there’s exhaustion of initial pent-up demand or because of the virus creating a change in consumer behavior,” said Michelle Meyer, head of U.S. economics at Bank of America Corp. While the third quarter will get a boost from initial state reopenings, “now the question is, how sustainable is that bounce?”

<p class=”canvas-atom canvas-text Mb(1.0em) Mb(0)–sm Mt(0.8em)–sm” type=”text” content=”For more articles like this, please visit us at bloomberg.com” data-reactid=”48″>For more articles like this, please visit us at bloomberg.com

<p class=”canvas-atom canvas-text Mb(1.0em) Mb(0)–sm Mt(0.8em)–sm” type=”text” content=”Subscribe now to stay ahead with the most trusted business news source.” data-reactid=”49″>Subscribe now to stay ahead with the most trusted business news source.

OTTAWA – Canada’s unemployment rate held steady at 6.5 per cent last month as hiring remained weak across the economy.

Statistics Canada’s labour force survey on Friday said employment rose by a modest 15,000 jobs in October.

Business, building and support services saw the largest gain in employment.

Meanwhile, finance, insurance, real estate, rental and leasing experienced the largest decline.

Many economists see weakness in the job market continuing in the short term, before the Bank of Canada’s interest rate cuts spark a rebound in economic growth next year.

Despite ongoing softness in the labour market, however, strong wage growth has raged on in Canada. Average hourly wages in October grew 4.9 per cent from a year ago, reaching $35.76.

Friday’s report also shed some light on the financial health of households.

According to the agency, 28.8 per cent of Canadians aged 15 or older were living in a household that had difficulty meeting financial needs – like food and housing – in the previous four weeks.

That was down from 33.1 per cent in October 2023 and 35.5 per cent in October 2022, but still above the 20.4 per cent figure recorded in October 2020.

People living in a rented home were more likely to report difficulty meeting financial needs, with nearly four in 10 reporting that was the case.

That compares with just under a quarter of those living in an owned home by a household member.

Immigrants were also more likely to report facing financial strain last month, with about four out of 10 immigrants who landed in the last year doing so.

That compares with about three in 10 more established immigrants and one in four of people born in Canada.

This report by The Canadian Press was first published Nov. 8, 2024.

The Canadian Institute for Health Information says health-care spending in Canada is projected to reach a new high in 2024.

The annual report released Thursday says total health spending is expected to hit $372 billion, or $9,054 per Canadian.

CIHI’s national analysis predicts expenditures will rise by 5.7 per cent in 2024, compared to 4.5 per cent in 2023 and 1.7 per cent in 2022.

This year’s health spending is estimated to represent 12.4 per cent of Canada’s gross domestic product. Excluding two years of the pandemic, it would be the highest ratio in the country’s history.

While it’s not unusual for health expenditures to outpace economic growth, the report says this could be the case for the next several years due to Canada’s growing population and its aging demographic.

Canada’s per capita spending on health care in 2022 was among the highest in the world, but still less than countries such as the United States and Sweden.

The report notes that the Canadian dental and pharmacare plans could push health-care spending even further as more people who previously couldn’t afford these services start using them.

This report by The Canadian Press was first published Nov. 7, 2024.

Canadian Press health coverage receives support through a partnership with the Canadian Medical Association. CP is solely responsible for this content.

As Canadians wake up to news that Donald Trump will return to the White House, the president-elect’s protectionist stance is casting a spotlight on what effect his second term will have on Canada-U.S. economic ties.

Some Canadian business leaders have expressed worry over Trump’s promise to introduce a universal 10 per cent tariff on all American imports.

A Canadian Chamber of Commerce report released last month suggested those tariffs would shrink the Canadian economy, resulting in around $30 billion per year in economic costs.

More than 77 per cent of Canadian exports go to the U.S.

Canada’s manufacturing sector faces the biggest risk should Trump push forward on imposing broad tariffs, said Canadian Manufacturers and Exporters president and CEO Dennis Darby. He said the sector is the “most trade-exposed” within Canada.

“It’s in the U.S.’s best interest, it’s in our best interest, but most importantly for consumers across North America, that we’re able to trade goods, materials, ingredients, as we have under the trade agreements,” Darby said in an interview.

“It’s a more complex or complicated outcome than it would have been with the Democrats, but we’ve had to deal with this before and we’re going to do our best to deal with it again.”

American economists have also warned Trump’s plan could cause inflation and possibly a recession, which could have ripple effects in Canada.

It’s consumers who will ultimately feel the burden of any inflationary effect caused by broad tariffs, said Darby.

“A tariff tends to raise costs, and it ultimately raises prices, so that’s something that we have to be prepared for,” he said.

“It could tilt production mandates. A tariff makes goods more expensive, but on the same token, it also will make inputs for the U.S. more expensive.”

A report last month by TD economist Marc Ercolao said research shows a full-scale implementation of Trump’s tariff plan could lead to a near-five per cent reduction in Canadian export volumes to the U.S. by early-2027, relative to current baseline forecasts.

Retaliation by Canada would also increase costs for domestic producers, and push import volumes lower in the process.

“Slowing import activity mitigates some of the negative net trade impact on total GDP enough to avoid a technical recession, but still produces a period of extended stagnation through 2025 and 2026,” Ercolao said.

Since the Canada-United States-Mexico Agreement came into effect in 2020, trade between Canada and the U.S. has surged by 46 per cent, according to the Toronto Region Board of Trade.

With that deal is up for review in 2026, Canadian Chamber of Commerce president and CEO Candace Laing said the Canadian government “must collaborate effectively with the Trump administration to preserve and strengthen our bilateral economic partnership.”

“With an impressive $3.6 billion in daily trade, Canada and the United States are each other’s closest international partners. The secure and efficient flow of goods and people across our border … remains essential for the economies of both countries,” she said in a statement.

“By resisting tariffs and trade barriers that will only raise prices and hurt consumers in both countries, Canada and the United States can strengthen resilient cross-border supply chains that enhance our shared economic security.”

This report by The Canadian Press was first published Nov. 6, 2024.