After a summer in which stocks have hit a seemingly never-ending run of record highs, September brings a series of monetary and political events that could jolt investors out of their complacency.

The will-they-won’t-they debate over trimming pandemic-era stimulus gets an airing with several G10 central banks holding meetings — Australia’s central bank on Tuesday confirmed plans to taper. A showdown over U.S. national debt alongside crucial elections in Japan and Germany add to the risks.

Here are eight events, listed chronologically, which investors will watch in September:

TAPER DOWN UNDER — SEPT. 7

The Reserve Bank of Australia on Tuesday confirmed it was trimming its bond buying programme in the first test this month of central banks’ determination to stick with plans to cut stimulus.

The central bank surprised some by reducing its bond buying by A$1 billion ($745.20 million) a week to A$4 billion, though it also extended the programme to at least mid-February, which was seen as a dovish concession.

The rapid spread of the Delta variant, stay-at-home orders in major cities and a slowing economy had prompted speculation the RBA would delay tapering altogether.

But RBA Governor Philip Lowe predicted an economic rebound once vaccination rates rose and restrictions were eased.

Australian unemployment and interest rates https://fingfx.thomsonreuters.com/gfx/mkt/egpbkkgblvq/australia.PNG

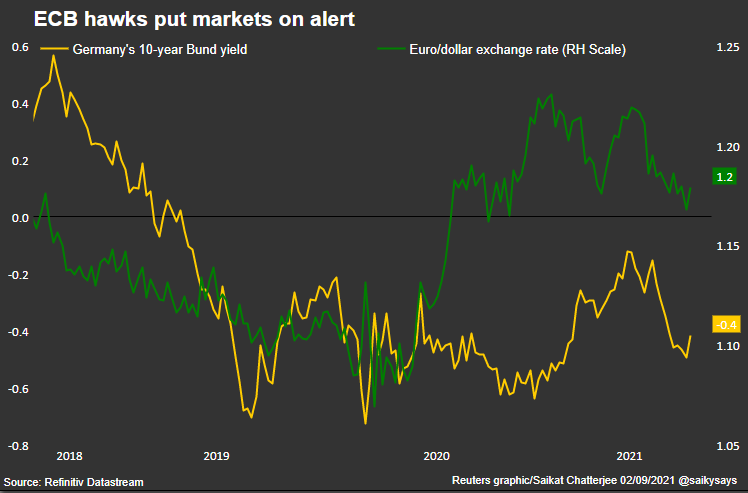

WHO LET THE HAWKS OUT? ECB MEETS — SEPT. 9

Thursday’s European Central Bank meeting could be a lively affair. ECB policy hawks have been out in force, arguing now is the time to start debating the end of a stimulus scheme.

The ECB might opt to slow the pace of purchases but chief Christine Lagarde will likely stress this is not the same as tapering.

Communicating that will not be easy. The risk is markets interpret such a step as hawkish — lifting the euro and sovereign borrowing costs.

ECB hawks put markets on alert

CANADA ELECTION — SEPT. 20

Canadian Prime Minister Justin Trudeau called a snap vote two years early and now faces a tight race.

Trudeau is hoping his management of the pandemic and vaccine rollout will deliver him a majority, but polls show his Liberals in a statistical tie with Erin O’Toole’s Conservatives.

Canadian elections rarely register for global markets, but with the Liberals proposing tax hikes on big banks and both candidates proposing spending increases, this one will be watched closely.

Canada Election: Poll Tracker Canada Election: Poll Tracker https://graphics.reuters.com/CANADA-ELECTION/POLL/lbpgnnyogvq/chart.png

FED TAPER TIMELINE — SEPT. 21-22

Weak August U.S. payrolls have not entirely derailed expectations the Federal Reserve might announce a taper timeline at its September meeting. But with a year-end start to the taper mostly priced in, focus is shifting to when interest rates may rise.

Fed boss Jerome Powell could stress again that tapering and rate increases are separate and that he regards current inflation spikes as transitory.

Fed fund futures are pricing the first hike for early 2023. And we should also know by the meeting whether it will be Powell who presses the button on that rise — his term expires in February 2022. Ninety percent of economists polled by Reuters expect his tenure to be extended.

Fed balance sheet https://fingfx.thomsonreuters.com/gfx/mkt/movannrrrpa/Pasted%20image%201630602241113.png

NORWAY TO HIKE — SEPT. 23

Norway is set to raise interest off 0%, becoming the first of the G10 group of developed economies to do so.

A rate hike will demonstrate its willingness to look beyond rising COVID-19 infections and to focus on a strongly recovering economy.

Investors expect the rise, but confirmation that a major central bank is actually tightening rather than just talking about it — especially after New Zealand unexpectedly baulked at raising in August — would still mark a significant moment for markets hooked on cheap cash.

German Social Democrats lead in the opinion polls https://graphics.reuters.com/GERMANY-ELECTION/gdpzyygbrvw/chart.png

GERMANY VOTES — SEPT. 26

Western Europe’s longest-ruling incumbent leader, Angela Merkel, steps down as German chancellor after 16 years in charge and four straight election victories.

The election has a wider-than-usual range of possible outcomes, especially as the centre-left Social Democrats are leading in the opinion polls, pulling ahead of Merkel’s conservatives for the first time in 15 years.

Two key questions for markets — what will a new government mean for fiscal policy at home and at the European level? And what does it mean for European integration?

JAPAN’S NEXT PREMIER — SEPT. 29

Prime Minister Yoshihide Suga’s decision to resign has given a surprise twist to Japanese politics.

Amid a wave of COVID-19 infections, Suga’s popularity had sunk but there is no frontrunner in the race to succeed him as chief of the ruling Liberal Democratic Party.

Possible candidates include ex-foreign minister Fumio Kishida and the popular minister in charge of Japan’s vaccination rollout, Taro Kono. Whoever triumphs is assured to become premier given the party’s majority in parliament’s lower chamber.

The contest is slated for Sept. 29, and the winner must call the general election by Nov. 28.

Japan’s accelerating COVID-19 cases https://graphics.reuters.com/HEALTH-CORONAVIRUS/JAPAN/gdpzyygdqvw/chart_eikon.jpg

TOWARDS THE X-DATE

The U.S. Treasury technically hit its $28 trillion debt “ceiling” a month ago but by dipping into its bank accounts, it has postponed the day it runs out of borrowing room. Yet the day will soon come — probably in October — when it lacks the money to pay its obligations.

To prevent a government shutdown or worse, a technical default, Congress must this month raise or suspend that limit. Republican senators, opposed to the Democrats’ $3.5 trillion infrastructure plan, have vowed to vote against raising the ceiling.

Back in 2011 the debt ceiling bickering induced S&P Global to cut U.S. credit ratings to AA+ from AAA. Fitch might do the same this time, leaving the United States with only a Moody’s triple-A rating.

While there is no sign bond markets are pricing in a risk of default, that could change. In the words of NatWest analysts, it “sets up a September to remember in DC”.

Debt ceiling https://fingfx.thomsonreuters.com/gfx/mkt/dwvkrrmnqpm/Pasted%20image%201630596029635.png

(Reporting by Tommy Wilkes, Sujata Rao and Dhara Ranasinghe; Editing by Hugh Lawson and Raissa Kasolowsky)

Related

{kind=link}