As sections of the global economy tip-toe toward reopening, it’s becoming clearer that a full recovery from the worst slump since the 1930s will be impossible until a vaccine or treatment is found for the deadly coronavirus.

Consumers will stay on edge and companies will be held back as temperature checks and distancing rules are set to remain in workplaces, restaurants, schools, airports, sports stadiums and more.

China — the first major economy consumed by the virus and the first to emerge on the other side — has been able to revive production but not demand. The lesson for other economies: it’ll be a stop-start path back toward normal.

There’s also the risk of new flare ups. Some 108 million people in China’s northeast region have been put back under varying degrees of lockdown amid a new cluster of infections. Doctors there are also seeing the coronavirus manifest differently, suggesting that it may be changing in unknown ways.

In South Korea – where the virus was controlled without a hard lockdown — consumer spending remains weak as infections continue to pop up.

Sweden’s highly contested response left much of the economy open, yet the country is still headed for its worst recession since World War II.

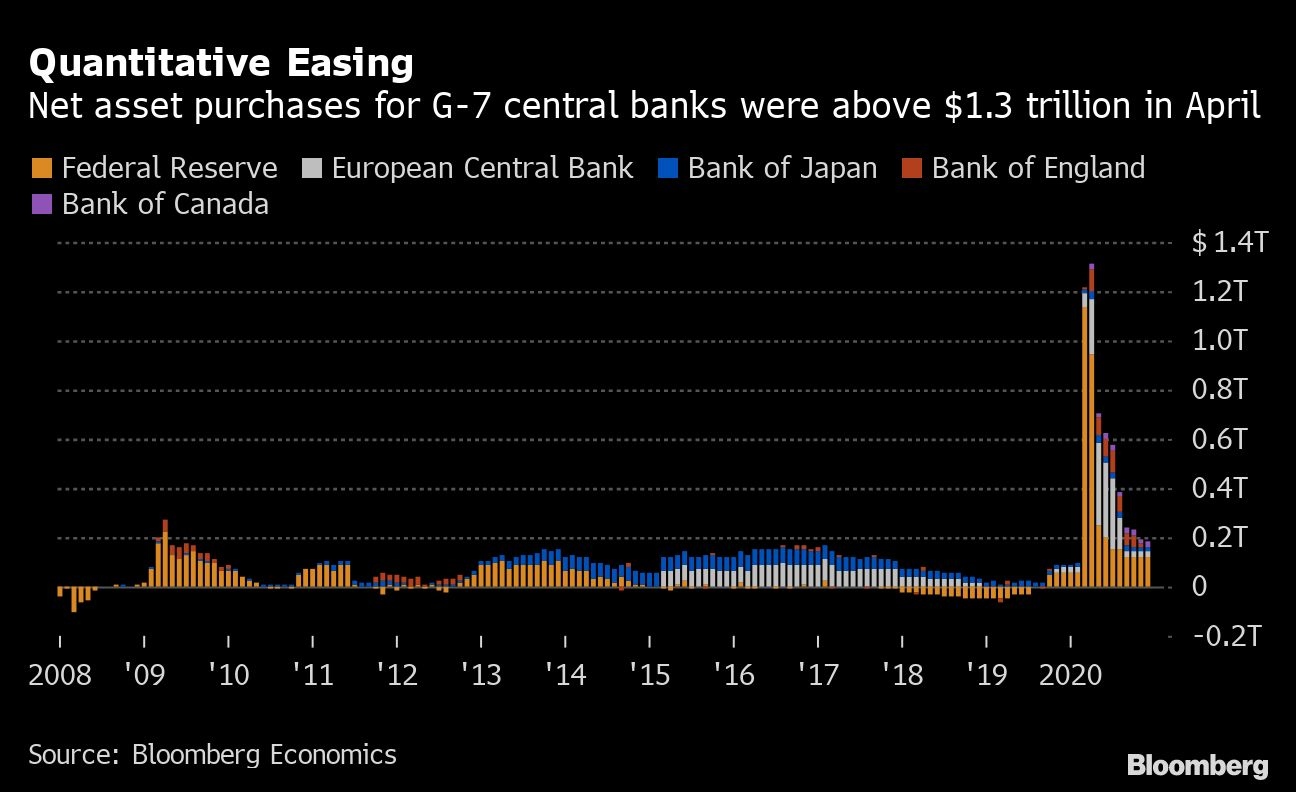

That means global policy makers — who have already announced trillions of dollars of fiscal and monetary support — will need to keep the stimulus flowing to avoid yet more company failures and job losses. Federal Reserve Chairman Jerome Powell has warned that a full recovery will need to wait until the scientists deliver, a warning echoed by his Australian counterpart.

“If we don’t get breakthroughs on the medical front, then I think it’s going to be quite a slow recovery,” Australia’s central bank chief, Philip Lowe, said this week. “We’ve got a lot resting on the shoulders of the scientists here.”

Harvard University professor Carmen Reinhart, who is the incoming chief economist of the World Bank, had a similar message. “We’re not going to have something akin to full normalization unless we (a) have a vaccine and (b) — and this is a big if — that vaccine is accessible to the global population at large,” she told the Harvard Gazette.

With global infections topping five million and a death toll of over 330,000, there’s an air of desperation for good news on either a vaccine or effective anti-viral.

Shares in Cambridge, Massachusetts-based Moderna Inc. hit a record on Monday on early data from a small trial of the company’s coronavirus vaccine. It gave up some of those gains in later days as investors weighed the early nature of the vaccine data.

A survey of money managers by Bank of America Corp. found the biggest tail risk is a second wave of the virus that means restrictions will have to be imposed again. Only 10% expect a rapid rebound, the bank said in a note titled “V is for Vaccine”.

The race for a cure has a geopolitical edge too. U.S. President Donald Trump has vowed a Manhattan Project-style effort dubbed “Operation Warp Speed” to develop a cure, while China’s President Xi Jinping has pledged to make one universally available once it’s developed.

The fusion of when successful drugs can be found and when economies can get back to normal is dominating sentiment in financial markets.

“There is a global bounty on the virus,” said Stephen Jen, who runs hedge fund and advisory firm Eurizon SLJ Capital in London. “I don’t see how it is wiser for investors to bet on the virus than to bet on science, technology, and unlimited political and financial capital in the world to contain and defeat the virus.”

Health experts caution that the process for developing an effective immunity will take time – possibly years. And even then it will need distribution on an unprecedented scale, according to Anita Zaidi, Director of Vaccine Development and Surveillance at the Bill & Melinda Gates Foundation.

“I am optimistic we can develop a vaccine by the end of 2020,” she said during a discussion hosted by Bloomberg New Economy. “I am not very hopeful that we can deploy a vaccine for mass use by the end of 2020 because of the unprecedented scale needed to immunize the whole world.”

Deutsche Bank AG economists are working on the basis that a vaccine or a cure won’t be widely available for the next year and a half.

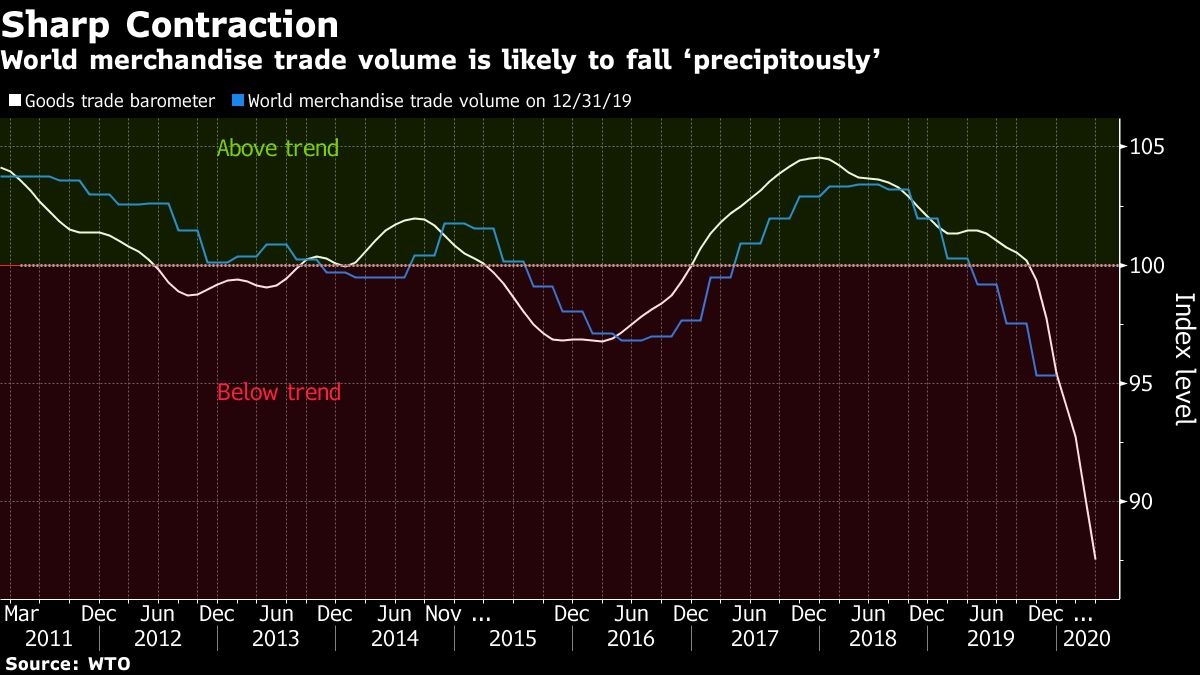

In the meantime, the cogs of global commerce are in limbo. The International Monetary Fund has warned the “Great Lockdown” recession would be the steepest in almost a century. More than 1 billion workers are at high risk of a pay cut or losing their job, the International Labour Organization warned in April. World merchandise trade volume is likely to fall “precipitously” in the first half of 2020, according to the World Trade Organization.

Critically, consumer confidence is shattered. One example: U.K. retail sales dropped by almost a fifth in April.

Bloomberg Economics estimates the lockdowns triggered a drop in activity of around 30% and their research found that the first steps to relax controls will have a more positive impact on activity than later ones.

Central bank chiefs, who have had to resort to considering scenarios instead of hard forecasts, are staying in crisis mode.

Powell has pledged to keep using the Fed’s tools. The Bank of Japan, in an emergency meeting on Friday, launched a new lending program worth 30 trillion yen ($279 billion) to support small businesses as a key inflation gauge slid below zero in April for the first time in more than three years. India’s central bank cut interest rates in an unscheduled announcement on Friday to their lowest since 2000.

While the world waits for a vaccine, workers employed in areas like tourism will need to be reskilled and shifted to where there’s demand, a process that will take time, said Shaun Roache, Asia-Pacific chief economist at S&P Global Ratings.

“Without a medical solution, either a vaccine or effective therapy, persistent behavior change would lead to large structural shifts in the economy,” he said.

Big employers are already adapting to the new, new normal. Facebook Inc. plans to hire more remote workers in areas where the company doesn’t have an office, and let some current employees work from home permanently. JPMorgan Chase & Co. expects to keep its offices half full at the most for the “foreseeable future.”

The circuit breaker to all of this would be a scientific breakthrough, said Torsten Slok, Deutsche Bank Securities Chief Economist.

The Canadian Institute for Health Information says health-care spending in Canada is projected to reach a new high in 2024.

The annual report released Thursday says total health spending is expected to hit $372 billion, or $9,054 per Canadian.

CIHI’s national analysis predicts expenditures will rise by 5.7 per cent in 2024, compared to 4.5 per cent in 2023 and 1.7 per cent in 2022.

This year’s health spending is estimated to represent 12.4 per cent of Canada’s gross domestic product. Excluding two years of the pandemic, it would be the highest ratio in the country’s history.

While it’s not unusual for health expenditures to outpace economic growth, the report says this could be the case for the next several years due to Canada’s growing population and its aging demographic.

Canada’s per capita spending on health care in 2022 was among the highest in the world, but still less than countries such as the United States and Sweden.

The report notes that the Canadian dental and pharmacare plans could push health-care spending even further as more people who previously couldn’t afford these services start using them.

This report by The Canadian Press was first published Nov. 7, 2024.

Canadian Press health coverage receives support through a partnership with the Canadian Medical Association. CP is solely responsible for this content.

As Canadians wake up to news that Donald Trump will return to the White House, the president-elect’s protectionist stance is casting a spotlight on what effect his second term will have on Canada-U.S. economic ties.

Some Canadian business leaders have expressed worry over Trump’s promise to introduce a universal 10 per cent tariff on all American imports.

A Canadian Chamber of Commerce report released last month suggested those tariffs would shrink the Canadian economy, resulting in around $30 billion per year in economic costs.

More than 77 per cent of Canadian exports go to the U.S.

Canada’s manufacturing sector faces the biggest risk should Trump push forward on imposing broad tariffs, said Canadian Manufacturers and Exporters president and CEO Dennis Darby. He said the sector is the “most trade-exposed” within Canada.

“It’s in the U.S.’s best interest, it’s in our best interest, but most importantly for consumers across North America, that we’re able to trade goods, materials, ingredients, as we have under the trade agreements,” Darby said in an interview.

“It’s a more complex or complicated outcome than it would have been with the Democrats, but we’ve had to deal with this before and we’re going to do our best to deal with it again.”

American economists have also warned Trump’s plan could cause inflation and possibly a recession, which could have ripple effects in Canada.

It’s consumers who will ultimately feel the burden of any inflationary effect caused by broad tariffs, said Darby.

“A tariff tends to raise costs, and it ultimately raises prices, so that’s something that we have to be prepared for,” he said.

“It could tilt production mandates. A tariff makes goods more expensive, but on the same token, it also will make inputs for the U.S. more expensive.”

A report last month by TD economist Marc Ercolao said research shows a full-scale implementation of Trump’s tariff plan could lead to a near-five per cent reduction in Canadian export volumes to the U.S. by early-2027, relative to current baseline forecasts.

Retaliation by Canada would also increase costs for domestic producers, and push import volumes lower in the process.

“Slowing import activity mitigates some of the negative net trade impact on total GDP enough to avoid a technical recession, but still produces a period of extended stagnation through 2025 and 2026,” Ercolao said.

Since the Canada-United States-Mexico Agreement came into effect in 2020, trade between Canada and the U.S. has surged by 46 per cent, according to the Toronto Region Board of Trade.

With that deal is up for review in 2026, Canadian Chamber of Commerce president and CEO Candace Laing said the Canadian government “must collaborate effectively with the Trump administration to preserve and strengthen our bilateral economic partnership.”

“With an impressive $3.6 billion in daily trade, Canada and the United States are each other’s closest international partners. The secure and efficient flow of goods and people across our border … remains essential for the economies of both countries,” she said in a statement.

“By resisting tariffs and trade barriers that will only raise prices and hurt consumers in both countries, Canada and the United States can strengthen resilient cross-border supply chains that enhance our shared economic security.”

This report by The Canadian Press was first published Nov. 6, 2024.

OTTAWA – Statistics Canada says the country’s merchandise trade deficit narrowed to $1.3 billion in September as imports fell more than exports.

The result compared with a revised deficit of $1.5 billion for August. The initial estimate for August released last month had shown a deficit of $1.1 billion.

Statistics Canada says the results for September came as total exports edged down 0.1 per cent to $63.9 billion.

Exports of metal and non-metallic mineral products fell 5.4 per cent as exports of unwrought gold, silver, and platinum group metals, and their alloys, decreased 15.4 per cent. Exports of energy products dropped 2.6 per cent as lower prices weighed on crude oil exports.

Meanwhile, imports for September fell 0.4 per cent to $65.1 billion as imports of metal and non-metallic mineral products dropped 12.7 per cent.

In volume terms, total exports rose 1.4 per cent in September while total imports were essentially unchanged in September.

This report by The Canadian Press was first published Nov. 5, 2024.