If you have a large or complicated estate, it pays to take a look at insurance, experts say

Q: “My wife and I are both 50 and have two kids. Our household income is about $200,000 a year, evenly split between my wife and I. I’d like to leave a large inheritance to my two kids. Is it ever a good idea to buy a whole life insurance policy as an investment vehicle? Why or why not? And if not, what would be a better option? — Alejandro

FP Answers: Whole life insurance can be a controversial product, but its two main features, tax-sheltered growth, and a tax-free death benefit, make it worth considering when you’re doing estate planning, or when looking for another tax shelter after maximizing your registered retirement savings plans (RRSPs) and tax-free savings accounts (TFSAs).

Integrating whole life insurance into a plan is unique to everyone and there are many different ways to leverage the value of a policy, but that’s a topic for a different article. Your questions here are whether whole life insurance is a good investment and what are the alternatives if you want to leave a large inheritance to your children?

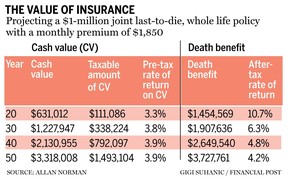

At year 40, or when both you and your wife turn age 90, the whole life policy is projected to give you an average annual after-tax return of 4.8 percent. Keep in mind this is not guaranteed. The projected values and returns will be different, but the results shown are based on current rates.

By comparison, current five-year guaranteed investment certificates (GIC) rates are sitting at five per cent. Forgetting tax for a minute, investing the $1,850 monthly premium into a GIC over 40 years will grow to $2,755,651. If you factor in a marginal tax rate of 40 per cent, the GIC investment would only grow to $1,701,891, about $1 million less than insurance. Does that make whole life insurance a good investment?

Sometimes, there isn’t an alternative to whole life for inheritance purposes, or it takes time to create an alternative. What insurance, term or whole life, excels at is providing an immediate estate value — or inheritance value — for your children. I don’t know of any alternatives that can do that.

You can create alternatives to whole life insurance if you have the time and the ability to save and invest money. These alternatives combine term insurance with investment and/or debt-reducing strategies. Term insurance is put in place to provide the immediate estate value and buy you time to grow your investments to the point where the insurance is no longer required.

There is always a risk when creating alternatives that by combining term and investing strategy you won’t save enough, you’ll spend your money yourselves, the markets may crash the day you die, you have a new spouse later in life and so forth. Insurance is called insurance for a reason.

Decide what’s important to you about leaving money to your children when you die. What benefits would come to you and your children if you gifted them money earlier in their lives?

Whole life insurance can also be used as an investment vehicle to create and maintain an estate’s value. But I find that its tax advantages more often make it more useful once a large estate has been created through investing, multiple real estate holdings, corporate success, farming and other investments. If you have a large or complicated estate, it pays to take a look at insurance.

Allan Norman provides fee only certified financial planning services through Atlantis Financial Inc. Allan is also registered as an investment advisor with Aligned Capital Partners Inc. He can be reached at www.atlantisfinancial.ca or [email protected]. This commentary is provided as a general source of information and is not intended to be personalized investment advice.

_Share this article in your social network