New projections show stronger growth than expected in 2021, but the untackled problems of inequality, indebtedness and weak investment threaten hopes for a more resilient future.

The global economy is set to grow by 4.7% this year, faster than predicted in September (4.3%), thanks in part to a stronger recovery in the United States, where progress in distributing vaccines and a fresh fiscal stimulus of $1.9 trillion are expected to boost consumer spending, says a new UNCTAD report.

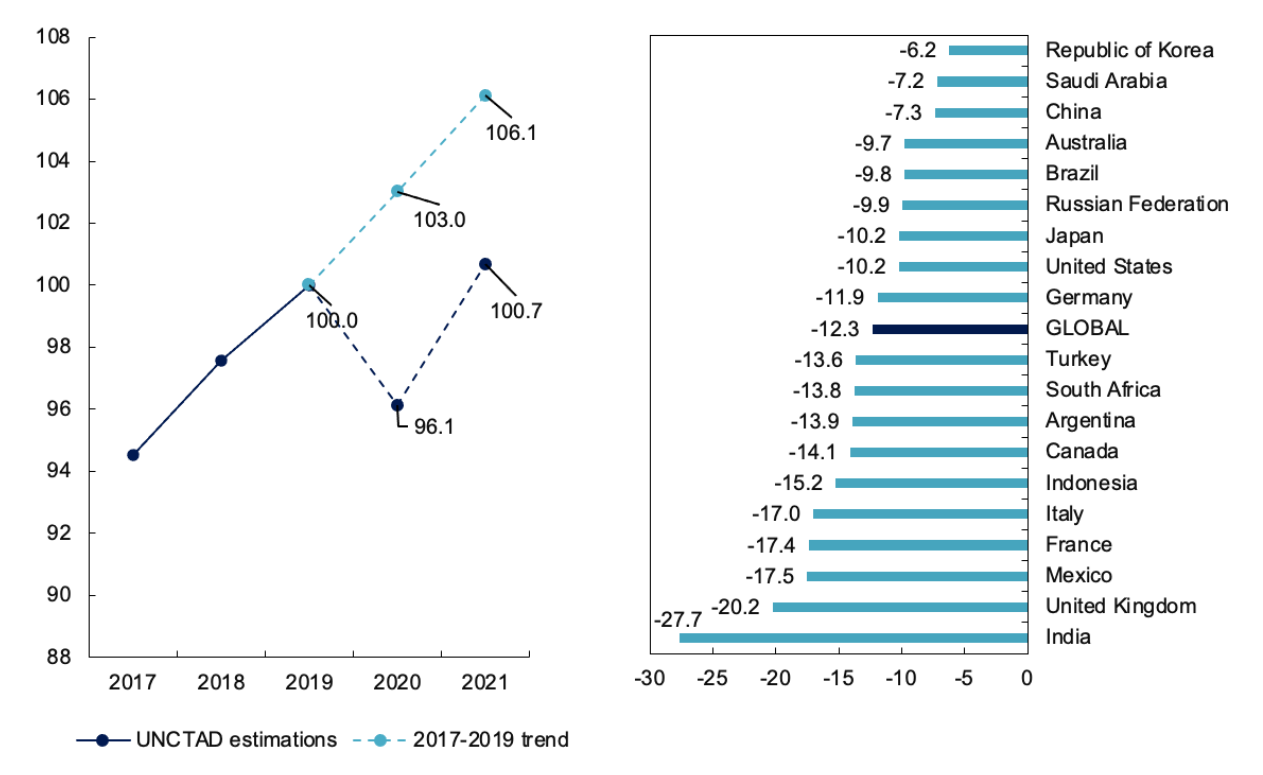

But this will still leave the global economy over $10 trillion short of where it could have been by the end of 2021 if it had stayed on the pre-pandemic trend (Figure 1) and with persistent worries about the reality behind the rhetoric of a more resilient future.

“A misguided return to austerity after a deep and destructive recession is the main risk to our global outlook,” says the report, Out of the frying pan …Into the fire?, published on 18 March as an update to UNCTAD’s Trade and Development Report 2020.

Figure 1: (left) World output level, 2017-2021 (2019 = 100); (right) Accumulated real income loss relative to pre-Covid-19 trend, 2020-2021 (% of GDP)

Source: UNCTAD secretariat calculations, based on official data and estimates generated by United Nations Global Policy Model.

“V” is for vulnerable

The brunt of the hit to the global economy is being felt in developing countries with limited fiscal space, tightening balance of payments constraints and inadequate international support, according to UNCTAD. And while all regions will see a turnaround this year, potential downside health and economic risks could still produce slippages.

Looking further ahead, the report says outdated economic dogmas, weak multilateral cooperation and a widespread reluctance to tackle the problems of inequality, indebtedness and insufficient investment – all worsening thanks to COVID-19.

It suggests that, without a change of course, the new normal for many will be an unbalanced recovery, vulnerability to further shocks and persistent economic insecurity.

Describing 2020 as an “annus horribilis”, the report acknowledges that things could have been worse.

A combination of preemptive Central Bank action to avoid a financial meltdown, swift and sizeable relief packages in advanced countries, a bounce-back in capital flows and commodity prices and the unprecedented fast-tracking of vaccine development all helped to avoid an even more vicious deflationary spiral taking hold.

However, the impact of these actions has been uneven, with K-shaped recoveries emerging within and across countries. Developing countries have experienced some of the largest personal income drops relative to GDP.

In countries where poverty levels are already high and large parts of the labour force are working in informal jobs, the immediate impact of even a small downturn in economic activity can be devastating. The World Bank estimates a quarter of a billion more people will slide into poverty (on a $3.20 daily benchmark) as a result of the pandemic.

International cooperation wanting

Despite the scale of the global health and economic crisis, international cooperation has fallen well short of what is needed.

The report compares the $12 billion of suspended debt servicing (for the year June 2020 to June 2021) for the 46 countries participating in the G20’s Debt Service Suspension Initiative (DSSI) to the $80 billion in debt service payments in 2019 by the 73 eligible DSSI countries and over a trillion dollars for all developing countries.

Equally, the refusal by advanced countries to support a waiver on trade-related aspects of intellectual property rights (TRIPS) at the World Trade Organization to help boost vaccine availability has signalled a priority of profits over people in the fight against the pandemic.

The global recovery that began in the third quarter of 2020 is expected to continue through 2021, albeit with a good deal of unevenness and unpredictability, reflecting epidemiological, policy and coordination uncertainties.

The report sees a misguided return to austerity, after a deep and destructive recession, as the main risk to its global outlook, especially in the context of fractured labour markets and deregulated financial markets in advanced economies.

But even barring an immediate return of austerity, the report notes, it will take more than one year for output and employment to return to their pre-COVID-19 levels in most countries with employment, income inequality and public welfare over the medium term depending on the evolution of policy responses.

The report warns, however, that COVID-19 will likely have lasting economic, as well as health consequences, which will require continued government support.

Old habits die hard

The report sees signs that emerging growth strategies post COVID-19 across the world are reverting to their pre-crisis norm, with an undue emphasis on exports in parts of east Asia and western Europe, loose monetary policy and asset-fuelled consumption in the US, and reliance on private capital inflows and commodity exports in Africa and Latin America.

The $1.9 trillion stimulus package in the US is grounds for encouragement. However, while the package contains large cash transfers, there is much less direct spending on consumption and investment, which would offer the safest route to aggregate demand expansion and a green transition. This makes the full effect of the package uncertain.

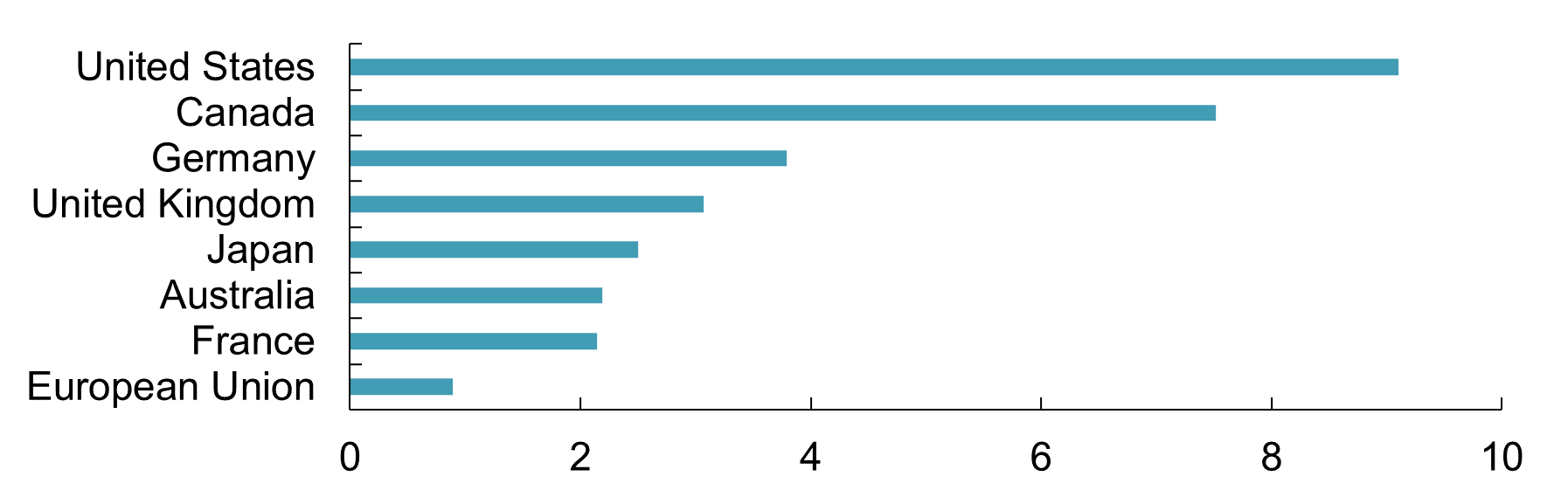

More troubling, according to the report, is that other advanced countries are lagging far behind (Figure 2).

There are also signs that the new US administration is extending its efforts to the multilateral level, endorsing a $500 billion issuance of new special drawing rights to support global liquidity at the upcoming G20 meeting, previously blocked by the Trump administration.

This is a welcome move but, according to the report, the scale of the debt threat, particularly for developing countries, cannot be reduced without debt forgiveness and the adoption of a functioning debt workout mechanism.

Figure 2: Estimated fiscal stimulus measures, select advanced economies, third quarter 2020 through fourth quarter 2021 (% of GDP)

Source: UNCTAD secretariat calculations based on national sources. Note: Fiscal estimates are based on above-the-line fiscal spending and tax stimulus measures. Accelerated spending and short-term deferral measures, i.e. tax payments deferred from one quarter or month to the next, are not included in these estimates.

The report concludes that tackling the mutually reinforcing trends of rising inequality, mounting debt distress, detached financial markets and growing market power of large corporations reluctant to reinvest their profits in building productive capacities will require more than a one-shot economic stimulus.

It calls for a more wholesale rewriting of the rules of the economic game if the mistakes of the 2009 financial crisis are not to be repeated and the goal of an inclusive, sustainable and resilient global economy realized by 2030.

OTTAWA – Canada’s unemployment rate held steady at 6.5 per cent last month as hiring remained weak across the economy.

Statistics Canada’s labour force survey on Friday said employment rose by a modest 15,000 jobs in October.

Business, building and support services saw the largest gain in employment.

Meanwhile, finance, insurance, real estate, rental and leasing experienced the largest decline.

Many economists see weakness in the job market continuing in the short term, before the Bank of Canada’s interest rate cuts spark a rebound in economic growth next year.

Despite ongoing softness in the labour market, however, strong wage growth has raged on in Canada. Average hourly wages in October grew 4.9 per cent from a year ago, reaching $35.76.

Friday’s report also shed some light on the financial health of households.

According to the agency, 28.8 per cent of Canadians aged 15 or older were living in a household that had difficulty meeting financial needs – like food and housing – in the previous four weeks.

That was down from 33.1 per cent in October 2023 and 35.5 per cent in October 2022, but still above the 20.4 per cent figure recorded in October 2020.

People living in a rented home were more likely to report difficulty meeting financial needs, with nearly four in 10 reporting that was the case.

That compares with just under a quarter of those living in an owned home by a household member.

Immigrants were also more likely to report facing financial strain last month, with about four out of 10 immigrants who landed in the last year doing so.

That compares with about three in 10 more established immigrants and one in four of people born in Canada.

This report by The Canadian Press was first published Nov. 8, 2024.

The Canadian Institute for Health Information says health-care spending in Canada is projected to reach a new high in 2024.

The annual report released Thursday says total health spending is expected to hit $372 billion, or $9,054 per Canadian.

CIHI’s national analysis predicts expenditures will rise by 5.7 per cent in 2024, compared to 4.5 per cent in 2023 and 1.7 per cent in 2022.

This year’s health spending is estimated to represent 12.4 per cent of Canada’s gross domestic product. Excluding two years of the pandemic, it would be the highest ratio in the country’s history.

While it’s not unusual for health expenditures to outpace economic growth, the report says this could be the case for the next several years due to Canada’s growing population and its aging demographic.

Canada’s per capita spending on health care in 2022 was among the highest in the world, but still less than countries such as the United States and Sweden.

The report notes that the Canadian dental and pharmacare plans could push health-care spending even further as more people who previously couldn’t afford these services start using them.

This report by The Canadian Press was first published Nov. 7, 2024.

Canadian Press health coverage receives support through a partnership with the Canadian Medical Association. CP is solely responsible for this content.

As Canadians wake up to news that Donald Trump will return to the White House, the president-elect’s protectionist stance is casting a spotlight on what effect his second term will have on Canada-U.S. economic ties.

Some Canadian business leaders have expressed worry over Trump’s promise to introduce a universal 10 per cent tariff on all American imports.

A Canadian Chamber of Commerce report released last month suggested those tariffs would shrink the Canadian economy, resulting in around $30 billion per year in economic costs.

More than 77 per cent of Canadian exports go to the U.S.

Canada’s manufacturing sector faces the biggest risk should Trump push forward on imposing broad tariffs, said Canadian Manufacturers and Exporters president and CEO Dennis Darby. He said the sector is the “most trade-exposed” within Canada.

“It’s in the U.S.’s best interest, it’s in our best interest, but most importantly for consumers across North America, that we’re able to trade goods, materials, ingredients, as we have under the trade agreements,” Darby said in an interview.

“It’s a more complex or complicated outcome than it would have been with the Democrats, but we’ve had to deal with this before and we’re going to do our best to deal with it again.”

American economists have also warned Trump’s plan could cause inflation and possibly a recession, which could have ripple effects in Canada.

It’s consumers who will ultimately feel the burden of any inflationary effect caused by broad tariffs, said Darby.

“A tariff tends to raise costs, and it ultimately raises prices, so that’s something that we have to be prepared for,” he said.

“It could tilt production mandates. A tariff makes goods more expensive, but on the same token, it also will make inputs for the U.S. more expensive.”

A report last month by TD economist Marc Ercolao said research shows a full-scale implementation of Trump’s tariff plan could lead to a near-five per cent reduction in Canadian export volumes to the U.S. by early-2027, relative to current baseline forecasts.

Retaliation by Canada would also increase costs for domestic producers, and push import volumes lower in the process.

“Slowing import activity mitigates some of the negative net trade impact on total GDP enough to avoid a technical recession, but still produces a period of extended stagnation through 2025 and 2026,” Ercolao said.

Since the Canada-United States-Mexico Agreement came into effect in 2020, trade between Canada and the U.S. has surged by 46 per cent, according to the Toronto Region Board of Trade.

With that deal is up for review in 2026, Canadian Chamber of Commerce president and CEO Candace Laing said the Canadian government “must collaborate effectively with the Trump administration to preserve and strengthen our bilateral economic partnership.”

“With an impressive $3.6 billion in daily trade, Canada and the United States are each other’s closest international partners. The secure and efficient flow of goods and people across our border … remains essential for the economies of both countries,” she said in a statement.

“By resisting tariffs and trade barriers that will only raise prices and hurt consumers in both countries, Canada and the United States can strengthen resilient cross-border supply chains that enhance our shared economic security.”

This report by The Canadian Press was first published Nov. 6, 2024.