(Bloomberg) — The global economy is suffering from a “disequilibrium phase” marked with unfavorable growth and inflation, and a worsening from here “cannot be ruled out,” according to Singapore’s central bank.

“In the quarters ahead, there is a risk that elevated inflation could lead to even tighter financial conditions, which could in turn weigh on already weakening economic activity,” the Monetary Authority of Singapore said in its biannual Macroeconomic Review published Thursday.

“The pullback in household and business spending, together with a further tightening in financial conditions, could potentially interact with existing vulnerabilities in the financial system, and exacerbate the economic downturn,” according to the report.

The trade-reliant city-state’s latest outlook on the local and global economy reflects persistent inflation and lingering growth worries amid increasingly uncertain geopolitics. While the global economy should avert a full-blown recession, things could get worse before they get better, and 2023 is seen as a painful year with activity slowing “sharply” in the US in the first half.

“Given where inflation is, a slowdown in the global economy is not altogether a bad thing,” MAS Managing Director Ravi Menon told Bloomberg Television this week. “It’s a good way to relieve those inflationary pressures — provided the slowdown is mild, short, and shallow.”

Singapore Central Bank Chief Urges Restraint on FX Intervention

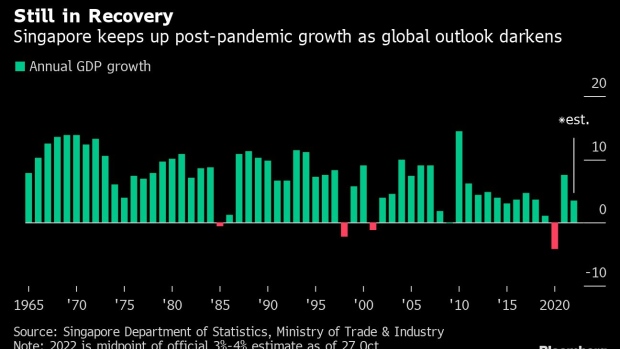

The MAS reiterated its forecast for 3%-4% growth in Singapore this year and cited “below-trend” economic activity in 2023. A specific forecast for 2023 is due at the final third-quarter GDP release next month. The city-state is seeing further post-Covid healing in industries that benefit from border reopening, while its critical electronics sector has slipped into a “consolidation phase.”

Singapore is also not immune to the heavy price pressures that weigh on much of the world, prompting the MAS to tighten monetary policy settings for a fifth time since October 2021.

Core inflation, the MAS’s preferred gauge that’s been accelerating near a 14-year high, should come in around 4% this year and between 3.5%-4.5% in 2023, the central bank said. It would stay elevated in the first half of next year before “moderating more discernibly” in late 2023 amid demand softening, the MAS reiterated.

The MAS review also included a study done in collaboration with the ASEAN+3 Macroeconomic Research Office on the drivers of regional inflation. Global factors, especially world energy costs, weigh heavily on price growth, while inflation expectations “appear to have been largely well-anchored since 2000, perhaps reflecting greater central bank credibility in the region after the Asian Financial Crisis,” the study found.

–With assistance from Kevin Varley.

©2022 Bloomberg L.P.