In spite of three months of economic free fall due to COVID-19, the Toronto real estate market seems to be returning to its pre-pandemic vigour.

Click on the video below to watch my update this – recap follows below. As always, I welcome your questions and comments at askjohn@movesmartly.com

[embedded content]

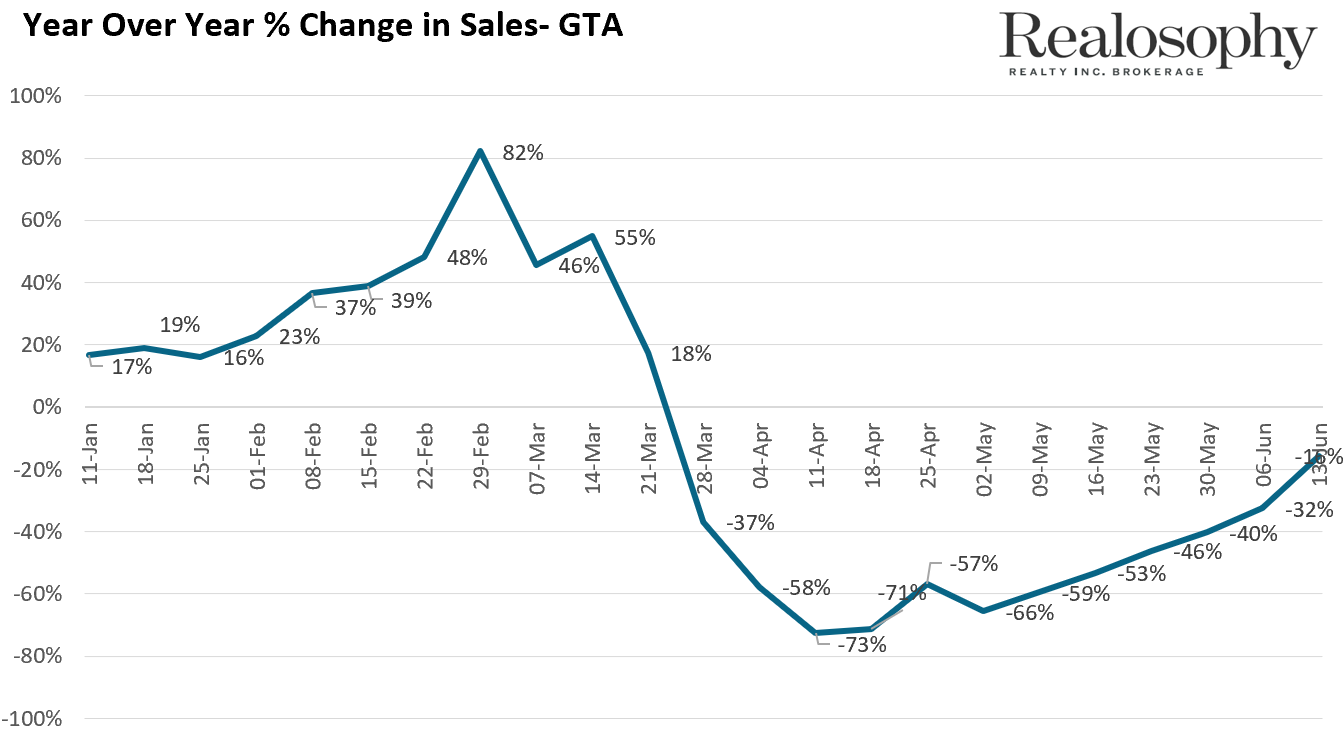

Sales are down 16% compared to last year but you can see from the chart below that every week they keep improving and are getting close to last year’s volumes.

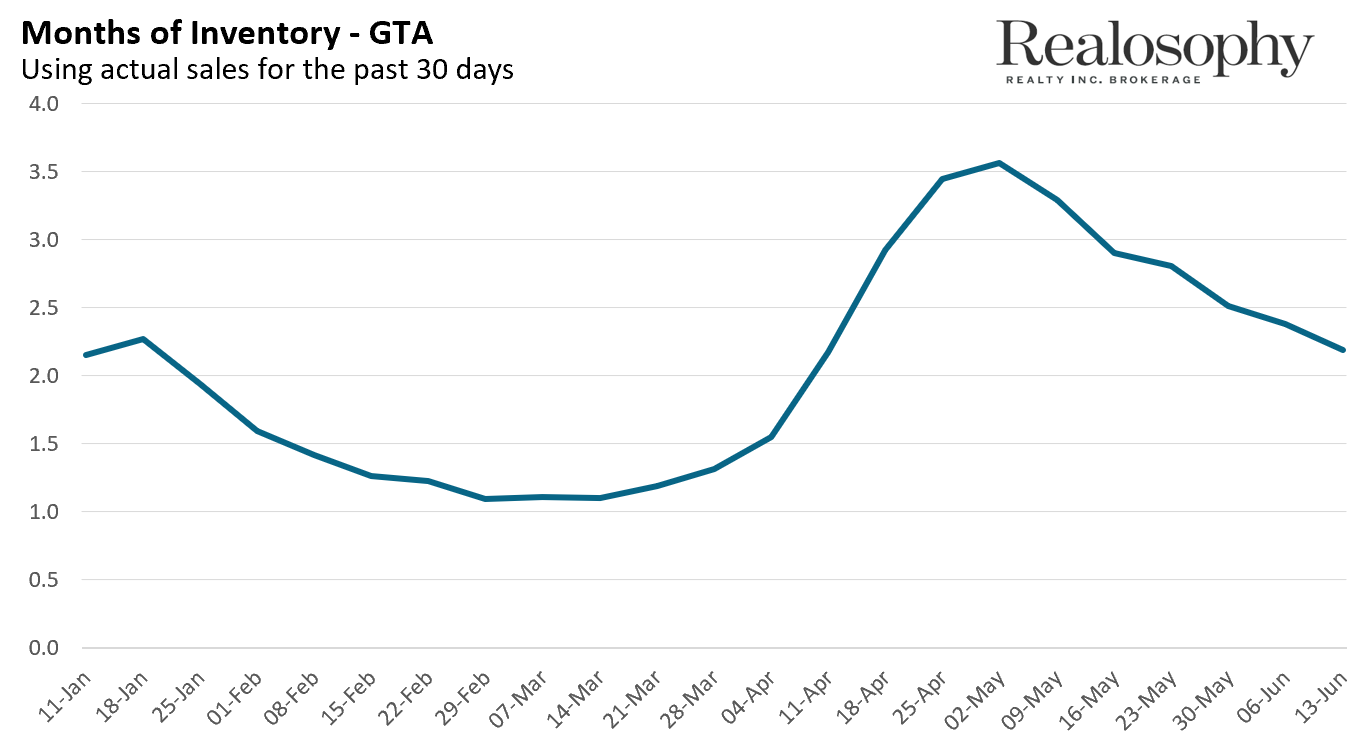

The Months of Inventory (MOI) which measures the number of homes on the market relative to the number of sales also keeps falling – which means every week that passes the number of available homes for buyers to choose from is declining.

What does this look like on the ground? More bidding wars, homes selling faster and with far more competition.

This of course does not mean every home is getting 10 offers and selling in 3 days. As always, there are some segments of the market that are slower than others. But as a whole the market is quite competitive.

Which of course raises an important question, why is the real estate market booming when the unemployment rate is at 14%?

History has shown us that housing markets usually cool down when the unemployment rate increases. This makes sense. With an increase in the number of people loosing their jobs fewer buyers can afford to buy homes and more owners usually need to sell their homes when they can no longer afford their mortgage after a prolonged period of unemployment.

So why is the opposite happening?

Some people are pointing to the very low interest rates – around 2% for a 5 year mortgage – as the cause for this surge in demand. But low rates don’t create demand. If you lost your job over the past 2 months you’re not going to suddenly jump back into the market and buy a home because rates are lower – you can’t get a mortgage without a job.

The more likely explanation is that the vast majority of jobs that have been lost in Canada were in lower paying front line service jobs. Many of the buyers our agents are working with have not been impacted by the recent job losses. They are primarily in jobs where working from home is an option so have not seen a loss to their income.

So how will the housing market progress from here?

I expect the summer to remain very competitive and the only thing that might help cool the competition is a spike in new listings.

As for the fall market, there are still two main risks on the horizon. Firstly, when all the government support for businesses and individuals who lost their jobs comes to an end, only then will we know how many households are impacted and have permanently lost their income as a result of this crisis.

Secondly, households who have deferred their mortgage payments are going to see their deferrals come to an end this fall.

But while I was very concerned about the fall market about a month ago, I’m a bit less concerned today for a couple of reasons. As businesses open up, I expect household spending to increase and more and more businesses to start making money again. I don’t think things will be back to normal, but I do not think they will be worse than they were a month ago. The economy will start to recover which means it’s unlikely for demand to be lower tomorrow than there is today.

There may be some tenants and homeowners who are unable to pay their rent or mortgage after all the government support comes to an end, but I’m not convinced that this alone is enough to put downward pressure on home prices. Anecdotally, I’m hearing that many of the households deferring their mortgages today are doing this to be cautious, not because they can’t afford their mortgage payments.

The one big unknown of course is if we see a second COVID-19 wave that is worse than the first, which would be additional stress on an already stressed healthcare system and economy. It’s hard to imagine what things will look like if that does happen. The best we can do for now it to monitor developments closely – stay tuned.

John Pasalis is President of Realosophy Realty,a Toronto real estate brokerage which uses data analysis to advise residential real estate buyers, sellers and investors.

A specialist in real estate data analysis, John’s research focuses on unlocking micro trends in the Greater Toronto Area real estate market. His research has been utilized by the Bank of Canada, the Canadian Mortgage and Housing Corporation (CMHC) and the International Monetary Fund (IMF).

HALIFAX – A village of tiny homes is set to open next month in a Halifax suburb, the latest project by the provincial government to address homelessness.

Located in Lower Sackville, N.S., the tiny home community will house up to 34 people when the first 26 units open Nov. 4.

Another 35 people are scheduled to move in when construction on another 29 units should be complete in December, under a partnership between the province, the Halifax Regional Municipality, United Way Halifax, The Shaw Group and Dexter Construction.

The province invested $9.4 million to build the village and will contribute $935,000 annually for operating costs.

Residents have been chosen from a list of people experiencing homelessness maintained by the Affordable Housing Association of Nova Scotia.

They will pay rent that is tied to their income for a unit that is fully furnished with a private bathroom, shower and a kitchen equipped with a cooktop, small fridge and microwave.

The Atlantic Community Shelters Society will also provide support to residents, ranging from counselling and mental health supports to employment and educational services.

This report by The Canadian Press was first published Oct. 24, 2024.

Housing affordability is a key issue in the provincial election campaign in British Columbia, particularly in major centres.

Here are some statistics about housing in B.C. from the Canada Mortgage and Housing Corporation’s 2024 Rental Market Report, issued in January, and the B.C. Real Estate Association’s August 2024 report.

Average residential home price in B.C.: $938,500

Average price in greater Vancouver (2024 year to date): $1,304,438

Average price in greater Victoria (2024 year to date): $979,103

Average price in the Okanagan (2024 year to date): $748,015

Average two-bedroom purpose-built rental in Vancouver: $2,181

Average two-bedroom purpose-built rental in Victoria: $1,839

Average two-bedroom purpose-built rental in Canada: $1,359

Rental vacancy rate in Vancouver: 0.9 per cent

How much more do new renters in Vancouver pay compared with renters who have occupied their home for at least a year: 27 per cent

This report by The Canadian Press was first published Oct. 17, 2024.

VANCOUVER – Voters along the south coast of British Columbia who have not cast their ballots yet will have to contend with heavy rain and high winds from an incoming atmospheric river weather system on election day.

Environment Canada says the weather system will bring prolonged heavy rain to Metro Vancouver, the Sunshine Coast, Fraser Valley, Howe Sound, Whistler and Vancouver Island starting Friday.

The agency says strong winds with gusts up to 80 kilometres an hour will also develop on Saturday — the day thousands are expected to go to the polls across B.C. — in parts of Vancouver Island and Metro Vancouver.

Wednesday was the last day for advance voting, which started on Oct. 10.

More than 180,000 voters cast their votes Wednesday — the most ever on an advance voting day in B.C., beating the record set just days earlier on Oct. 10 of more than 170,000 votes.

Environment Canada says voters in the area of the atmospheric river can expect around 70 millimetres of precipitation generally and up to 100 millimetres along the coastal mountains, while parts of Vancouver Island could see as much as 200 millimetres of rainfall for the weekend.

An atmospheric river system in November 2021 created severe flooding and landslides that at one point severed most rail links between Vancouver’s port and the rest of Canada while inundating communities in the Fraser Valley and B.C. Interior.

This report by The Canadian Press was first published Oct. 17, 2024.