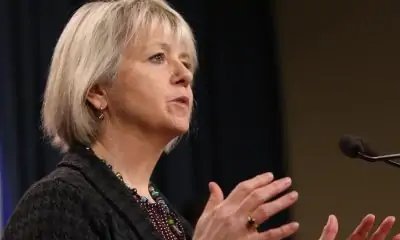

Shinzo Abe’s policies did not succeed in pushing up real wages, as deflation gave way to rising prices.GIAN EHRENZELLER/The Associated Press

Shinzo Abe often framed his economic vision as a policy bundle of “three arrows”: an integration of fiscal stimulus, loose money and structural reform that together would snap Japan out of its prolonged stagnation.

In doing so, the former prime minister drew on the Japanese folk story of three brothers, each given an arrow. Separately, their arrows could be easily snapped; together, the arrows – and the brothers – were unbreakable.

Mr. Abe, who was assassinated on Friday, meant the three-arrows reference as an illustration of the irrefutable logic of what came to be known as Abenomics. That parable did turn out to be strikingly relevant, but not in the way he would have hoped.

Two of his arrows, launched in 2013, struck home. Massive fiscal stimulus did boost Japan’s growth. Negative interest rates and quantitative easing finally vanquished the persistent deflation brought on by the real estate collapse of the 1990s. But the third arrow fell short, with the Abe government failing to fully counteract the productivity-sapping effects of an aging population. And, as the parable implies, two out of three arrows are not enough – a lesson other countries, including Canada, should heed.

According to David Edgington, a professor emeritus at the University of British Columbia and former director of the school’s Centre for Japanese Research, Mr. Abe’s policies did not succeed in pushing up real wages, as deflation gave way to rising prices.

“While inflation ticked up a bit, most of the extra cash put into government bonds by the Bank of Japan went into the stock market,” he said, adding that the country became a much more unequal society under Abenomics.

Still, there’s no doubt that Mr. Abe faced a monumental economic challenge when he returned to office in 2012. Japan’s economy was at a standstill in 2011. Prices were falling, with a deflation rate of 0.27 per cent. And GDP growth had flat-lined at 0 per cent.

Against that backdrop, Mr. Abe sought to shock Japan’s economy back to life.

In the same way that he marketed his economic policy to the Japanese people by tapping the country’s folklore, Mr. Abe embraced Western-style showmanship to pitch the revival of Japan to the world: “Buy my Abenomics,” he exhorted during a speech at the New York Stock Exchange in 2013.

As a mix of economic-policy measures, Abenomics was in fact quite conventional. The idea of using monetary and fiscal policy levers to avoid deflation, while pursuing a promise of supply-side reforms aimed at shifting labour and capital into more productive areas of the economy, is hardly radical thinking in most developed countries.

Yet the policies marked an abrupt break from the Japanese economic orthodoxy that prevailed during the previous two decades before Mr. Abe began his second term. Most crucially, the Bank of Japan had long argued deflation was largely beyond its control, a by-product of an aging population, and that the best it could do was provide a supportive interest-rate environment while the government did the heavy lifting of boosting Japan’s real potential growth.

Under Abenomics and the Bank of Japan’s new governor, Haruhiko Kuroda, the central bank instead unleashed an era of unprecedented easing. It adopted, for the first time, an inflation target of 2 per cent. And it injected liquidity into the economy through quantitative easing, introduced negative interest rates and declared its willingness to let inflation overshoot its target. (All measures, incidentally, that many of the world’s large central banks eventually came to adopt.)

“For years you had reflationists in Japan banging on the walls and pointing to things that American and European economists were saying,with no success,” said Tobias Harris, a Washington-based Japan analyst and author of The Iconoclast, a biography of Mr. Abe published in 2020.

“Abe ended up being a vehicle for these outsiders who had been looking for someone who could carry their ideas about fighting deflation.”

By the time Mr. Abe stepped down in 2020, citing health issues, Abenomics had delivered decidedly mixed results to Japan’s economy.

Prices initially responded well to the Bank of Japan’s aggressive policies, with inflation reaching 3.7 per cent in 2014 as the country enjoyed record employment. However, a hike in Japan’s consumption tax that year caused spending to drop and tipped the country into recession. It also cost the government and central bank credibility in their fight against deflation. While inflation largely stayed positive prior to the pandemic, it never again hit the bank’s target, rarely lifting above 1 per cent.

Nor did the supply-side reforms promised by Abenomics amount to much. He did liberalize the country’s electricity market and resurrected the Trans-Pacific Partnership trade deal, but stopped short of deeper changes.

“Abe was able to offer lots of carrots to corporate Japan, but he was always reluctant to use sticks to try to encourage them to change their behaviour in ways that furthered his policy goals,” Mr. Harris said.

That said, Mr. Harris believes Abenomics brought about a lasting philosophical shift on the part of the Japanese government. On the global trade front, the country is willing to play a role as a leader in integration that it was not willing to before.

But Japan’s structural problems are hardly unique. Worries about deflation countered by massive fiscal and monetary stimulus. Persistently flaccid productivity growth, and mounting pressure from an aging population. That describes not only Japan, but Canada less than two years ago.

Deflation, at least, proved to be a fleeting concern, as inflation has surged in 2021 and this year. But productivity remains a central challenge for Canada, particularly as the baby boomers move fully into their retirement.

Trevor Kennedy, vice-president of trade and international policy at the Business Council of Canada, said every economy in the world, including our own, can learn from Japan’s experience with Abenomics.

“We actually should all be paying attention to Japan, including how it manages an aging population,” he said. “We all could be facing a similar future, certainly on the demographic side.”

In the most recent federal budget, the Canadian government painted a comforting picture of a long-term decline in the country’s debt burden. But that scenario is predicated on a sharp and enduring increase in productivity that, so far, is not buttressed by any major policy shift.

In an echo of Abenomics, the federal Liberals have run significant deficits since coming to office, continuing in 2022 and beyond, even though the economy is clearly overheating. For the moment, however, there’s no hint of the kind of broad-based tax increases that Japan brought in to tamp down its national debt.

Ottawa has boosted immigration goals and laid the foundation for national subsidized child care. Both of those measures should help to buoy the labour force, although their effect on productivity is less clear. On those two fronts, Canada has outpaced Japan.

But there is one arrow, at least, that is in flight in Japan, but still stuck in Canada’s quiver: a concerted push to keep older workers in the labour pool.

One of the first moves the federal Liberals made when entering office in 2015 was to cancel the planned gradual increase in the eligibility for federal old-age benefits to 67 from 65, starting in 2023. That policy would have both reduced fiscal pressures on Ottawa and encouraged older Canadians to remain in the workplace.

Japan, belatedly, is moving in the opposite direction. The official retirement age for government employees will start to gradually rise to 65 from 60 by 2031, starting next year. The retirement age for private-sector workers is effectively being moved up to 70, and there are plans to pare back benefits for those aged 60 to 64.

All of those changes are happening relatively quickly. Workers in their 50s and 60s, not just those at the start of their working life, are seeing the terms of their retirement rewritten. That could be the most fundamental lesson from Abenomics: The longer the delay, the greater the pain.

Your time is valuable. Have the Top Business Headlines newsletter conveniently delivered to your inbox in the morning or evening. Sign up today.

OTTAWA – Canada’s unemployment rate held steady at 6.5 per cent last month as hiring remained weak across the economy.

Statistics Canada’s labour force survey on Friday said employment rose by a modest 15,000 jobs in October.

Business, building and support services saw the largest gain in employment.

Meanwhile, finance, insurance, real estate, rental and leasing experienced the largest decline.

Many economists see weakness in the job market continuing in the short term, before the Bank of Canada’s interest rate cuts spark a rebound in economic growth next year.

Despite ongoing softness in the labour market, however, strong wage growth has raged on in Canada. Average hourly wages in October grew 4.9 per cent from a year ago, reaching $35.76.

Friday’s report also shed some light on the financial health of households.

According to the agency, 28.8 per cent of Canadians aged 15 or older were living in a household that had difficulty meeting financial needs – like food and housing – in the previous four weeks.

That was down from 33.1 per cent in October 2023 and 35.5 per cent in October 2022, but still above the 20.4 per cent figure recorded in October 2020.

People living in a rented home were more likely to report difficulty meeting financial needs, with nearly four in 10 reporting that was the case.

That compares with just under a quarter of those living in an owned home by a household member.

Immigrants were also more likely to report facing financial strain last month, with about four out of 10 immigrants who landed in the last year doing so.

That compares with about three in 10 more established immigrants and one in four of people born in Canada.

This report by The Canadian Press was first published Nov. 8, 2024.

The Canadian Institute for Health Information says health-care spending in Canada is projected to reach a new high in 2024.

The annual report released Thursday says total health spending is expected to hit $372 billion, or $9,054 per Canadian.

CIHI’s national analysis predicts expenditures will rise by 5.7 per cent in 2024, compared to 4.5 per cent in 2023 and 1.7 per cent in 2022.

This year’s health spending is estimated to represent 12.4 per cent of Canada’s gross domestic product. Excluding two years of the pandemic, it would be the highest ratio in the country’s history.

While it’s not unusual for health expenditures to outpace economic growth, the report says this could be the case for the next several years due to Canada’s growing population and its aging demographic.

Canada’s per capita spending on health care in 2022 was among the highest in the world, but still less than countries such as the United States and Sweden.

The report notes that the Canadian dental and pharmacare plans could push health-care spending even further as more people who previously couldn’t afford these services start using them.

This report by The Canadian Press was first published Nov. 7, 2024.

Canadian Press health coverage receives support through a partnership with the Canadian Medical Association. CP is solely responsible for this content.

As Canadians wake up to news that Donald Trump will return to the White House, the president-elect’s protectionist stance is casting a spotlight on what effect his second term will have on Canada-U.S. economic ties.

Some Canadian business leaders have expressed worry over Trump’s promise to introduce a universal 10 per cent tariff on all American imports.

A Canadian Chamber of Commerce report released last month suggested those tariffs would shrink the Canadian economy, resulting in around $30 billion per year in economic costs.

More than 77 per cent of Canadian exports go to the U.S.

Canada’s manufacturing sector faces the biggest risk should Trump push forward on imposing broad tariffs, said Canadian Manufacturers and Exporters president and CEO Dennis Darby. He said the sector is the “most trade-exposed” within Canada.

“It’s in the U.S.’s best interest, it’s in our best interest, but most importantly for consumers across North America, that we’re able to trade goods, materials, ingredients, as we have under the trade agreements,” Darby said in an interview.

“It’s a more complex or complicated outcome than it would have been with the Democrats, but we’ve had to deal with this before and we’re going to do our best to deal with it again.”

American economists have also warned Trump’s plan could cause inflation and possibly a recession, which could have ripple effects in Canada.

It’s consumers who will ultimately feel the burden of any inflationary effect caused by broad tariffs, said Darby.

“A tariff tends to raise costs, and it ultimately raises prices, so that’s something that we have to be prepared for,” he said.

“It could tilt production mandates. A tariff makes goods more expensive, but on the same token, it also will make inputs for the U.S. more expensive.”

A report last month by TD economist Marc Ercolao said research shows a full-scale implementation of Trump’s tariff plan could lead to a near-five per cent reduction in Canadian export volumes to the U.S. by early-2027, relative to current baseline forecasts.

Retaliation by Canada would also increase costs for domestic producers, and push import volumes lower in the process.

“Slowing import activity mitigates some of the negative net trade impact on total GDP enough to avoid a technical recession, but still produces a period of extended stagnation through 2025 and 2026,” Ercolao said.

Since the Canada-United States-Mexico Agreement came into effect in 2020, trade between Canada and the U.S. has surged by 46 per cent, according to the Toronto Region Board of Trade.

With that deal is up for review in 2026, Canadian Chamber of Commerce president and CEO Candace Laing said the Canadian government “must collaborate effectively with the Trump administration to preserve and strengthen our bilateral economic partnership.”

“With an impressive $3.6 billion in daily trade, Canada and the United States are each other’s closest international partners. The secure and efficient flow of goods and people across our border … remains essential for the economies of both countries,” she said in a statement.

“By resisting tariffs and trade barriers that will only raise prices and hurt consumers in both countries, Canada and the United States can strengthen resilient cross-border supply chains that enhance our shared economic security.”

This report by The Canadian Press was first published Nov. 6, 2024.

:format(jpeg)/cloudfront-us-east-1.images.arcpublishing.com/tgam/33IIPE63AVGGJAGP5AQ4ZEJN5E.jpg)