This

post is part of CoinDesk’s 2019 Year in Review, a collection of 100+ op-eds,

interviews and takes on the state of blockchain and the world. Scott Army is

the founder and CEO of digital asset manager Vision Hill Group. The following

is a summary of the report: “An Institutional Take on the 2019/2020 Digital Asset Market”.

No. 1: There’s bitcoin, and then there’s everything else.

The

industry is currently segmented into two main categories: Bitcoin and

everything else. “Everything else” includes: Web3 innovation, Decentralized

Finance (“DeFi”), Decentralized Autonomous Organizations, smart contract

platforms, security tokens, digital identity, data privacy, gaming, enterprise

blockchain or distributed ledger technology, and much more.

Non-crypto natives are seldom aware that there are multiple blockchains. Bitcoin, by virtue of it being the first blockchain network brought into the mainstream and by being the largest digital asset by market capitalization, is often the first stop for many newcomers and likely will continue to be for the foreseeable future.

No. 2: Bitcoin is perhaps market beta, for now.

In traditional equity markets, beta is defined as a measure of volatility, or unsystematic risk an individual stock possesses relative to the systematic risk of the market as a whole. The difficulty in defining “market beta” in a space like digital assets is that there is no consensus for a market proxy like the S&P 500 or Dow Jones. Since the space is still very early in its development, and bitcoin has dominant market share (~68 percent at the time of writing), bitcoin is often viewed as the obvious choice for beta, despite the drawbacks of defining “market beta” as a single asset with idiosyncratic tendencies.

Bitcoin’s

size and its institutionalization (futures, options, custody, and clear

regulatory status as a commodity), have enabled it to be an attractive first

step for allocators looking to get exposure (both long and short) to the

digital asset market, suggesting that bitcoin is perhaps positioned to be digital

asset market beta, for now.

No. 3: Despite slow conversion, substantial progress was made on growing institutional investor interest in 2019.

Education,

education, education. Blockchain

technology and digital assets represent an extraordinarily complex asset class

– one that requires a non-trivial time commitment to undergo a proper learning

curve. While handfuls of institutions have already started to invest in the

space, a very small amount of institutional capital has actually made it in

(relative to the broader institutional landscape), gauged by the size of the

asset class and the public market trading volumes. This has led many to

repeatedly ask: “when will the herd actually come?”

The reality is that

institutional investors are still learning – slowly getting comfortable – and

this process will continue to take time. Despite educational progress through 2019, some

institutions are wondering if it’s too early to be investing in this space, and

whether they can potentially get involved in investing in digital assets in the

future and still generate positive returns, but in ways that are de-risked

relative to today.

Despite a few other

challenges imposed on larger institutional allocators with respect to investing

in digital assets, true believers inside these large organizations are

emerging, and the processes for forming a digital asset strategy are either

getting started or already underway.

No. 4: Long simplicity, short complexity

Another trend we

observed emerge this year was a shift away from complexity and toward

simplicity. We saw significant growth in simple,

passive, low-cost structures to capture beta. With the lowest-friction investor

adoption focused on the largest liquid asset in the space – bitcoin – the

proliferation of single asset vehicles has increased. These private vehicles are a result of

delayed approval of an official bitcoin ETF by the SEC.

In addition to the Grayscale

Bitcoin Trust, other bitcoin-focused

products this year include the launch of Bakkt, the launch of Galaxy Digital’s two new

bitcoin funds, Fidelity’s

bitcoin product rollout, TD Ameritrade’s bitcoin trading service on Nasdaq via its brokerage platform, 3iQ’s

recent favorable ruling for a bitcoin fund and Stone Ridge Asset Management’s recent SEC approval for its NYDIG Bitcoin Strategy Fund, based on cash-settled bitcoin

futures.

We also observed a growing

institutional appetite for simpler hedge fund and venture fund structures. For

the last several years, many fundamental-focused crypto-native hedge funds

operated hybrid structures with the use of side-pockets that enabled a barbell

strategy approach to investing in both the public and private digital asset

markets. These hedge funds tend to have

longer lock-up periods – typically two or three years – and low liquidity.

While this may be attractive from an opportunistic perspective, the reality is it’s

quite complicated from an institutional perspective for reporting purposes.

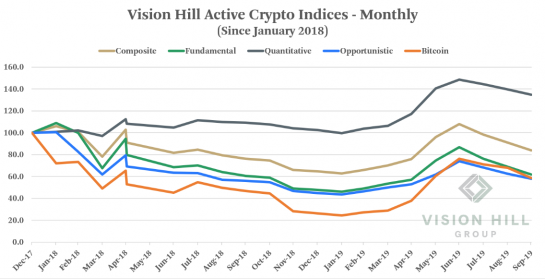

No. 5: Active management’s been challenged, but differentiated sources of alpha are emerging.

For the year-to-date period ended Q3 2019, active managers were collectively up 30 percent on an absolute return basis according to our tracking of approximately 50 institutional-quality funds, compared to bitcoin being up 122 percent over the same time period.

Bitcoin’s performance this year, particularly in Q2 2019, has made it clear that its parabolic ascents challenge the ability of active managers to outperform bitcoin during the windows they occur. Active managers generally need to justify the fees they charge investors by outperforming their benchmark(s), which are often beta proxies, yet at the same time they need to avoid imprudent risk behavior that can potentially have swift and sizable negative effects on their portfolios.

Interestingly, active management performance from the beginning of 2018 consistently outperformed passively holding bitcoin (with the exception of “opportunistic” managers who also take advantage of yield and staking opportunities, as of May 2019). This is largely due to various risk management techniques used to mitigate the negative performance drawdowns experienced throughout the extended market sell-off in 2018.

Source: Vision Hill Group

Although 2019 has challenged the large-scale

success of these alpha strategies, they are nonetheless in the process of

proving themselves out through various market cycles, and we expect this to be

a growing theme in 2020.

No. 6: Token value accrual: Transitioning from subjective to objective

At the end of Q3 2019, according to dapp.com, there were 1,721 decentralized applications built on top of ethereum, with 604 of them actively used – more than any other blockchain. Ethereum also had 1.8 million total unique users, with just under 400,000 of them active – also more than any other blockchain. Yet, despite all this growing network activity, the value of ETH has remained largely flat throughout most of 2019 and is on track to end the year down approximately 10 percent at the time of writing (by comparison, BTC has nearly doubled in value over the same period). This begs the question: is ETH adequately capturing the economic value of the ethereum network’s activity, and DeFi in particular?

A new fundamental metric was introduced

earlier this year by Chris Burniske – the Network Value to Token

Value (“NVTV”) ratio – to ascertain whether the value of all assets anchored

into a platform can be greater than the value of the base platform’s asset.

The ETH NVTV ratio has steadily declined throughout the last few years. There are likely to be several reasons for this, but I think one theory summarizes it best: most applications and tokens built and issued atop ethereum may be parasitic. ETH token holders are paying for the security of all these applications and tokens, via the inflation rate that is currently given to the miners – dilution for ETH holders, but not for holders of ethereum-based tokens.

This is not a bullish or bearish

statement on ETH; rather it is an observation of early signs of network stack

value capture in the space.

No. 7: Money or not, software-powered collateral economies are here

Another trend we observed this year is a larger migration away from “cryptocurrencies” in an ideological currency (e.g., money/payment and a means of exchange) sense, and toward digital assets for financial applications and economic utility. A form of economic utility that took the stage this year is the notion of software-powered collateral economies. People generally want to hold assets with disinflationary or deflationary supply curves, because part of their promise is that they should store value well. Smart contracts enable us to program the characteristics of any asset, thus it is not irrational to assume that it’s only a matter of time until traditional collateral assets get digitized and put to economic use on blockchain networks.

The

benefit of digital collateral is that it can be liquid and economically

productive in its nature while at the same time serving its primary purpose (to

collateralize another asset), yet without possessing the risks of traditional

rehypothecation. If assets can be allocated for multiple purposes

simultaneously, with the risks appropriately managed, we should see more

liquidity, lower cost of borrowing, and more effective allocation of capital in

ways the traditional world may not be able to compete with.

No. 8: Network lifecycles: An established supply side meets a quiet but emerging demand side.

Supply side services in digital asset

networks are services provided by a third party to a decentralized network in

exchange for compensation allocated by that network. Examples include mining,

staking, validation, bonding, curation, node operation and more, done to help bootstrap

and grow these networks. Incentivizing the supply side is important in digital

assets to facilitate their growth early in their lifecycles, from initial fundraising

and distribution through the bootstrapping phase to eventual mainnet launches.

While there has been significant growth of this supply side of the equation in

2019 from funds, companies, and developers, the open question is how and when

demand for these services will pick up. Our view is that as developer

infrastructure continues to mature and activity begins to move “up the stack”

toward the application layer, more obvious manifestations of product-market fit

are likely to emerge with cleaner and simpler interfaces that will attract high

volumes of users in the process. In essence, it is important to build the

necessary infrastructure first (the supply side) to enable buy-in from the end

users of those services (the demand side).

No. 9: We are in the late innings of the smart contract wars.

While ethereum leads the space on adoption and moves closer to executing on its scalability initiatives, dozens of smart contract competitors fundraised in the market throughout 2018 and 2019 in an attempt to dethrone ethereum. A handful have formally launched their chains and operate in mainnet as of the end of 2019, while many others remain in testnet or have stalled in development.

What’s

been particularly interesting to observe is the accelerative pace of innovation

– not just technologically, but economically (incentive mechanisms) and

socially (community building) as well.

We expect many more smart contract competitors operating privately as of

Q4 2019 to launch their mainnets in 2020. Thus, given the incoming magnitude of

publicly observable experimentations throughout 2020, if a smart contract

platform does not launch in 2020, it is likely to become disadvantageously

positioned relative to the rest of the landscape as it relates to capturing

substantial developer mindshare and future users and creating defensible

network effects.

No. 10: Product-market fit is coming, if not already here

We don’t think human and financial capital would have

continued pouring into the digital asset space in such great magnitude over the

last several years if there wasn’t a focus on solving at least one very clear

problem. The questionable sustainability of modern monetary theory is one of

them, and Ray Dalio of Bridgerwater Associates has been quite vocal about it. Big Tech centralization is another. There are also growing

global concerns related to data privacy and identity. And let’s not forget

cybersecurity. The list goes on. We are at the tip of the iceberg as it

relates to the products and applications blockchain technology enables, and mainstream users will come with growing

manifestations of product-market fit. As more time and attention gets spent on

diagnosing problems and working on solutions, the industry will begin to

achieve its full potential. Facebook’s Libra and

Twitter’s Bluesky initiative confirm that as an industry we are heading in the

right direction.

A 2020 look ahead

We see 2020 shaping up to be one of the brightest years on record for the digital asset industry. To be clear, this is not a price forecast; if we exclusively measured the health of the industry from a fundamental progress perspective, by various accounts and measures we should have been in a raging bull market for the last two years, and that has not been the case. Rather, we expect 2020 to be a year of accelerated industry maturation.

Source: Vision Hill Group

Digital assets are still an emerging asset class with many quickly evolving narratives, trends, and investment strategies. It is important to note, that not all strategies are suitable for all investors. The size of allocations to each category will and should vary depending on the specific allocator’s type, risk tolerance, return expectations, liquidity needs, time horizon and other factors. What is encouraging is that as the asset class continues to grow and mature, the opacity slowly dissipates and clearly defined frameworks for evaluation will continue to emerge. This will hopefully lead to more informed investment decisions across the space. The future is bright for 2020 and beyond.

The leader in blockchain news, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CoinDesk is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups.

NEW YORK (AP) — Shares of Tesla soared Wednesday as investors bet that the electric vehicle maker and its CEO Elon Musk will benefit from Donald Trump’s return to the White House.

Tesla stands to make significant gains under a Trump administration with the threat of diminished subsidies for alternative energy and electric vehicles doing the most harm to smaller competitors. Trump’s plans for extensive tariffs on Chinese imports make it less likely that Chinese EVs will be sold in bulk in the U.S. anytime soon.

“Tesla has the scale and scope that is unmatched,” said Wedbush analyst Dan Ives, in a note to investors. “This dynamic could give Musk and Tesla a clear competitive advantage in a non-EV subsidy environment, coupled by likely higher China tariffs that would continue to push away cheaper Chinese EV players.”

Tesla shares jumped 14.8% Wednesday while shares of rival electric vehicle makers tumbled. Nio, based in Shanghai, fell 5.3%. Shares of electric truck maker Rivian dropped 8.3% and Lucid Group fell 5.3%.

Tesla dominates sales of electric vehicles in the U.S, with 48.9% in market share through the middle of 2024, according to the U.S. Energy Information Administration.

Subsidies for clean energy are part of the Inflation Reduction Act, signed into law by President Joe Biden in 2022. It included tax credits for manufacturing, along with tax credits for consumers of electric vehicles.

Musk was one of Trump’s biggest donors, spending at least $119 million mobilizing Trump’s supporters to back the Republican nominee. He also pledged to give away $1 million a day to voters signing a petition for his political action committee.

In some ways, it has been a rocky year for Tesla, with sales and profit declining through the first half of the year. Profit did rise 17.3% in the third quarter.

The U.S. opened an investigation into the company’s “Full Self-Driving” system after reports of crashes in low-visibility conditions, including one that killed a pedestrian. The investigation covers roughly 2.4 million Teslas from the 2016 through 2024 model years.

And investors sent company shares tumbling last month after Tesla unveiled its long-awaited robotaxi at a Hollywood studio Thursday night, seeing not much progress at Tesla on autonomous vehicles while other companies have been making notable progress.

TORONTO – Canada’s main stock index was up more than 100 points in late-morning trading, helped by strength in base metal and utility stocks, while U.S. stock markets were mixed.

The S&P/TSX composite index was up 103.40 points at 24,542.48.

In New York, the Dow Jones industrial average was up 192.31 points at 42,932.73. The S&P 500 index was up 7.14 points at 5,822.40, while the Nasdaq composite was down 9.03 points at 18,306.56.

The Canadian dollar traded for 72.61 cents US compared with 72.44 cents US on Tuesday.

The November crude oil contract was down 71 cents at US$69.87 per barrel and the November natural gas contract was down eight cents at US$2.42 per mmBTU.

The December gold contract was up US$7.20 at US$2,686.10 an ounce and the December copper contract was up a penny at US$4.35 a pound.

This report by The Canadian Press was first published Oct. 16, 2024.

TORONTO – Canada’s main stock index was up more than 200 points in late-morning trading, while U.S. stock markets were also headed higher.

The S&P/TSX composite index was up 205.86 points at 24,508.12.

In New York, the Dow Jones industrial average was up 336.62 points at 42,790.74. The S&P 500 index was up 34.19 points at 5,814.24, while the Nasdaq composite was up 60.27 points at 18.342.32.

The Canadian dollar traded for 72.61 cents US compared with 72.71 cents US on Thursday.

The November crude oil contract was down 15 cents at US$75.70 per barrel and the November natural gas contract was down two cents at US$2.65 per mmBTU.

The December gold contract was down US$29.60 at US$2,668.90 an ounce and the December copper contract was up four cents at US$4.47 a pound.

This report by The Canadian Press was first published Oct. 11, 2024.