US investors pulled huge sums from relatively expensive investment funds last year as the divide between cheap and expensive funds grew into a “chasm”, Morningstar analysis suggests.

The data is symptomatic of an increasingly laser-like focus by investors and their advisers on attempting to maximise returns by keeping costs to a minimum.

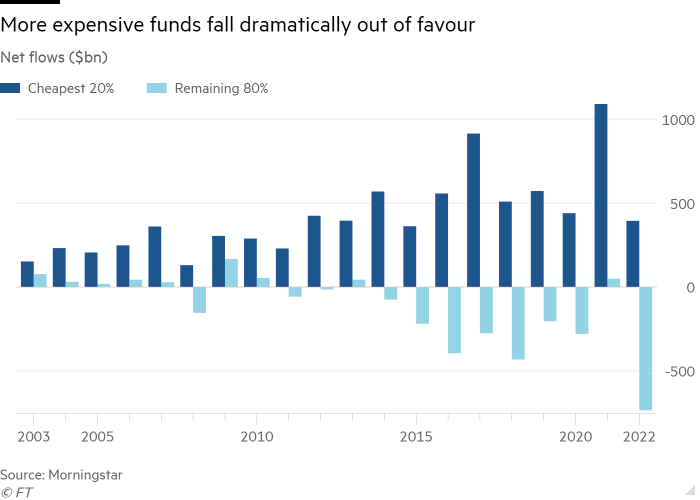

The most expensive 80 per cent of US-domiciled mutual and exchange traded funds — based on the asset-weighted average expense ratio — saw an unprecedented $734bn of collective net outflows last year, far in excess of the previous record of $431bn in 2018, according to Morningstar.

In sharp contrast, the 20 per cent of cheapest funds gathered $394bn of net new money, with the divide between the fortunes of the two camps exceeding $1.1tn.

“One of the biggest differences we saw year over year was a significant drop in assets in some of the pricier, more speculative strategies,” said Bryan Armour, director of passive strategies research, North America, at Morningstar.

Investors now appear to be getting even pickier, with the most expensive end of the cheapest 20 per cent of funds also starting to fall out of favour.

The cheapest 5 per cent of funds — a segment dominated by low-cost index-tracking ETFs — pulled in a net $519bn last year. Those in the 5-10 per cent category saw small net outflows, but $108bn was withdrawn from funds in the 10-20 per cent decile, by far the highest figure on record.

Investors’ desire for cheap and cheerful funds, allied to heightened competition between asset managers, has driven a sharp decline in fees globally in recent decades.

The US has led the way with the average asset-weighted expense ratio across mutual funds and ETFs tumbling from 91 basis points in 2002 to 40bp in 2021, before a further drop to 37bp last year.

Last year’s decline, at 7.4 per cent, was the second-largest year-on-year fall since 1994, Morningstar said, estimating that this last cost cut alone saved investors nearly $9.8bn in fees last year.

The fall was a result both of funds cutting fees and investors increasingly switching to cheaper products, with the increasing popularity of ETFs behind much of the decline in average fees.

Noting that investors poured a net $609bn into US-listed ETFs last year, even as a record $1.1tn was withdrawn from US-domiciled mutual funds, according to the Investment Company Institute, a trade body, Armour said “ETF investors expect lower fees, so flows into ETFs generally correlate highly with cheaper fees”.

This switching was elevated last year because of changing market dynamics, he believed, with investors returning to more sensible-type strategies after strategies that chased performance were hit hard in 2022.

A further factor, both in the US and increasingly parts of Europe, has been an evolution in the economics of advice.

A move away from commission-driven remuneration models towards fee-based financial advice has helped fuel the shift towards cheaper funds.

“Advisers are going after cheaper funds so they don’t have too many layers of fees on top of their own,” Armour said. “In some ways that’s just stripping out these fees [from funds] and putting them elsewhere,” he added, although overall he was convinced the process had resulted in a “net win” for investors.

Armour believed the trend towards ever-lower fees would continue, in part driven by active managers extending their most popular mutual fund strategies into the ETF structure, a move that typically comes with decreased fees.

He also pointed to fee cuts this year, such as State Street Global Advisors’ recent decision to cut prices on 10 ETFs, including a halving of the fee for the SPDR Portfolio High Yield Bond ETF (SPHY) to 5bp, just weeks after Schwab Asset Management launched its Schwab High Yield Bond ETF (SCYB) at 10bp.

“There are price wars going on, there are skirmishes that have broken out and I wouldn’t expect it to stop,” Armour said.

However, within the ETF world, at least, fee compression appears to have slowed in 2023, according to data from FactSet. Its figures show average fees fell just 0.1bp in the first half of this year, a fifth of the historic rate.

Elisabeth Kashner, director of global fund analytics at FactSet, said this was in part because of the popularity of some relatively expensive products, such as JPMorgan Equity Premium Income (JEPI), which took in more than $10bn in the first half of 2023.

“JEPI is well named,” Kashner said, with “44 of its direct competitors” undercutting its 35bp fee, “yet JEPI is the largest and fastest growing actively managed ETF”.

“JEPI’s investors are not terribly price sensitive,” she added. “As a result, fee compression has reversed among actively managed size and style ETFs and has slowed for all active equity ETFs.”

More broadly, “as in prior years, investors choosing vanilla and strategic funds continued to gravitate to the cheapest options, but those selecting idiosyncratic approaches and active management paid more and showed less enthusiasm for cheaper options,” Kashner said.

Second, for the first time in six years, more ETFs raised fees in the first half than cut them, FactSet’s data shows, with 200 increasing fees and only 101 cutting them.

The trend has been particularly noticeable in short-term bond “cash management” vehicles, where returns have risen sharply from desultory levels as interest rates have jumped. The First Trust Enhanced Short Maturity ETF (FTSM) has raised its expense ratio from 25bp to 45bp, for example, a move projected to increase revenue by $15mn a year.

NEW YORK (AP) — Shares of Tesla soared Wednesday as investors bet that the electric vehicle maker and its CEO Elon Musk will benefit from Donald Trump’s return to the White House.

Tesla stands to make significant gains under a Trump administration with the threat of diminished subsidies for alternative energy and electric vehicles doing the most harm to smaller competitors. Trump’s plans for extensive tariffs on Chinese imports make it less likely that Chinese EVs will be sold in bulk in the U.S. anytime soon.

“Tesla has the scale and scope that is unmatched,” said Wedbush analyst Dan Ives, in a note to investors. “This dynamic could give Musk and Tesla a clear competitive advantage in a non-EV subsidy environment, coupled by likely higher China tariffs that would continue to push away cheaper Chinese EV players.”

Tesla shares jumped 14.8% Wednesday while shares of rival electric vehicle makers tumbled. Nio, based in Shanghai, fell 5.3%. Shares of electric truck maker Rivian dropped 8.3% and Lucid Group fell 5.3%.

Tesla dominates sales of electric vehicles in the U.S, with 48.9% in market share through the middle of 2024, according to the U.S. Energy Information Administration.

Subsidies for clean energy are part of the Inflation Reduction Act, signed into law by President Joe Biden in 2022. It included tax credits for manufacturing, along with tax credits for consumers of electric vehicles.

Musk was one of Trump’s biggest donors, spending at least $119 million mobilizing Trump’s supporters to back the Republican nominee. He also pledged to give away $1 million a day to voters signing a petition for his political action committee.

In some ways, it has been a rocky year for Tesla, with sales and profit declining through the first half of the year. Profit did rise 17.3% in the third quarter.

The U.S. opened an investigation into the company’s “Full Self-Driving” system after reports of crashes in low-visibility conditions, including one that killed a pedestrian. The investigation covers roughly 2.4 million Teslas from the 2016 through 2024 model years.

And investors sent company shares tumbling last month after Tesla unveiled its long-awaited robotaxi at a Hollywood studio Thursday night, seeing not much progress at Tesla on autonomous vehicles while other companies have been making notable progress.

TORONTO – Canada’s main stock index was up more than 100 points in late-morning trading, helped by strength in base metal and utility stocks, while U.S. stock markets were mixed.

The S&P/TSX composite index was up 103.40 points at 24,542.48.

In New York, the Dow Jones industrial average was up 192.31 points at 42,932.73. The S&P 500 index was up 7.14 points at 5,822.40, while the Nasdaq composite was down 9.03 points at 18,306.56.

The Canadian dollar traded for 72.61 cents US compared with 72.44 cents US on Tuesday.

The November crude oil contract was down 71 cents at US$69.87 per barrel and the November natural gas contract was down eight cents at US$2.42 per mmBTU.

The December gold contract was up US$7.20 at US$2,686.10 an ounce and the December copper contract was up a penny at US$4.35 a pound.

This report by The Canadian Press was first published Oct. 16, 2024.

TORONTO – Canada’s main stock index was up more than 200 points in late-morning trading, while U.S. stock markets were also headed higher.

The S&P/TSX composite index was up 205.86 points at 24,508.12.

In New York, the Dow Jones industrial average was up 336.62 points at 42,790.74. The S&P 500 index was up 34.19 points at 5,814.24, while the Nasdaq composite was up 60.27 points at 18.342.32.

The Canadian dollar traded for 72.61 cents US compared with 72.71 cents US on Thursday.

The November crude oil contract was down 15 cents at US$75.70 per barrel and the November natural gas contract was down two cents at US$2.65 per mmBTU.

The December gold contract was down US$29.60 at US$2,668.90 an ounce and the December copper contract was up four cents at US$4.47 a pound.

This report by The Canadian Press was first published Oct. 11, 2024.