A real estate is a common form of investment compared to all the other assets. Homeownership is also a kind of real estate investment. Every investor in the real estate sector has a different definition for their investments. But there are three things that are common to every investor i.e., risk, growth prospects, and dividends.

While investing, shift your focus to other essential factors such as company valuations and external market forces as well. Without considering all the factors, it can be difficult to gauge the growth potential of the stock.

Rising interest rates and increasing inflation have raised investor concerns. Hence, make your investments safe and pave way for lower risk and healthy returns.

Now, let us look at five real estate stocks to get a clear picture of their recent performances:

[embedded content]

-

FirstService Corporation (TSX: FSV)

FirstService Corp operates two business segments-FirstService Residential and FirstService Brands. FirstService Residential manages low-rise and medium condominiums, co-operatives, and residential communities and is a major contributor to the company’s revenue. FirstService Brands is engaged in providing property services. The customer segments under FirstService Brands are commercial as well as residential.

For the second quarter, ending June 30, 2022, FirstService Corporation’s revenue was reported at US$ 930.7 million compared to US$ 831.6 million in the year-ago quarter. The Q2 2022 adjusted EBITDA too witnessed an increase to US$ 91.3 million from US$ 89.9 million for the same comparative period in 2021.

On the other hand, there was a decrease in the net earnings which were noted at US$ 40,506 million from US$ 44,020 million in the same quarter the previous year.

The quarterly dividend announced by FirstService Corporation was US$ 0.203 per share. It has an EPS (earnings per share) of US$ 3.60.

-

Canadian Apartment Properties Real Estate Investment Trust (TSX: CAR.UN)

Canadian Apartment Properties Real Estate Investment Trust, or CAPREIT, is basically engaged in the leasing and acquisition of multiunit residential rental properties and is a real estate investment trust. The company’s properties include townhouses and apartments. These properties are located across urban areas of Canada.

In the quarter that ended June 30, 2022, the total operating revenue of CAPREIT was posted at C$ 251.69 million as against C$ 228.85 million for the same time of the previous year.

The monthly dividend by the company was reported at C$ 0.121 per share and its five-year dividend growth was noted at 2.48 per cent.

-

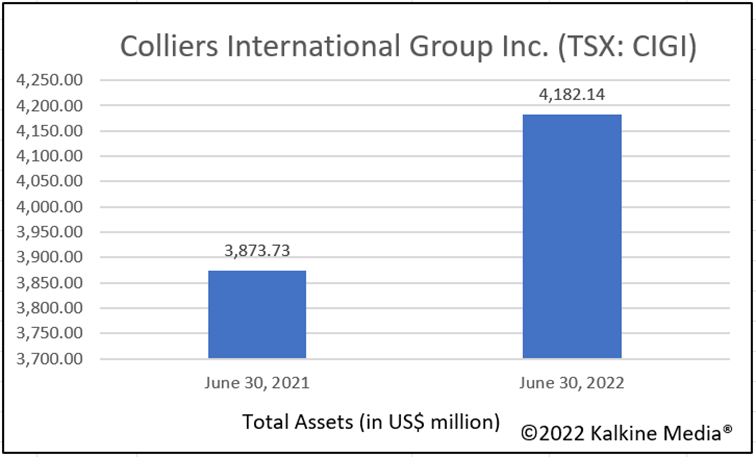

Colliers International Group Inc. (TSX: CIGI)

Colliers International Group Inc. is an investment firm with its presence in over 60 countries. It also provides real estate services to maximize the value of the property for investors, occupiers, and developers.

The revenue of Colliers International Group for the second quarter of fiscal 2022, was reported at US$ 1,127.8 million versus US$ 946 million in the same quarter the previous year.

The adjusted EBTDA witnessed an increase and was noted at US$ 161.3 million compared to US$ 136.6 million. While the Free cash flow decreased to US$ 110.17 million from US$ 157.18 million.

The cash and cash equivalents in Q2 2022, grew to US$ 206.45 million compared to US$ 177.56 million in Q2 2021.

On April 4, 2022, Colliers International announced its acquisition of two firms- Colliers Italy and Antirion SGR S.p.A.

The graph below shows Colliers International’s increase in total assets within a time of 12 months.

-

Granite Real Estate Investment Trust (TSX: GRT.UN)

Granite Real Estate Investment Trust is a real estate investment trust that majorly focuses on managing, acquiring, and developing primarily industrial properties in Europe and North America.

For Q2 2022, revenue of Granite Real Estate increased to C$ 109.8 million from C$ 94 million in Q2 2021. The net operating income also witnessed an increase and was posted at C$ 92.8 million against C$ 80 million for the same comparative period.

As of June 30, 2022, there was a slight increase in the total debt which was reported at C$ 2,540 million as compared to C$ 2,414 million as on December 31, 2022.

Granite pays a monthly dividend of C$ 0.258 to its shareholders. Further, the dividend yield of the company was reported at 4.596 per cent. The EPS of the company is C$ 16.79 with a price-to-earnings (P/E) ratio of four.

-

Allied Properties Real Estate Investment Trust (TSX: AP.UN)

Allied Properties is engaged in managing and developing urban office environments. The company operates in all major cities of Canada. Rental revenue is the major source of income for the company, and it comes from the tenants in its properties.

In Q2 2022, Allied Properties’ total assets grew to C$ 11,620.46 million in comparison to C$ 9,717.64 million for the same comparative period. There was a growth seen in the rental revenue and it was reported at C$ 154.41 million as compared to C$ 138.67 million.

The net income also rose to C$ 100.03 million in comparison to 98.52 million.

Allied Properties pays a monthly dividend of C$ 0.146. Further, the five-year dividend growth was reported at 2.40 per cent.

Bottom Line:

Most investors are attracted to the real estate sector but are not able to handle it due to lack of knowledge. Not all stocks offer the same return during a downturn or market low time.

Look for all the aspects diligently and track all the market forces on regular intervals. Long term investors are aware of the recessionary periods and hence prepare themselves accordingly. Therefore, every investor must implement the long-term approach in their portfolio to safeguard it from the market fluctuations.

Please note, the above content constitutes a very preliminary observation based on the industry and is of limited scope without any in-depth fundamental valuation or technical analysis. Any interest in stocks or sectors should be thoroughly evaluated taking into consideration the associated risks.