The nightmare scenario is one where the virus continues to suffocate the global economy for a year or more.

ISABEL INFANTES/AFP/Getty Images

Over the past three weeks, governments around the world have embarked on one of the greatest peacetime borrowing binges in history.

In many countries – including Canada, the United States, Germany and Britain – policy makers have launched massive stimulus programs to help sustain economies under attack from the novel coronavirus. To fund more than US$5-trillion in relief packages, governments are issuing epic amounts of debt.

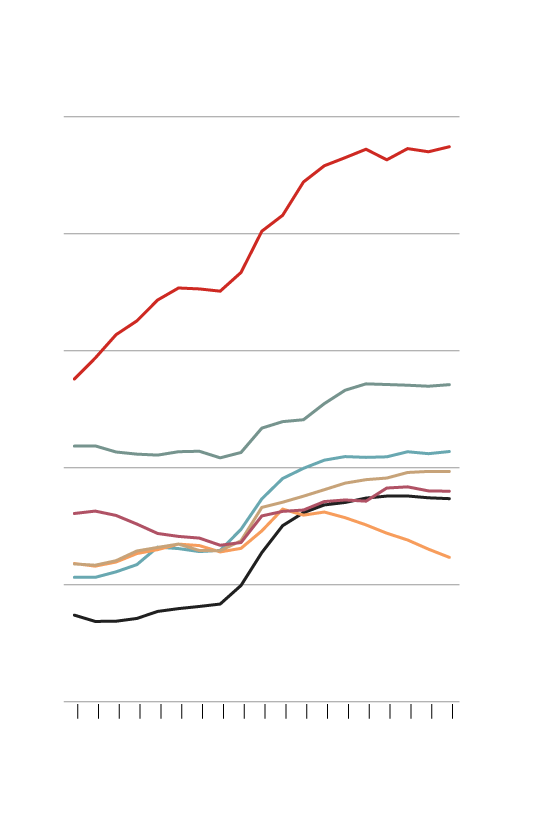

Most big economies will see government borrowing leap higher as a result of the virus, says Gavyn Davies, chairman of Fulcrum Asset Management in London. He expects ratios of public debt to gross domestic product to jump by 10 to 20 percentage points. In Canada, a move of that magnitude would propel general government debt, including both federal and provincial borrowing, to around 100 per cent of GDP, while in the United States it would boost the ratio above 120 per cent.

Story continues below advertisement

Can the world afford this avalanche of new borrowing? For now, the answer is yes. So long as interest rates remain low and economies return to something approaching normality within a few months, developed countries should find the additional burden to be tolerable. Most will remain considerably less indebted than Japan, which for years has sustained stratospheric levels of public borrowing, with government debt well in excess of 200 per cent of GDP.

One big uncertainty hovers over these calculations, however: What happens if the world does not return to normalcy within, say, six months? If so, governments will find themselves writing enormous cheques every month to sustain comatose economies. If that happens, all bets are off.

For now, though, worrying about such possibilities misses the point. Confronted by an overwhelming emergency, governments have little choice but to engage in deficit spending on a giant scale.

In fact, the urgent question isn’t whether these countries can afford to take on more debt. It’s whether they’re taking on enough debt to fund the stimulus programs necessary to avert an even deeper downturn.

Analysts at Bank of America describe the massive US$2-trillion stimulus package passed by U.S. Congress in March as the “bare minimum.” Scott Minerd, chief investment officer at Guggenheim Partners, told Reuters he expects more support will be needed for the U.S. economy. If so, Canada is likely to be caught short as well.

Lockdowns and quarantines needed to fight the virus have already sent unemployment soaring. In Canada, more than two million Canadians filed for unemployment benefits in the last half of March. Meanwhile, in the United States, almost 10 million people have filed for benefits over the past two weeks.

The pain is not going to let up. If private-sector forecasters are right, economic output in the second quarter will shrivel at a 15-per-cent to 35-per-cent annualized rate in Canada and the United States. This would be a far deeper downturn than anything that occurred during the financial crisis.

Story continues below advertisement

General government debt to GDP ratio

In select OECD countries

JOHN SOPINSKI/THE GLOBE AND MAIL, SOURCE: imf

General government debt to GDP ratio

In select OECD countries

JOHN SOPINSKI/THE GLOBE AND MAIL, SOURCE: imf

General government debt to GDP ratio

In select OECD countries

JOHN SOPINSKI/THE GLOBE AND MAIL, SOURCE: imf

Capital Economics is warning clients that the global slowdown is shaping up as the sharpest and deepest global slowdown since the Second World War. Harvard University economist Kenneth Rogoff goes even further: He told Barron’s that the depth of the global downturn could be as bad as anything in the past century and a half.

Without relief, many households will go bust. Their incomes will shrink or vanish, and they will default on mortgages, rent payments and car bills. Meanwhile, many restaurants, retail stores, travel operators, malls, hotels and airlines will tumble into bankruptcy. With all those employers gone, many workers will not have jobs to go back to when the virus does come under control. The slump could stretch on for years and turn into a full-on depression.

Generous government support can help prevent this ugly scenario by ensuring we still have a functioning economy whenever life does return to normal. For most economists, the logic is inarguable: No matter how expensive an outpouring of government aid may seem right now, it is cheaper than dealing with a depression down the road.

Still, the size of the necessary relief programs is staggering. In the United States, for instance, the federal deficit will hit 13 per cent of GDP this year, according to credit rater Fitch. That would blow away the previous record of 9.8 per cent, which occurred during the darkest days of the financial crisis, in 2009.

In Canada, the fiscal programs already unveiled by federal and provincial governments amount to 13 per cent of GDP, Capital Economics calculates. But even that enormous flood of government cash may not be enough to save everyone.

Stephen Brown, senior Canada economist at Capital Economics, points out that 10 per cent of the 13,330 Canadian restaurants that replied to a recent survey indicated they were closing their doors permanently in March. A further 18 per cent said they were likely to go out of business this month. If the imploding restaurant business is any gauge, Canada’s economy may be in need of even more support, and all the government debt that implies.

Story continues below advertisement

Should we worry about the long-term effects of this new borrowing? Without question, the new debt will leave taxpayers with a significantly larger burden to carry in years to come.

But so long as financial conditions remain similar to today’s, the burden should not be overwhelming. “The Canadian government has the space to deliver stimulus on this scale,” DBRS researchers assured investors in a report this week. “The federal government is entering the crisis with a modest fiscal deficit, relatively low levels of debt, and funding costs that are negative in real terms.”

The biggest ally of deficit spenders everywhere is today’s shockingly low interest rates. When Canada and other major industrialized economies can borrow money for 10 years at considerably less than 1 per cent a year, the real burden of carrying additional debt becomes exceedingly small – or even negative, as DBRS notes. At these rates, lenders are essentially begging Canada and other advanced countries to borrow more.

The low rates set up some favourable math. Once the world gets past the worst of the pandemic, and growth returns to more normal levels, the economies in most industrialized countries should expand substantially faster than the interest rate on their debt. This means the size of their government debt should shrink steadily as a portion of GDP. In Canada, for instance, it makes perfect sense to borrow at 0.7 per cent (the current yield on 10-year Canada bonds) to support an economy capable of growing at 3 per cent or more.

Remember, too, that today’s emergency measures are temporary. Unlike proposals for spending on new social programs, the need for most of the new stimulus programs will melt away as soon as the threat from the virus eases.

To be sure, there are risks, particularly in poorer parts of the world. In some emerging economies, a rapid run-up in debt could result in a crisis if investors begin to worry about possible defaults, or if bondholders start to fear that hard-pressed governments will inflate their way out of the problem.

Story continues below advertisement

In more advanced economies, though, one has to squint hard to see any immediate problem. Judging from today’s ultralow yields on Canadian, U.S., German and British government bonds, investors are desperate for safe assets. They are clamouring to buy government bonds from big industrialized economies and that demand is not likely to dry up any time soon.

All this argues strongly that the current borrowing binge should turn out well – so long as things get back to normal in relatively short order.

The nightmare scenario is one where the virus continues to suffocate the global economy for a year or more.

“What would be the effect of the Treasury continuing to add trillions of dollars each quarter to the deficit (which was already running at $1-trillion even before the virus hit) and of the Fed continuing to pump trillions more into the monetary system?” asked Howard Marks, the widely followed co-chairman of Oaktree Capital Management, in a commentary this week.

Mr. Marks puts forward a couple of tentative possibilities: Maybe a burst of inflation because of all that money printing. Maybe a shift away from the U.S. dollar as the world’s reserve currency because of worries over the U.S. economy’s rapidly expanding debt load.

At the very least, he suggests, the next few months will stoke debate around Modern Monetary Theory, the heterodox school of economics that argues government debt and deficits don’t matter. While highly contentious, MMT has helped to focus attention on central banks’ increasingly aggressive interventions in debt markets.

Story continues below advertisement

The largest example of those interventions are the massive bond-buying operations launched by the European Central Bank and the U.S. Federal Reserve since the financial crisis. By hoovering up domestic bonds, these central banks are creating artificial demand for bonds and thereby driving down interest rates (which move in the opposite direction to bond prices).

bond yields

10-year government bond yields,

as of noon Eastern, Friday

JOHN SOPINSKI/THE GLOBE AND MAIL

SOURCE: marketwatch

bond yields

10-year government bond yields, as of noon Eastern, Friday

JOHN SOPINSKI/THE GLOBE AND MAIL, SOURCE: marketwatch

bond yields

10-year government bond yields, as of noon Eastern, Friday

JOHN SOPINSKI/THE GLOBE AND MAIL, SOURCE: marketwatch

To some eyes, bond buying by central banks – or quantitative easing, as it’s known in the jargon – commits the unpardonable sin of blurring the distinction between fiscal and monetary policy. After all, it consists of one arm of government creating money in order to buy debt issued by another arm of government. That looks perilously close to a shell game in which central banks monetize government debt and distort markets.

Defenders of central bankers argue that is not entirely accurate. They say the bank interventions stop short of rigging the game. Rather than holding all the cards, central banks still own only a fraction of government bonds. (In March, for instance, the Fed held about 12 per cent of all U.S. Treasury securities, considerably less than foreign investors and also less than the U.S. Social Security system.) In addition, central banks typically vow the interventions are temporary. They promise to eventually reverse most, if not all, of their bond buying.

Maybe so. But those reversals show no signs of happening in the foreseeable future. Central banks’ balance sheets are expanding furiously as they gobble up government bonds and other forms of debt. The Federal Reserve’s balance sheet has already swelled to US$5.7-trillion from just less than US$4-trillion before the pandemic hit. It could swell to as much as US$10-trillion – roughly half the size of the U.S. economy – over the next few months, according to Capital Economics.

Some commentators believe debt-challenged governments may eventually be forced to go even further and turn to “helicopter money,” a manoeuvre in which central banks would simply create money, without issuing any corresponding debt, and government would funnel the new cash to people and businesses. It is an attractive idea in theory. However, doing so would mark a new level of desperation. It would be a sign that governments are out of alternatives.

Fortunately, we’re not at that point yet. Governments still have the capacity to borrow and will make full use of that power in the weeks and months ahead. But until we win the battle against COVID-19, and revive our battered economies, we are in uncharted territory. Best to not rule anything out.

Story continues below advertisement

Your time is valuable. Have the Top Business Headlines newsletter conveniently delivered to your inbox in the morning or evening. Sign up today.

OTTAWA – Canada’s unemployment rate held steady at 6.5 per cent last month as hiring remained weak across the economy.

Statistics Canada’s labour force survey on Friday said employment rose by a modest 15,000 jobs in October.

Business, building and support services saw the largest gain in employment.

Meanwhile, finance, insurance, real estate, rental and leasing experienced the largest decline.

Many economists see weakness in the job market continuing in the short term, before the Bank of Canada’s interest rate cuts spark a rebound in economic growth next year.

Despite ongoing softness in the labour market, however, strong wage growth has raged on in Canada. Average hourly wages in October grew 4.9 per cent from a year ago, reaching $35.76.

Friday’s report also shed some light on the financial health of households.

According to the agency, 28.8 per cent of Canadians aged 15 or older were living in a household that had difficulty meeting financial needs – like food and housing – in the previous four weeks.

That was down from 33.1 per cent in October 2023 and 35.5 per cent in October 2022, but still above the 20.4 per cent figure recorded in October 2020.

People living in a rented home were more likely to report difficulty meeting financial needs, with nearly four in 10 reporting that was the case.

That compares with just under a quarter of those living in an owned home by a household member.

Immigrants were also more likely to report facing financial strain last month, with about four out of 10 immigrants who landed in the last year doing so.

That compares with about three in 10 more established immigrants and one in four of people born in Canada.

This report by The Canadian Press was first published Nov. 8, 2024.

The Canadian Institute for Health Information says health-care spending in Canada is projected to reach a new high in 2024.

The annual report released Thursday says total health spending is expected to hit $372 billion, or $9,054 per Canadian.

CIHI’s national analysis predicts expenditures will rise by 5.7 per cent in 2024, compared to 4.5 per cent in 2023 and 1.7 per cent in 2022.

This year’s health spending is estimated to represent 12.4 per cent of Canada’s gross domestic product. Excluding two years of the pandemic, it would be the highest ratio in the country’s history.

While it’s not unusual for health expenditures to outpace economic growth, the report says this could be the case for the next several years due to Canada’s growing population and its aging demographic.

Canada’s per capita spending on health care in 2022 was among the highest in the world, but still less than countries such as the United States and Sweden.

The report notes that the Canadian dental and pharmacare plans could push health-care spending even further as more people who previously couldn’t afford these services start using them.

This report by The Canadian Press was first published Nov. 7, 2024.

Canadian Press health coverage receives support through a partnership with the Canadian Medical Association. CP is solely responsible for this content.

As Canadians wake up to news that Donald Trump will return to the White House, the president-elect’s protectionist stance is casting a spotlight on what effect his second term will have on Canada-U.S. economic ties.

Some Canadian business leaders have expressed worry over Trump’s promise to introduce a universal 10 per cent tariff on all American imports.

A Canadian Chamber of Commerce report released last month suggested those tariffs would shrink the Canadian economy, resulting in around $30 billion per year in economic costs.

More than 77 per cent of Canadian exports go to the U.S.

Canada’s manufacturing sector faces the biggest risk should Trump push forward on imposing broad tariffs, said Canadian Manufacturers and Exporters president and CEO Dennis Darby. He said the sector is the “most trade-exposed” within Canada.

“It’s in the U.S.’s best interest, it’s in our best interest, but most importantly for consumers across North America, that we’re able to trade goods, materials, ingredients, as we have under the trade agreements,” Darby said in an interview.

“It’s a more complex or complicated outcome than it would have been with the Democrats, but we’ve had to deal with this before and we’re going to do our best to deal with it again.”

American economists have also warned Trump’s plan could cause inflation and possibly a recession, which could have ripple effects in Canada.

It’s consumers who will ultimately feel the burden of any inflationary effect caused by broad tariffs, said Darby.

“A tariff tends to raise costs, and it ultimately raises prices, so that’s something that we have to be prepared for,” he said.

“It could tilt production mandates. A tariff makes goods more expensive, but on the same token, it also will make inputs for the U.S. more expensive.”

A report last month by TD economist Marc Ercolao said research shows a full-scale implementation of Trump’s tariff plan could lead to a near-five per cent reduction in Canadian export volumes to the U.S. by early-2027, relative to current baseline forecasts.

Retaliation by Canada would also increase costs for domestic producers, and push import volumes lower in the process.

“Slowing import activity mitigates some of the negative net trade impact on total GDP enough to avoid a technical recession, but still produces a period of extended stagnation through 2025 and 2026,” Ercolao said.

Since the Canada-United States-Mexico Agreement came into effect in 2020, trade between Canada and the U.S. has surged by 46 per cent, according to the Toronto Region Board of Trade.

With that deal is up for review in 2026, Canadian Chamber of Commerce president and CEO Candace Laing said the Canadian government “must collaborate effectively with the Trump administration to preserve and strengthen our bilateral economic partnership.”

“With an impressive $3.6 billion in daily trade, Canada and the United States are each other’s closest international partners. The secure and efficient flow of goods and people across our border … remains essential for the economies of both countries,” she said in a statement.

“By resisting tariffs and trade barriers that will only raise prices and hurt consumers in both countries, Canada and the United States can strengthen resilient cross-border supply chains that enhance our shared economic security.”

This report by The Canadian Press was first published Nov. 6, 2024.