Private equity firms, among the world’s largest custodians of institutional money, have been buying up companies that advise individuals on their wealth.

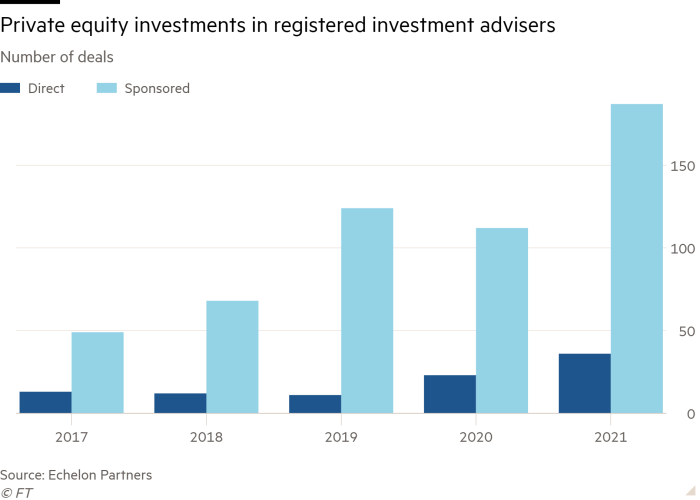

The number of private equity deals for registered investment advisers has surged to a record 223 so far in 2021, according to data from investment bank Echelon Partners. The sum is up almost two-thirds from 2020 and more than three times the number of deals five years ago.

The latest came this month, when Apollo agreed to buy the US wealth distribution and asset management arm of Los Angeles-based Griffin Capital, which has more than $5bn in actively managed closed-end funds, including a credit and real estate fund and dozens of staff who distribute investment strategies.

Other private equity firms such as KKR, Hellman & Friedman and TA Associates have been acquiring investment adviser groups.

Wealth management typically has a high degree of recurring revenue, with customer “stickiness” that’s similar to a software company, said Daniel Seivert, chief executive of Echelon Partners.

And in September, the Securities and Exchange Commission’s asset management committee recommended allowing retail investors to invest in private fund strategies, Seivert said — potentially enabling wealth management clients to invest with the firms that back their advisers.

In the Griffin deal, Apollo will not only pick up an asset management company that it can scale, but Griffin also distributes funds to registered investment advisers and brokers, who are a potentially huge new source of private equity assets.

Apollo wants to raise at least $50bn in capital from individual investors within the next five years, the firm said in a presentation in October. This segment accounted for 5 per cent of the capital that Apollo raised on average between 2018 to 2020, and the firm hopes to grow that to at least 30 per cent, Stephanie Drescher, Apollo’s chief client and product development officer, said during the presentation.

“Scaling global wealth is our key bet,” she said. “It’s a market that is two times the size of the institutional market, yet they’re under-allocated by two-to-five times to alternatives.”

Private equity firms are targeting the wealth management industry in part because technology has made it easier for individual investors to access “alternatives,” or more specialised investments than ordinary stock and bond markets.

“Private equity sponsors continue to recognise that solutions exist to help capture what has evolved from a more fractured and less transparent marketplace to one that can deliver more value across broader investor segments,” said Georges Archibald, head of the Americas for financial services provider Apex Group.

Other wealth management deals by private equity this year have included TA Associates’ investment in the advisory group Caprock and KKR buying half of $20bn Beacon Pointe Advisors from Abry Partners last month.

KKR wants to support growth plans for Beacon Pointe, a female-led registered investment adviser, and sees its Women’s Advisory Institute as important to serving women, Chris Harrington, a KKR partner, said. The investment in Beacon Pointe follows KKR’s exit this year from wealth management firm Focus Financial, which it took public in 2018.

Some US-based private equity firms are looking to less competitive markets overseas. This summer, Lightyear Capital funds bought UK-based Wren Sterling Financial Planning, and Flexpoint Ford acquired UK-based AFH Financial Group.

Aside from direct investments, most wealth deals were executed by portfolio companies owned by private equity, such as Leonard Green-backed serial acquirer Mariner Wealth and Oak Hill-backed Mercer Advisors. Mariner Wealth announced its ninth acquisition of the year last month, while Mercer Advisors scooped up 15 RIAs this year.

“Nearly all the most active strategic acquirers in today’s market are backed by prominent private equity firms and are often backed by more than one sponsor,” Seivert said.