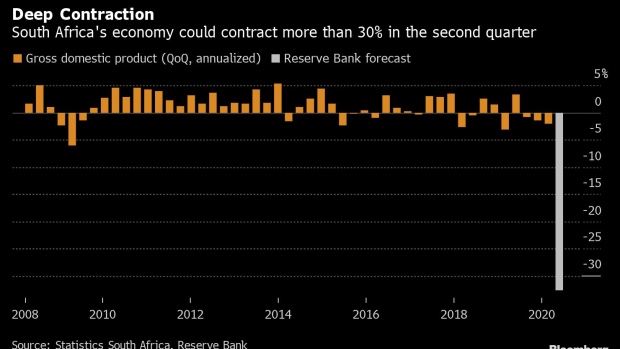

South Africa’s economy probably contracted more than 30% in the second quarter when restrictions to curb the spread of the coronavirus shuttered almost all activity for five weeks, according to central bank forecasts.

The annualized drop in gross domestic product is forecast at 32.6% for the three months through June from the previous quarter, the Pretoria-based Reserve Bank said in an emailed response to a query. That would be the deepest quarterly decline since at least 1990. The central bank’s projection in its annual report that was released on June 29 shows the economy will expand on a quarterly basis in the three months through September, which means the technical recession will be over.

The economy contracted an annualized 2% in the three months through March, the first time since 2009 that a South African recession has lasted longer than two quarters. The slump was less than projected and economists including Kevin Lings of Stanlib Asset Management warned that the fall-off in the second quarter will be severe.

South Africa implemented a strict lockdown from March 27 to limit the spread of the pandemic. For five weeks, almost all activity except essential services was halted and most citizens were only allowed to leave their homes to buy food, seek medical care and collect welfare grants.

The restrictions were eased from May 1, allowing the phased reopening of some businesses and industries. Still, many companies have closed down permanently and some of those that have resumed operations are still limited as to which services they may offer.

The Reserve Bank sees the economy contracting by 7% this year and the National Treasury projects a 7.2% decline in output. That would be the most since the Great Depression, when GDP fell by 6.2% in 1931. The near-term economic outlook is highly dependent on the development of the coronavirus pandemic and the extent of restrictions on business activity to limit the spread, the central bank said in an annual report.

OTTAWA – Statistics Canada says the country’s merchandise trade deficit narrowed to $1.3 billion in September as imports fell more than exports.

The result compared with a revised deficit of $1.5 billion for August. The initial estimate for August released last month had shown a deficit of $1.1 billion.

Statistics Canada says the results for September came as total exports edged down 0.1 per cent to $63.9 billion.

Exports of metal and non-metallic mineral products fell 5.4 per cent as exports of unwrought gold, silver, and platinum group metals, and their alloys, decreased 15.4 per cent. Exports of energy products dropped 2.6 per cent as lower prices weighed on crude oil exports.

Meanwhile, imports for September fell 0.4 per cent to $65.1 billion as imports of metal and non-metallic mineral products dropped 12.7 per cent.

In volume terms, total exports rose 1.4 per cent in September while total imports were essentially unchanged in September.

This report by The Canadian Press was first published Nov. 5, 2024.