The European Union’s lost opportunity to shake off the coronavirus with swift vaccinations is likely to overshadow economic forecasts this week that may show a frustratingly slow recovery in 2021.

The European Commission has the uncomfortable task of revealing an outlook that will implicitly highlight the impact of the bloc’s delayed procurement of inoculations. Persisting lockdowns are probably costing the EU economy about 12 billion euros ($14 billion) per week in missing output, according to Bloomberg Economics.

It’s not clear if the executive will need to downgrade its prior euro-zone forecast for an incomplete rebound of 4.2% from 2020’s massive contraction. In any case, those predictions on Thursday will surely struggle to convey as much optimism as the Bank of England did last week when it confirmed the U.K.’s go-it-alone vaccine strategy is paying off materially on growth.

Herd Immunity Trajectory

Years required to inoculate 75% of the population with a two-dose vaccine

Source: Bloomberg’s Covid-19 Vaccine Tracker

Note: Herd immunity forecast at 70%-85% vaccination level

.chart-js display: none;

Aside from the political furor in Brussels over the EU’s faltering immunization push, the fallout may put the onus on officials in Frankfurt to determine if the euro region’s recovery is getting enough support. That might be a question for European Central Bank President Christine Lagarde to answer when she testifies to the bloc’s parliament on Monday.

What Bloomberg Economics Says:

“The spread of more transmissible strains of Covid-19 and a slow start to the vaccination campaigns means that it will take longer before containment measures can be lifted. While economies have adapted to this new environment, restrictions will continue to weigh on the outlook well into the first half of the year.”

–Maeva Cousin, euro-area economist

Elsewhere, Lagarde’s predecessor, Mario Draghi, may be sworn in as Italy’s next prime minister at the head of a technocrat government, and central banks in Russia, Sweden and Mexico set interest rates.

Central Bank Rate Decisions This Week

.chart-js display: none;

Click here for what happened last week and below is our wrap of what is coming up in the global economy.

U.S.

Investors in the U.S. will be watching out for the latest consumer-price data, to see if higher costs for some industries are finding their way to households. Federal Reserve Chair Jerome Powell is also scheduled to speak Wednesday at the Economic Club of New York on the labor market.

Congressional committees are set to start crafting legislation this week on specific components of President Joe Biden’s $1.9 trillion Covid-19 relief plan after votes in the House and Senate Friday on a budget resolution for 2021.

Europe, Middle East, Africa

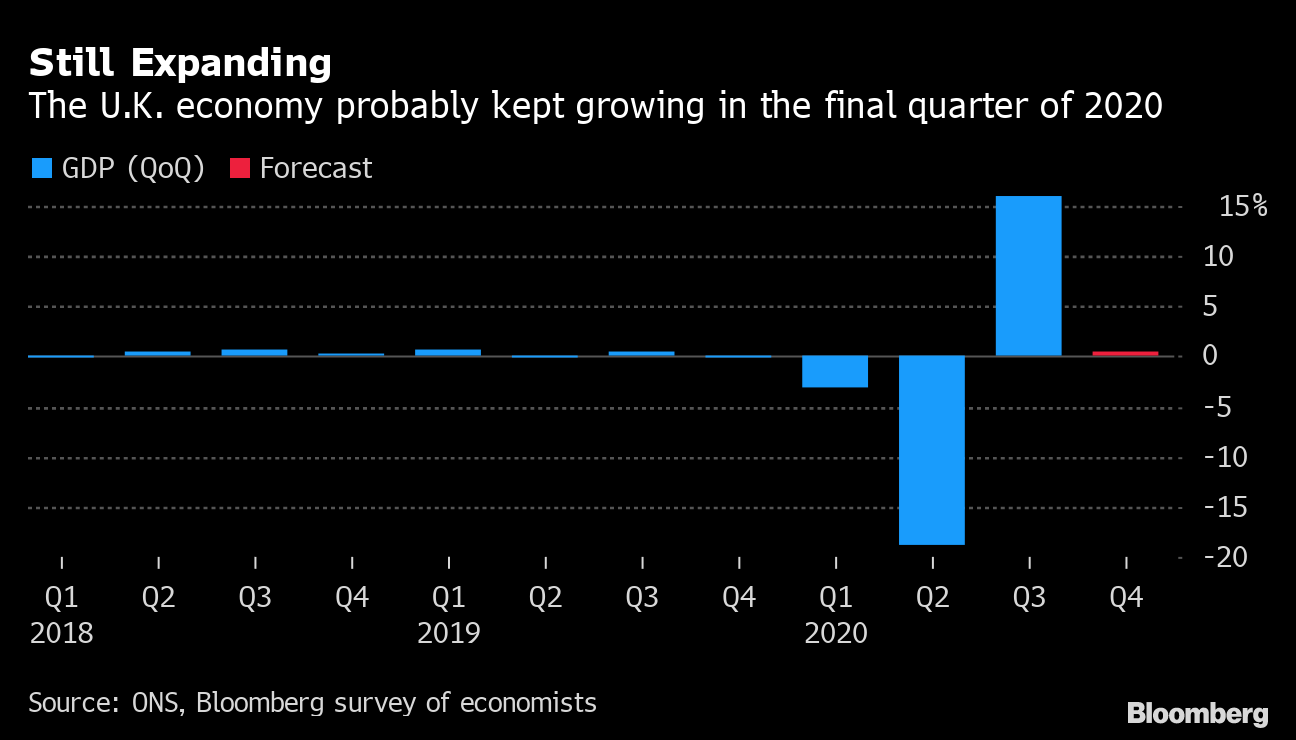

The U.K. economy probably kept growing in the fourth quarter, albeit at a weaker pace than the 16% rebound sustained in the prior three months. Economists anticipate a 0.5% expansion in gross domestic product for the period, a last spurt before new lockdowns brought activity to another crashing halt in recent weeks. Those data are due Friday.

Still Expanding

The U.K. economy probably kept growing in the final quarter of 2020

Source: ONS, Bloomberg survey of economists

.chart-js display: none;

As the BOE steers markets away from the idea that it might soon adopt negative rates in the U.K., a pioneering central bank that has already abandoned the policy is likely to keep borrowing costs at zero. Investors will likely focus on the Riksbank’s asset purchase program as vaccinations are seen gathering pace to help Sweden’s economy rebound.

Most economists expect Russian central bank Governor Elvira Nabiullina to keep rates on hold at her first policy meeting of the year on Friday, but rising inflation and ruble weakness might still prompt her to start hinting at an increase.

Serbia’s central bank also holds a rate meeting and is expected to keep the benchmark at a record low. In Romania, the parliament may debate and vote on a much-delayed 2021 state budget in the first major test for the country’s ruling coalition.

Ghana’s statistics office will release data on Wednesday that will probably show inflation remained close to the 10% top of the central bank’s target range. In South Africa, a report the same day will likely show business confidence remained muted in December and January after some Covid-19 restrictions were reimposed and power cuts resumed.

Asia

Data out Monday could show a shift in Japan’s remarkably low bankruptcy levels, as its renewed state of emergency puts more pressure on smaller businesses. Wage figures are expected to show a sharp fall on lower bonuses that could further weaken consumption.

New Bank of Japan board member Toyoaki Nakamura makes a debut speech Wednesday that will be closely scrutinized for clues over the BOJ’s policy review.

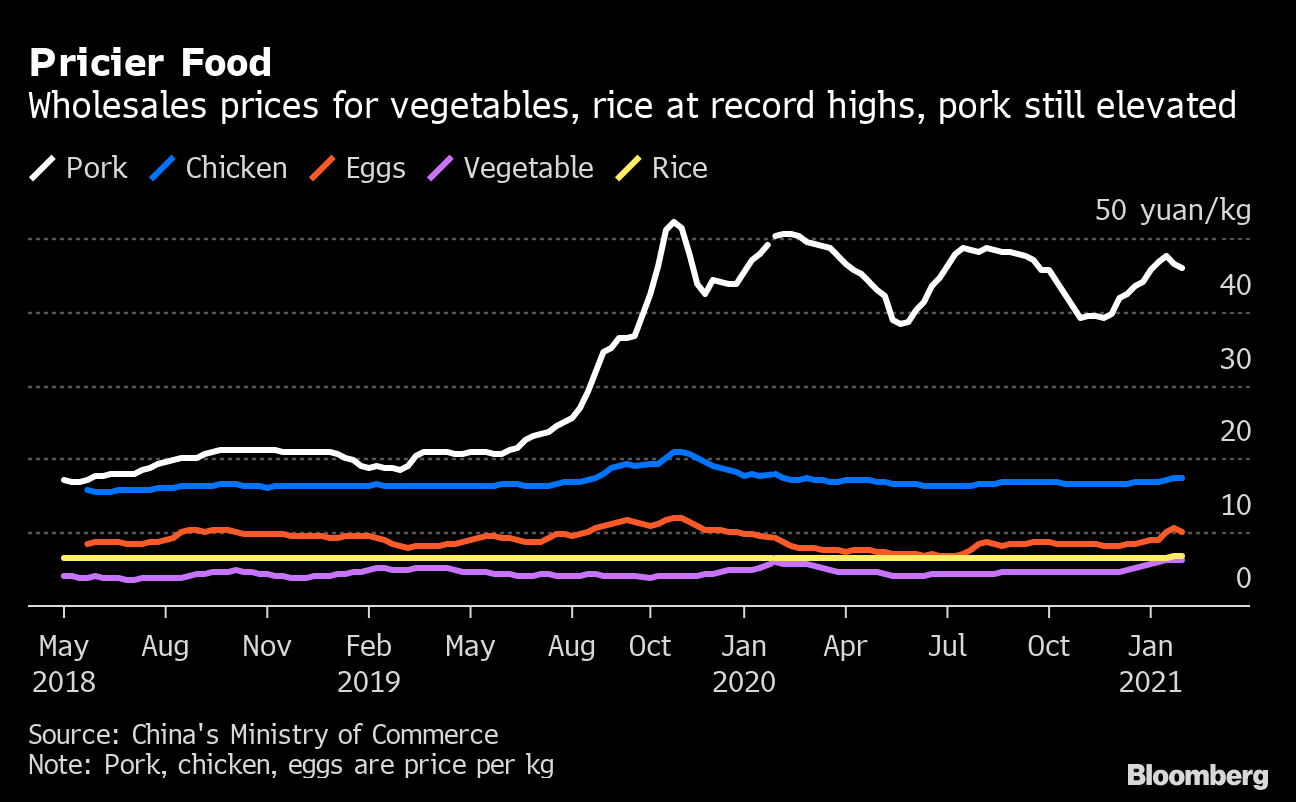

In China, inflation data due Wednesday are expected to show overall consumer prices fell slightly in January, although it may not feel that way for many people struggling with soaring food prices ahead of the Lunar New Year holiday that starts the next day.

Pricier Food

Wholesales prices for vegetables, rice at record highs, pork still elevated

Source: China’s Ministry of Commerce

Note: Pork, chicken, eggs are price per kg

.chart-js display: none;

On Thursday, Malaysia will report fourth quarter and full-year GDP numbers while interest rates are likely to be left on hold in the Philippines.

India’s CPI data for January, due on Friday, may reveal inflation remained in the central bank’s comfort zone for a second month.

Latin America

After a quiet 2020, inflation is back on Latin America’s agenda. Of the four countries reporting January data this week, the results from Chile and Argentina won’t surprise or influence policy, but those from Brazil and Mexico just might.

Heating Up

Brazilian inflation, key rate seen rising

Source: Estimates of analysts surveyed by Bloomberg.

.chart-js display: none;

Banco Central do Brasil would dearly like to hold at 2% next month, but accelerating price gains may force its hand, while analysts see some chance Banxico will look past slightly faster readings and cut its key rate to 4% Thursday.

The easing of lockdowns should flatter Colombia’s December retail sales result while a resurgence of the virus and wind-down of cash handouts should further deflate retailing and economic activity figures for Brazil.

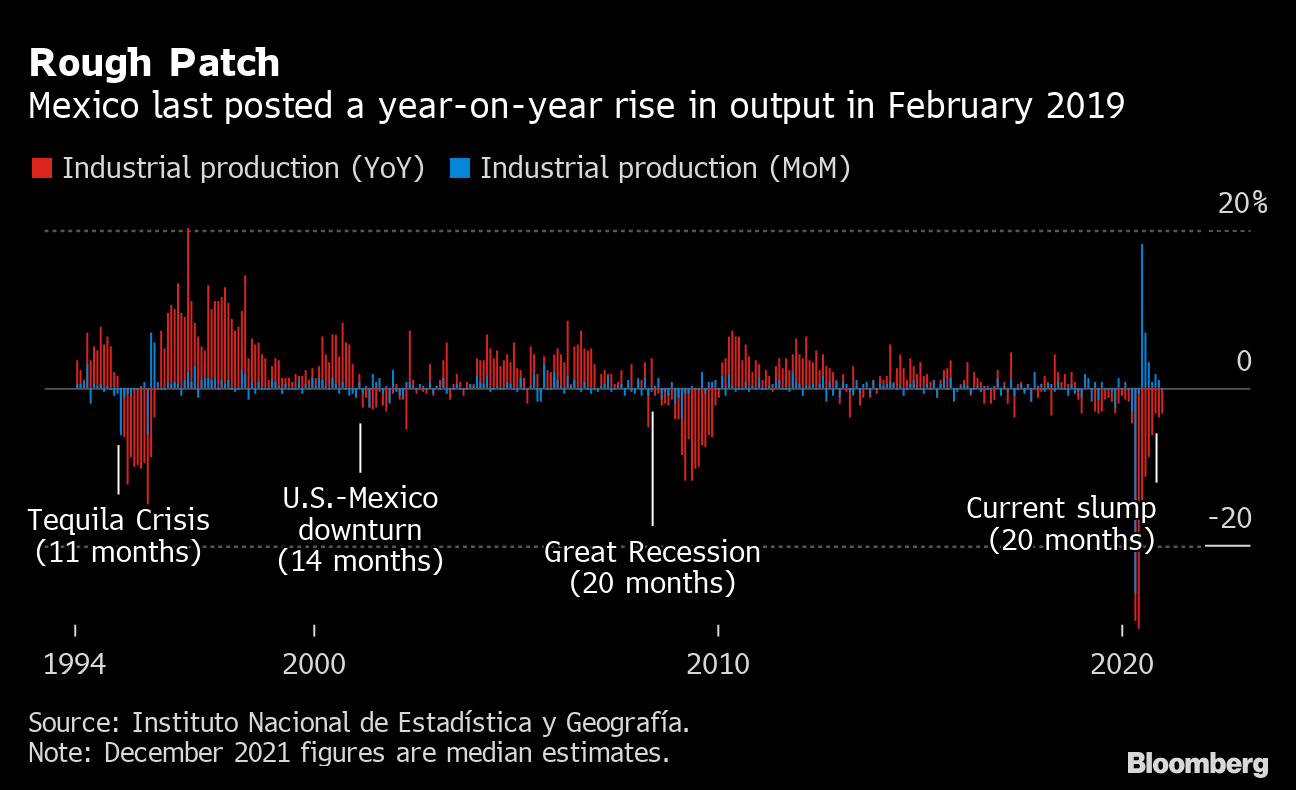

Rough Patch

Mexico last posted a year-on-year rise in output in February 2019

Source: Instituto Nacional de Estadística y Geografía.

Note: December 2021 figures are median estimates.

.chart-js display: none;

Unsurprisingly, the pandemic knocked Mexico’s industrial sector flat. In the longer view, however, December will likely see a 21st consecutive negative year-on-year print, with February 2019 as lone positive reading under President Andres Manuel Lopez Obrador.

Peru’s central bank on Thursday will all but certainly hold at 0.25% for a 10th month.

— With assistance by Peggy Collins, Robert Jameson, Benjamin Harvey, Alessandra Migliaccio, Malcolm Scott, and Alaa Shahine