Note: A version of this article was published on Tker.co.

Stocks rallied last week, with the S&P 500 rising 2.5% to close at 4,719.19. The index is now up 22.9% year to date, up 31.9% from its October 12, 2022 closing low of 3,577.03, and down 1.6% from its January 3, 2022 record closing high of 4,796.56.

Inflation continues to dominate conversations about the markets and the economy.

But the nature of those conversations have shifted significantly over the past year. This evolution can be seen in how the Federal Reserve’s language has changed from meeting to meeting.

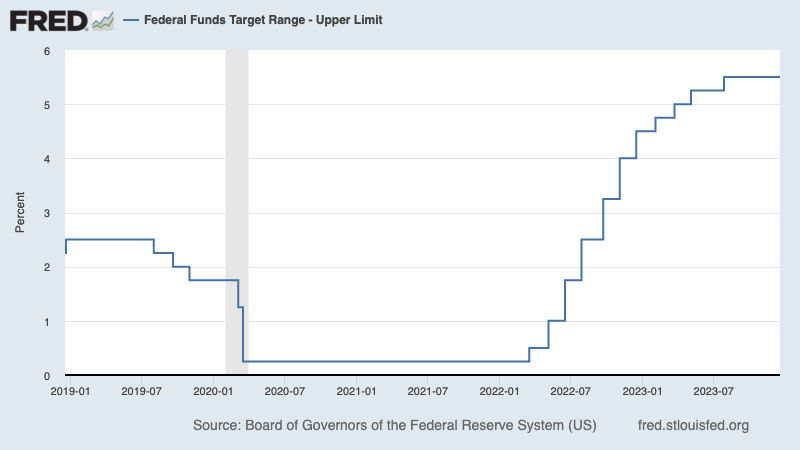

At the Fed’s December 2022 policy meeting, Chair Jerome Powell warned: “Inflation remains well above our longer-run goal of 2%. … It will take substantially more evidence to give confidence that inflation is on a sustained downward path.”

At the time, inflation rates had begun to come down from their mid-2022 highs — but confidence wasn’t particularly high that they would come down to comfortable levels in the near term. Everyone agreed interest rates would be hiked further in 2023. And many economists were convinced that the cost of defeating inflation was a recession.

Fast forward to present day after four more interest rate hikes. At their December 2023 meeting this past week, Powell acknowledged, “We’re seeing inflation making real progress.”

Impressively, the economy absorbed higher interest rates and realized lower inflation without having to go into recession. To get a sense of how surprising this was, check out: TKer’s 2023 chart of the year

As more and more people were able to go back to work, supply chains eased and supply gradually caught up with demand. This helped ease inflation, even as economic growth persisted — suggesting the goldilocks soft landing scenario that TKer described in January.

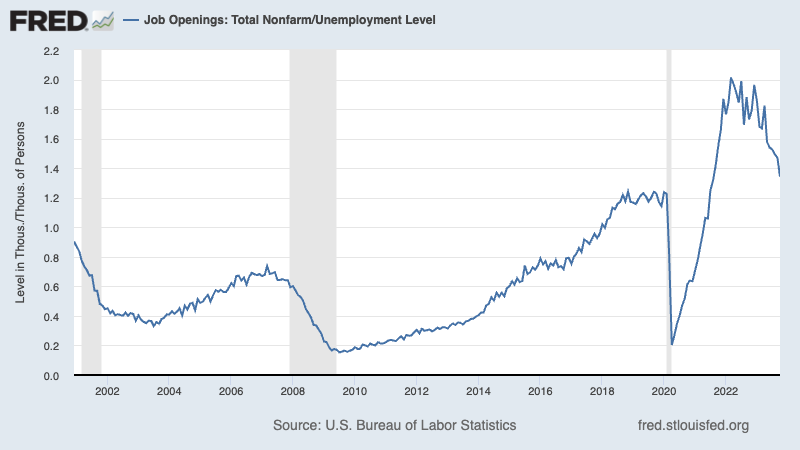

More recently, the massive tailwinds that have defined excess demand have faded significantly. Specifically, excess savings are nearing depletion, job openings are coming into balance with unemployment, and business investment orders have leveled off.

And while economic normalization has been good news for inflation, it also means demand is not as hot as it used to be.

The pandemic era economy has been an unusual one. The initial disruptions were unprecedented. With the unusually strong positive developments over time came unusually problematic challenges like inflation rates surging to levels the world hasn’t seen in 40 years.

And the pace and nature of the economic recovery has been almost unimaginable.

“I have always felt,” Fed Chair Jerome Powell said on December 13, “since the beginning, that there was a possibility, because of the unusual situation, that the economy could cool off in a way that enabled inflation to come down without the kind of large job losses that have often been associated with high inflation and tightening cycles. So far, that’s what we’re seeing.”

As things normalize, we can expect areas of strength to fade, which could present new challenges. But we should also expect new positives to emerge as unusual headwinds like high inflation dissipate.

There were a few notable data points and macroeconomic developments from last week to consider:

TheFed keeps rates unchanged, signals rate cuts. On Wednesday, the Federal Reserve kept monetary policy tight, leaving its target for the federal funds rate unchanged at a range of 5.25% to 5.5%.

From the Fed’s policy statement: “Recent indicators suggest that growth of economic activity has slowed from its strong pace in the third quarter. Job gains have moderated since earlier in the year but remain strong, and the unemployment rate has remained low. Inflation has eased over the past year but remains elevated.”

However, the Fed’s economic projections suggested that the central bank could cut rates three times in 2024.

That said, inflation still has to cool more and stay cool for a little while before the central bank is comfortable with price stability. So even though there may not be more rate hikes and rate cuts may be around the corner, rates are likely to be kept high for a while.

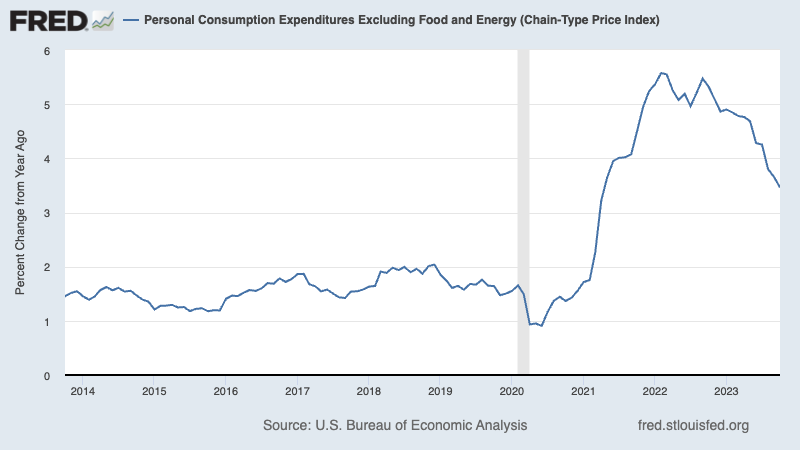

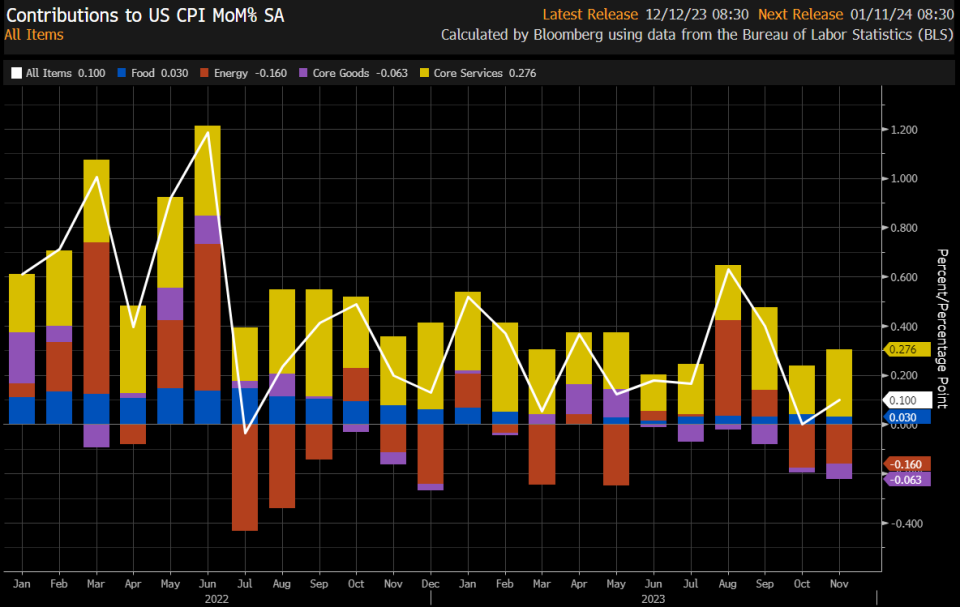

Inflation cools. According to BLS data released Tuesday, the Consumer Price Index (CPI) in November was up 3.1% from a year ago. This was down from the 3.2% rate in October. Adjusted for food and energy prices, core CPI was up 4.0%, the lowest since September 2021.

On a month-over-month basis, CPI was up just 0.1% as energy prices fell 2.3%. Core CPI was up a modest 0.3% as good prices fell and services prices rose.

If you annualize the three-month trend in the monthly figures, CPI was rising at a 2.2% rate and core CPI was climbing at a 3.4% rate.

While many broad measures of inflation continue to hover above the Fed’s target rate of 2%, they are way down from peak levels in the summer of 2022. And the trend suggests they could continue to move lower.

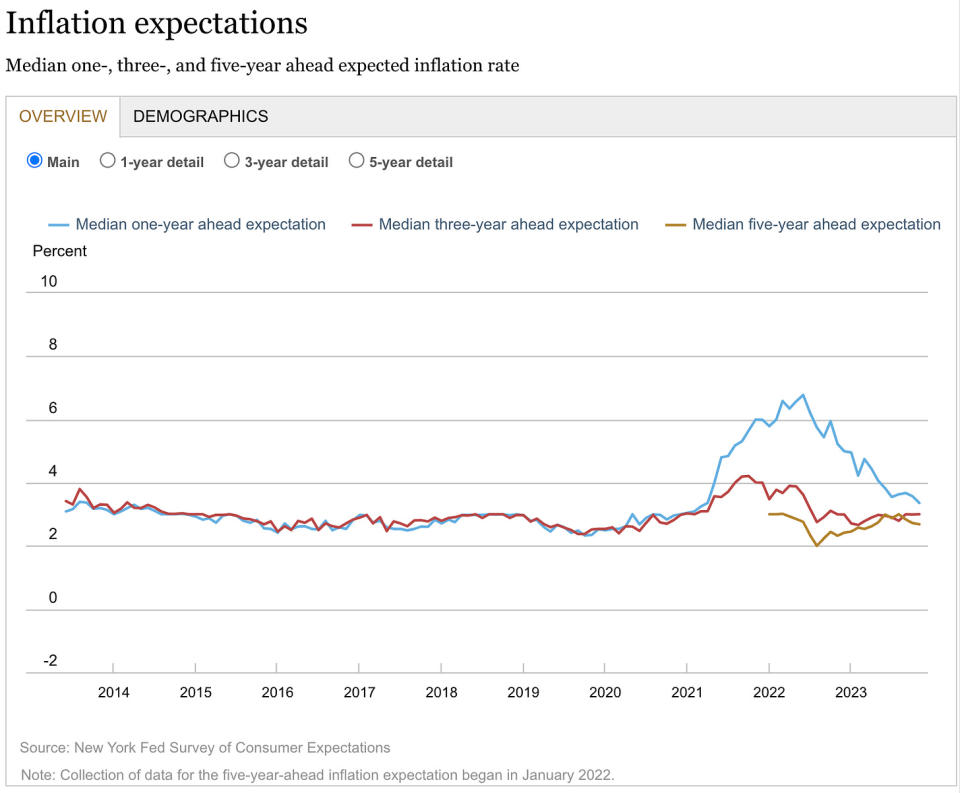

Inflation expectations improve. From the New York Fed’s November Survey of Consumer Expectations: “Median one-year ahead inflation expectations declined by 0.2 percentage point in November to 3.4%. This is the lowest reading since April 2021. Median inflation expectations at the three- and five-year ahead horizons remained unchanged at 3.0% and 2.7%, respectively.”

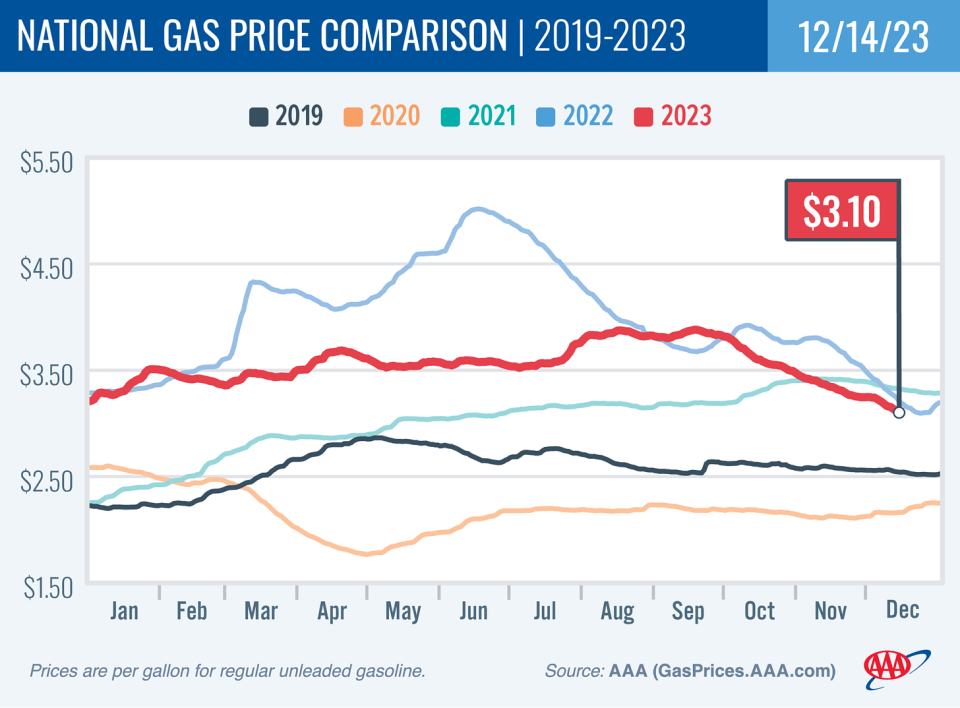

Gas prices continue to fall. From AAA: “According to new data from the Energy Information Administration (EIA), gas demand increased from 8.47 to 8.86 million b/d last week. Meanwhile, total domestic gasoline stocks increased slightly to 224 million bbl. Typically, higher demand would push pump prices higher, but lower oil prices have pushed prices lower. If oil prices remain low, drivers can expect pump prices to do the same during the holiday season. Today’s national average of $3.10 is 25 cents less than a month ago and 11 cents less than a year ago.”

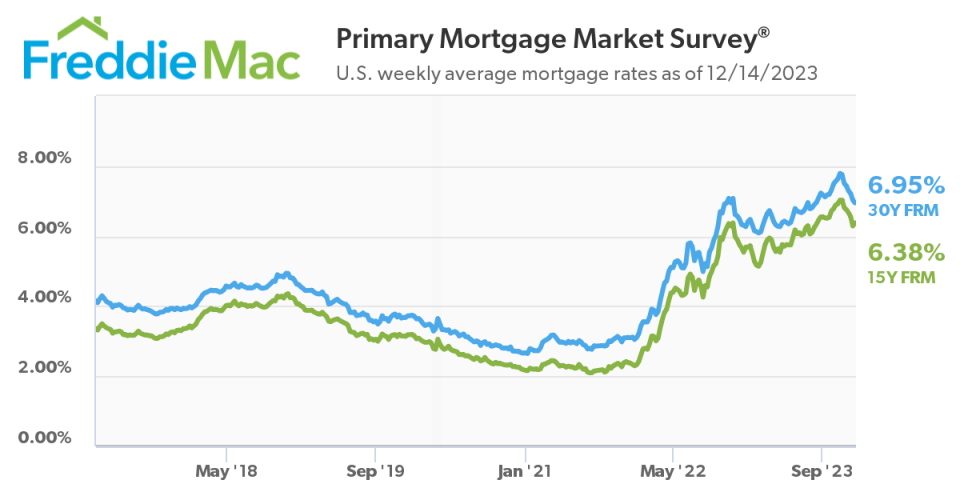

Mortgage rates continue to decline. According to Freddie Mac, the average 30-year fixed-rate mortgage fell to 6.95%. From Freddie Mac: “Potential homebuyers received welcome news this week as mortgage rates dropped below seven percent for the first time since August. Given inflation continues to decelerate and the Federal Reserve Board’s current expectations that they will lower the federal funds target rate next year, there will likely be a gradual thawing of the housing market in the new year.”

Rent is coming down. From Redfin: “The median U.S. asking rent declined 2.1% year over year in November to $1,967 — the biggest annual drop since February 2020 — and fell 0.6% from October.”

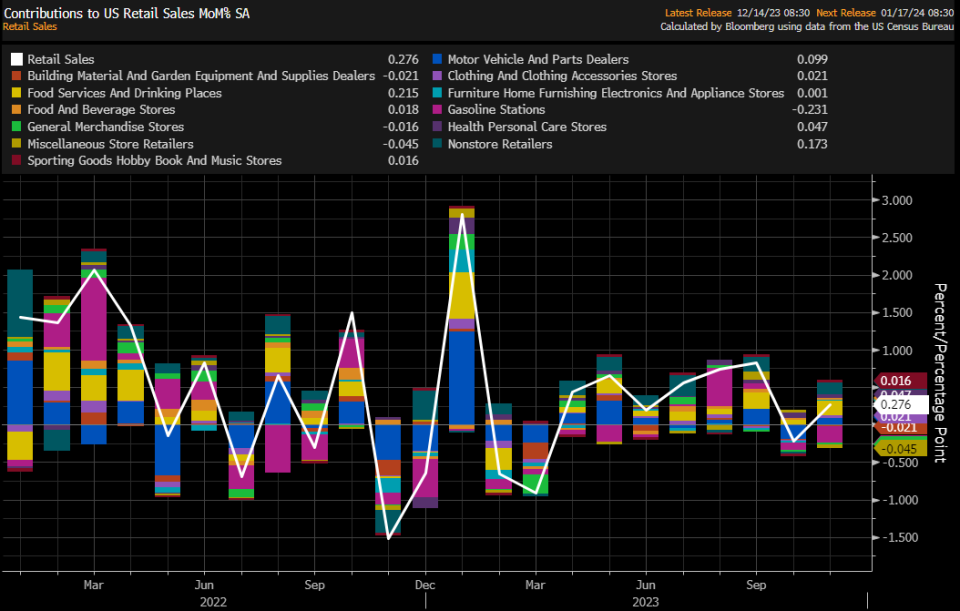

Consumers are spending. Retail sales increased 0.3% in November to a record $705.7 billion.

Categories leading growth included restaurants and bars, sporting and hobby, online, and furniture. Gas stations, department stores, and electronics saw declines.

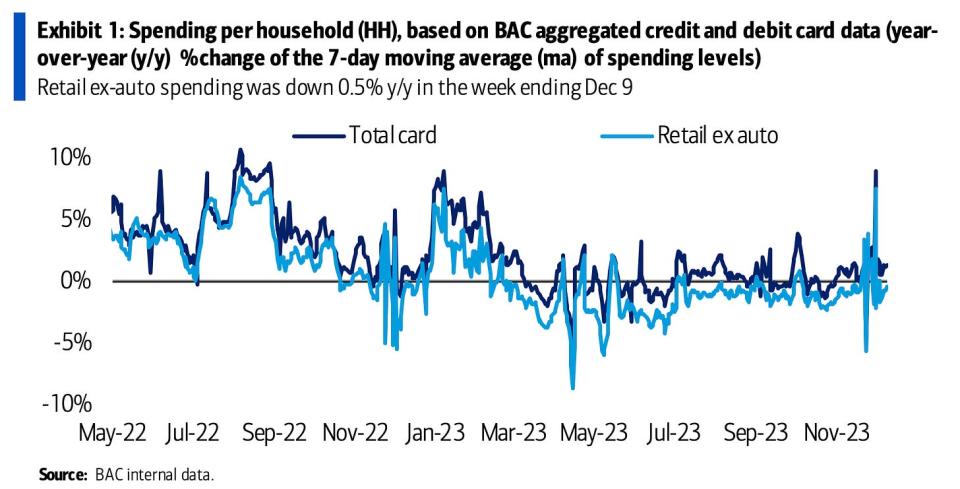

Card data suggest consumer spending is holding up in December. From BofA: “Total card spending per HH was up 1.3% y/y in the week ending Dec 9, according to BAC aggregated credit and debit card data. Spending on holiday items fell 1.5% y/y in the week ending Dec 9. … However, in the 16 days since Thanksgiving, spending on holiday items was up 0.8% compared to the same period last year.”

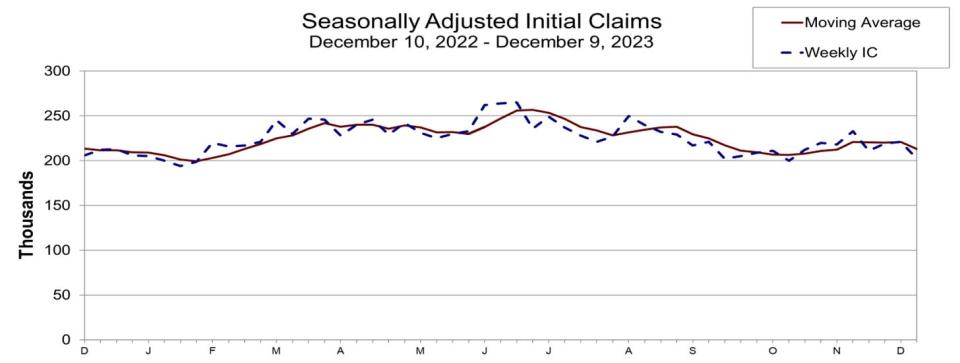

Unemployment claims fall. Initial claims for unemployment benefits fell to 202,000 during the week ending December 9, down from 220,000 the week prior. While this is up from a September 2022 low of 182,000, it continues to trend at levels associated with economic growth.

This comes as the Federal Reserve continues to employ very tight monetary policy in its ongoing effort to bring inflation down. While it’s true that the Fed has taken a less hawkish tone in 2023 than in 2022, and that most economists agree that the final interest rate hike of the cycle has either already happened or is near, inflation still has to cool more and stay cool for a little while before the central bank is comfortable with price stability.

OTTAWA – Statistics Canada says wholesale sales, excluding petroleum, petroleum products, and other hydrocarbons and excluding oilseed and grain, rose 0.4 per cent to $82.7 billion in July.

The increase came as sales in the miscellaneous subsector gained three per cent to reach $10.5 billion in July, helped by strength in the agriculture supplies industry group, which rose 9.2 per cent.

The food, beverage and tobacco subsector added 1.7 per cent to total $15 billion in July.

The personal and household goods subsector fell 2.5 per cent to $12.1 billion.

In volume terms, overall wholesale sales rose 0.5 per cent in July.

Statistics Canada started including oilseed and grain as well as the petroleum and petroleum products subsector as part of wholesale trade last year, but is excluding the data from monthly analysis until there is enough historical data.

This report by The Canadian Press was first published Sept. 13, 2024.

VICTORIA – British Columbia is forecasting a record budget deficit and a rising debt of almost $129 billion less than two weeks before the start of a provincial election campaign where economic stability and future progress are expected to be major issues.

Finance Minister Katrine Conroy, who has announced her retirement and will not seek re-election in the Oct. 19 vote, said Tuesday her final budget update as minister predicts a deficit of $8.9 billion, up $1.1 billion from a forecast she made earlier this year.

Conroy said she acknowledges “challenges” facing B.C., including three consecutive deficit budgets, but expected improved economic growth where the province will start to “turn a corner.”

The $8.9 billion deficit forecast for 2024-2025 is followed by annual deficit projections of $6.7 billion and $6.1 billion in 2026-2027, Conroy said at a news conference outlining the government’s first quarterly financial update.

Conroy said lower corporate income tax and natural resource revenues and the increased cost of fighting wildfires have had some of the largest impacts on the budget.

“I want to acknowledge the economic uncertainties,” she said. “While global inflation is showing signs of easing and we’ve seen cuts to the Bank of Canada interest rates, we know that the challenges are not over.”

Conroy said wildfire response costs are expected to total $886 million this year, more than $650 million higher than originally forecast.

Corporate income tax revenue is forecast to be $638 million lower as a result of federal government updates and natural resource revenues are down $299 million due to lower prices for natural gas, lumber and electricity, she said.

Debt-servicing costs are also forecast to be $344 million higher due to the larger debt balance, the current interest rate and accelerated borrowing to ensure services and capital projects are maintained through the province’s election period, said Conroy.

B.C.’s economic growth is expected to strengthen over the next three years, but the timing of a return to a balanced budget will fall to another minister, said Conroy, who was addressing what likely would be her last news conference as Minister of Finance.

The election is expected to be called on Sept. 21, with the vote set for Oct. 19.

“While we are a strong province, people are facing challenges,” she said. “We have never shied away from taking those challenges head on, because we want to keep British Columbians secure and help them build good lives now and for the long term. With the investments we’re making and the actions we’re taking to support people and build a stronger economy, we’ve started to turn a corner.”

Premier David Eby said before the fiscal forecast was released Tuesday that the New Democrat government remains committed to providing services and supports for people in British Columbia and cuts are not on his agenda.

Eby said people have been hurt by high interest costs and the province is facing budget pressures connected to low resource prices, high wildfire costs and struggling global economies.

The premier said that now is not the time to reduce supports and services for people.

Last month’s year-end report for the 2023-2024 budget saw the province post a budget deficit of $5.035 billion, down from the previous forecast of $5.9 billion.

Eby said he expects government financial priorities to become a major issue during the upcoming election, with the NDP pledging to continue to fund services and the B.C. Conservatives looking to make cuts.

This report by The Canadian Press was first published Sept. 10, 2024.

Note to readers: This is a corrected story. A previous version said the debt would be going up to more than $129 billion. In fact, it will be almost $129 billion.

NANAIMO, B.C. – Former Bank of Canada governor Mark Carney says he’ll be advising the Liberal party to flip some the challenges posed by an increasingly divided and dangerous world into an economic opportunity for Canada.

But he won’t say what his specific advice will be on economic issues that are politically divisive in Canada, like the carbon tax.

He presented his vision for the Liberals’ economic policy at the party’s caucus retreat in Nanaimo, B.C. today, after he agreed to help the party prepare for the next election as chair of a Liberal task force on economic growth.

Carney has been touted as a possible leadership contender to replace Justin Trudeau, who has said he has tried to coax Carney into politics for years.

Carney says if the prime minister asks him to do something he will do it to the best of his ability, but won’t elaborate on whether the new adviser role could lead to him adding his name to a ballot in the next election.

Finance Minister Chrystia Freeland says she has been taking advice from Carney for years, and that his new position won’t infringe on her role.

This report by The Canadian Press was first published Sept. 10, 2024.