A key goal laid out in the federal government’s recent speech from the throne was to “build back better to create a stronger, more resilient Canada.” In our view, “building back better” must include placing growing clean industries (such as electric vehicle manufacturing and zero-carbon power generation) at the centre of Canada’s industrial policy. At the same time, our social contract must be rejuvenated to take care of our young and old with affordable and accessible childcare and long-term care. The sketch provided by the throne speech suggests the government is on the right track – but it did not explain how we will be able to afford the significant investments needed to make the vision into a reality. Those details will be revealed in an upcoming budget or economic statement, but there are a number of fiscal tools at Ottawa’s disposal to make a clean and caring economy a reality.

A decent roadmap

If we look at the speech using a clean economy and caring lens, there were four essential lines. The commitment that “climate action will be a cornerstone of our plan to support and create a million jobs across the country” is a game-changing update to the government’s narrative around climate change. The related promises to support energy-efficient building retrofits and to launch a new fund to attract investments in zero-emission product manufacturing suggest that Canada may be on the way to having a clean industrial strategy.

In stating that “the government will make a significant, long-term, sustained investment to create a Canada-wide early-learning and child-care system,” the feds recognized that the majority of job losses (63 percent) caused by the pandemic-induced economic crisis have affected women, many of whom may not be able to return to the workforce without better child-care options.

The government’s intent to wave off the fiscal hawks and continue to dig deep to help us build back better was made clear when it noted that “this is not the time for austerity.”

The government further signaled it is serious about building back better by saying it would work with the provinces and territories to “make the largest investment in Canadian history in training for workers,” with the first item listed as “supporting Canadians as they build new skills in growing [read ‘green’] sectors.”

What was missing from the throne speech?

On the green recovery side (a package of investments and regulatory reforms to relaunch the economy on the back of green industries), there was a fair bit of detail on the new investment fund meant to support zero-emission vehicles and batteries – which will largely benefit central Canada. But there was scant mention of how to rev up the low-carbon resource sector in the West. This includes (in order of technology readiness): sustainable biofuels, hydrogen, and the potential bonanza of extracting carbon fibres from bitumen.

The immense potential for the farming and forestry sectors to contribute to climate solutions was given just one line, referring to “farmers, foresters, and ranchers as key partners in the fight against climate change, supporting their efforts to reduce emissions and build resilience.”

There was no mention of how to ensure that Canadians reap our fair share of capital gains and intellectual property rights in return for the billions of dollars of public investment about to be directed at the recovery. It would have been nice to see some indication of how the government plans to ensure that our pension funds get the inside track on these growth investment opportunities in Canadian enterprises. There was also a missed opportunity to lay down markers for more democratic ownership models, including provisions to encourage employee-owned businesses and co-ops.

The next economic update and a nation building strategy

Now is the time for the federal government to go “all in” for a caring economy and a green recovery by using its fiscal power and monetary sovereignty to make the investments that will expand, mobilize and redeploy our productive capacity for building the Canada we want and the Canada we need for the 21st century.

On a long-term basis, we are going to invest an additional 0.5 percent of GDP into the caring economy to make affordable and quality child care and elder care a universal reality. And over the next five years, to ensure that Canada plays to its full potential in seizing clean-growth markets, we will invest an additional one percent of GDP per year to build up the clean economy.

How are we going to pay for it? We can issue bonds today that will be directed at investments in affordable child care, long-term care for seniors and a green recovery, and we can afford to do it without raising tax rates. We can do this because these programs stimulate economic activity that will generate future government tax revenue that will be greater than the interest on the bonds.

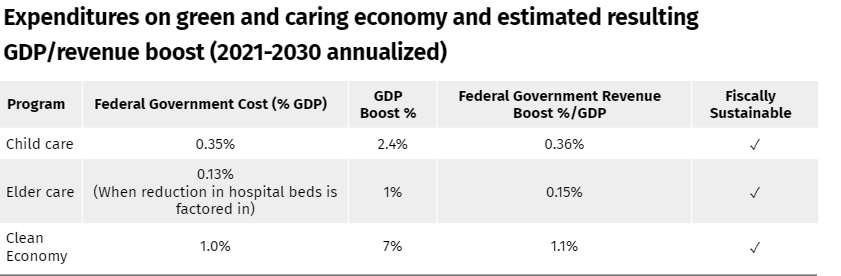

Here’s how it works: affordable child care creates jobs to deal with the “she-cession” and boosts labour force participation overall, which in turn fuels higher growth and tax revenues. A child care program (building on lessons learned from the Quebec model) would require additional federal investment of $80 billion over the next 10 years. On an annual basis, we estimate this investment would represent 0.35 percent of GDP (assuming 50-50 cost-sharing with provinces and territories). That expenditure in turn would be offset by higher economic growth – by reducing the gender workforce gap, GDP would go up a corresponding 2.4 percent by our estimates (based on an IMF paper extrapolating from the Quebec child care experience). This would represent an increase in federal revenues of $8.3 billion per year (or 0.36 percent of GDP, using the 15 percent federal revenue-to-GDP ratio).

Securing dignified long-term care as an element of universal health care almost certainly requires setting up a national long-term-care insurance program, with a strong community and home care component, according to the National Institute of Aging. Setting this up will likely require significant federal government contributions in the order of an additional 0.25 percent of GDP, assuming a matching contribution by provinces and territories. Together, this would raise Canada’s spending on publicly funded long-term care from 1.3 to 1.8 percent of GDP, in line with our OECD peers, and take some of the load off the 35 percent of Canadians who balance paid work with unpaid caregiving.

The federal contribution would be offset by higher levels of GDP. Corporate Knights estimates that GDP would rise by one percent, by factoring in a 35 percent productivity boost among the Canadians who currently balance paid work with unpaid caregiving, plus the economic boost associated with creating the new long-term care spaces, as estimated by the Conference Board of Canada. Savings in the order of 0.12 percent of GDP would arise from the hospital beds freed up through increased provision of long-term-care spaces and in-home-care support services, which are 80 percent more cost-effective.

Meanwhile, the government could support technological innovations and attract large-scale private investment into clean-growth areas that align with Canada’s strengths by issuing low-cost, long-dated sovereign bonds (issued now to lock in low interest rates). The European Union has a similar system. Corporate Knights economists estimate this would create a new engine of growth based on boosting the growth of clean industries, raising Canada’s 2030 GDP levels between five and 10 percent. At seven percent GDP growth, federal tax revenues would increase by 1.1 percent of GDP, enabling us to manage our sovereign debt loads and sustain a clean and caring economy over the coming decades.

Table:

Investing in a caring and green recovery will expand, mobilize and redeploy Canada’s productive capacity, enabling us to manage the sovereign debt and sustain a clean and caring economy over the coming decades.

Toby Heaps is the co-founder and CEO of Corporate Knights.

Céline Bak is the president and founder of Analytica Advisors.

Ralph Torrie is the president of Torrie Smith Associates, and a senior associate with the Sustainability Solution Group.

Please attribute the author(s) and mention that the article was originally published by Policy Options magazine. Editing the piece is not permitted, but you may publish excerpts.

OTTAWA – Canada’s unemployment rate held steady at 6.5 per cent last month as hiring remained weak across the economy.

Statistics Canada’s labour force survey on Friday said employment rose by a modest 15,000 jobs in October.

Business, building and support services saw the largest gain in employment.

Meanwhile, finance, insurance, real estate, rental and leasing experienced the largest decline.

Many economists see weakness in the job market continuing in the short term, before the Bank of Canada’s interest rate cuts spark a rebound in economic growth next year.

Despite ongoing softness in the labour market, however, strong wage growth has raged on in Canada. Average hourly wages in October grew 4.9 per cent from a year ago, reaching $35.76.

Friday’s report also shed some light on the financial health of households.

According to the agency, 28.8 per cent of Canadians aged 15 or older were living in a household that had difficulty meeting financial needs – like food and housing – in the previous four weeks.

That was down from 33.1 per cent in October 2023 and 35.5 per cent in October 2022, but still above the 20.4 per cent figure recorded in October 2020.

People living in a rented home were more likely to report difficulty meeting financial needs, with nearly four in 10 reporting that was the case.

That compares with just under a quarter of those living in an owned home by a household member.

Immigrants were also more likely to report facing financial strain last month, with about four out of 10 immigrants who landed in the last year doing so.

That compares with about three in 10 more established immigrants and one in four of people born in Canada.

This report by The Canadian Press was first published Nov. 8, 2024.

The Canadian Institute for Health Information says health-care spending in Canada is projected to reach a new high in 2024.

The annual report released Thursday says total health spending is expected to hit $372 billion, or $9,054 per Canadian.

CIHI’s national analysis predicts expenditures will rise by 5.7 per cent in 2024, compared to 4.5 per cent in 2023 and 1.7 per cent in 2022.

This year’s health spending is estimated to represent 12.4 per cent of Canada’s gross domestic product. Excluding two years of the pandemic, it would be the highest ratio in the country’s history.

While it’s not unusual for health expenditures to outpace economic growth, the report says this could be the case for the next several years due to Canada’s growing population and its aging demographic.

Canada’s per capita spending on health care in 2022 was among the highest in the world, but still less than countries such as the United States and Sweden.

The report notes that the Canadian dental and pharmacare plans could push health-care spending even further as more people who previously couldn’t afford these services start using them.

This report by The Canadian Press was first published Nov. 7, 2024.

Canadian Press health coverage receives support through a partnership with the Canadian Medical Association. CP is solely responsible for this content.

As Canadians wake up to news that Donald Trump will return to the White House, the president-elect’s protectionist stance is casting a spotlight on what effect his second term will have on Canada-U.S. economic ties.

Some Canadian business leaders have expressed worry over Trump’s promise to introduce a universal 10 per cent tariff on all American imports.

A Canadian Chamber of Commerce report released last month suggested those tariffs would shrink the Canadian economy, resulting in around $30 billion per year in economic costs.

More than 77 per cent of Canadian exports go to the U.S.

Canada’s manufacturing sector faces the biggest risk should Trump push forward on imposing broad tariffs, said Canadian Manufacturers and Exporters president and CEO Dennis Darby. He said the sector is the “most trade-exposed” within Canada.

“It’s in the U.S.’s best interest, it’s in our best interest, but most importantly for consumers across North America, that we’re able to trade goods, materials, ingredients, as we have under the trade agreements,” Darby said in an interview.

“It’s a more complex or complicated outcome than it would have been with the Democrats, but we’ve had to deal with this before and we’re going to do our best to deal with it again.”

American economists have also warned Trump’s plan could cause inflation and possibly a recession, which could have ripple effects in Canada.

It’s consumers who will ultimately feel the burden of any inflationary effect caused by broad tariffs, said Darby.

“A tariff tends to raise costs, and it ultimately raises prices, so that’s something that we have to be prepared for,” he said.

“It could tilt production mandates. A tariff makes goods more expensive, but on the same token, it also will make inputs for the U.S. more expensive.”

A report last month by TD economist Marc Ercolao said research shows a full-scale implementation of Trump’s tariff plan could lead to a near-five per cent reduction in Canadian export volumes to the U.S. by early-2027, relative to current baseline forecasts.

Retaliation by Canada would also increase costs for domestic producers, and push import volumes lower in the process.

“Slowing import activity mitigates some of the negative net trade impact on total GDP enough to avoid a technical recession, but still produces a period of extended stagnation through 2025 and 2026,” Ercolao said.

Since the Canada-United States-Mexico Agreement came into effect in 2020, trade between Canada and the U.S. has surged by 46 per cent, according to the Toronto Region Board of Trade.

With that deal is up for review in 2026, Canadian Chamber of Commerce president and CEO Candace Laing said the Canadian government “must collaborate effectively with the Trump administration to preserve and strengthen our bilateral economic partnership.”

“With an impressive $3.6 billion in daily trade, Canada and the United States are each other’s closest international partners. The secure and efficient flow of goods and people across our border … remains essential for the economies of both countries,” she said in a statement.

“By resisting tariffs and trade barriers that will only raise prices and hurt consumers in both countries, Canada and the United States can strengthen resilient cross-border supply chains that enhance our shared economic security.”

This report by The Canadian Press was first published Nov. 6, 2024.