The world economy’s rebound from the depths of the coronavirus crisis is fading, setting up an uncertain finish to the year.

The concerns are multiple. The coming northern winter may trigger another wave of the virus as the wait for a vaccine continues. Government support for furloughed workers and bank moratoriums on loan repayments are set to expire. Strains between the U.S. and China could get worse in the run-up to November’s presidential election, and undermine business confidence.

“We have seen peak rebound,” Joachim Fels, global economic adviser at Pacific Investment Management Co., told Bloomberg Television. “From now on, the momentum is fading a little bit.”

That sets up a delicate balancing act for governments. They’ve injected almost $20 trillion in fiscal and monetary support, in an effort to get the economy as far back to normal as is feasible in a pandemic, and can point to plenty of successes.

In the U.S., unemployment fell sharply in August and the housing market has been a bright spot. China’s steady recovery is cited by optimists as a guide to where the rest of the world is headed, while Germany is posting some decent industrial data too. And emerging markets are getting a breather from the dollar’s decline.

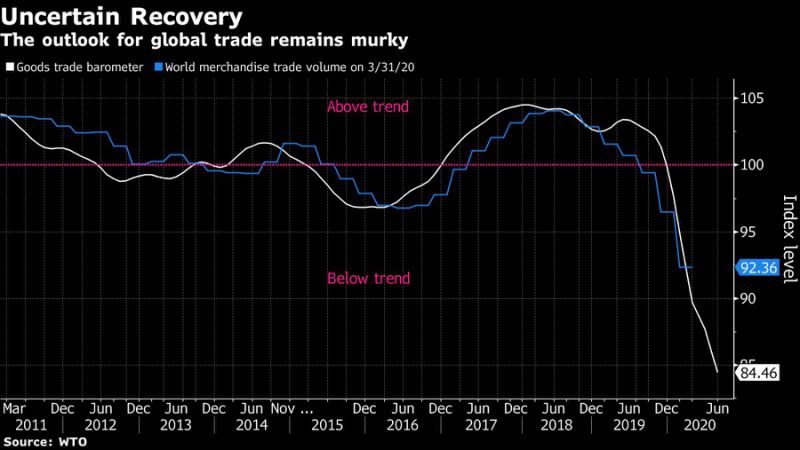

Long Slog

But keeping up the momentum on all these fronts won’t be easy. It would likely require policy makers to top up their stimulus efforts, at a point when some are looking to cut back instead. And for all the scientific progress with vaccines, they won’t be available anytime soon on the scale needed to bring the virus under tight control — a key condition for business-as-usual.

Meanwhile, there are headwinds. On labor markets, for example, government aid helped to drive an initial rebound — which may have been the easy part. Next up is the long slog of retooling businesses, reallocating resources, and retraining workers in industries that are no longer viable. That kind of restructuring could play out for some time.

Already this month, some of the world’s best known industrial brands have signaled job cuts are on the way.

A.P. Moller-Maersk A/S is planning a major overhaul that’s set to affect thousands at the world’s biggest container shipping company. Ford Motor Co. is cutting about 5% of its U.S. salaried workers, and United Airlines Holdings Inc. will eliminate 16,000 jobs next month as it shrinks operations.

There are other worrying signs too.

In China, which contained the virus months ago, consumers remain reluctant to spend and the nation’s biggest banks just posted their worst profit declines in more than a decade as bad debt ballooned.

U.S. lawmakers continue to haggle over more fiscal stimulus, which may be needed to sustain the recovery in the world’s largest economy.

Adding 1.4 million jobs in August was “a big step in the right direction,” said Ryan Sweet, head of monetary policy research at Moody’s Analytics. But the economy needs to maintain that kind of pace, he said, and “without fiscal stimulus that will be hard to do.”

‘Not Looking Good’

In Europe, gauges of activity are fading, and factories are trying to cut costs as weak demand and price cuts squeeze profit margins. While France and Germany have extended their furlough programs, the U.K. plans to end its version in October, potentially putting millions of jobs at risk.

Japanese Prime Minister Shinzo Abe, who announced his resignation last month on health grounds, warned in a press conference that “winter is coming” and the nation will need to gird to contain the virus.

What Bloomberg’s Economists Say

“High-frequency data paints a picture of a rapid rebound in the second quarter, and a stall – with activity still well short of pre-virus levels – in the third. There’s scope for further gains. If the U.S. did as well as Germany at containing the virus and getting back to work – for example – that would be a significant positive. To get back to pre-virus normality, a vaccine is required.”

–Tom Orlik, chief economist. Read more here

Stock markets are vulnerable to disappointment in economic numbers in the coming months amid a gradual curbing of emergency fiscal support.

“In terms of valuations, we’ve got to look beyond just what happened this week to the longer term,” said Catherine Mann, global chief economist at Citigroup Inc. “And the longer term is not looking good right now in terms of support for consumption, and therefore business investment and growth in the U.S. economy.”

Overshadowing everything is the continued spread of the virus, with flare-ups around the world.

Even when a vaccine is devised, making it available worldwide on the necessary scale is going to take time, according to Warwick McKibbin of the Brookings Institution and Australia National University. His models suggest that the virus could cost the world economy some $35 trillion through 2025.

“You have to get quite a lot of the population vaccinated before the economic costs start to come down,” he said.

<p class="canvas-atom canvas-text Mb(1.0em) Mb(0)–sm Mt(0.8em)–sm" type="text" content="For more articles like this, please visit us at bloomberg.com” data-reactid=”58″>For more articles like this, please visit us at bloomberg.com

<p class="canvas-atom canvas-text Mb(1.0em) Mb(0)–sm Mt(0.8em)–sm" type="text" content="Subscribe now to stay ahead with the most trusted business news source.” data-reactid=”59″>Subscribe now to stay ahead with the most trusted business news source.

OTTAWA – The Canadian economy was flat in August as high interest rates continued to weigh on consumers and businesses, while a preliminary estimate suggests it grew at an annualized rate of one per cent in the third quarter.

Statistics Canada’s gross domestic product report Thursday says growth in services-producing industries in August were offset by declines in goods-producing industries.

The manufacturing sector was the largest drag on the economy, followed by utilities, wholesale and trade and transportation and warehousing.

The report noted shutdowns at Canada’s two largest railways contributed to a decline in transportation and warehousing.

A preliminary estimate for September suggests real gross domestic product grew by 0.3 per cent.

Statistics Canada’s estimate for the third quarter is weaker than the Bank of Canada’s projection of 1.5 per cent annualized growth.

The latest economic figures suggest ongoing weakness in the Canadian economy, giving the central bank room to continue cutting interest rates.

But the size of that cut is still uncertain, with lots more data to come on inflation and the economy before the Bank of Canada’s next rate decision on Dec. 11.

“We don’t think this will ring any alarm bells for the (Bank of Canada) but it puts more emphasis on their fears around a weakening economy,” TD economist Marc Ercolao wrote.

The central bank has acknowledged repeatedly the economy is weak and that growth needs to pick back up.

Last week, the Bank of Canada delivered a half-percentage point interest rate cut in response to inflation returning to its two per cent target.

Governor Tiff Macklem wouldn’t say whether the central bank will follow up with another jumbo cut in December and instead said the central bank will take interest rate decisions one a time based on incoming economic data.

The central bank is expecting economic growth to rebound next year as rate cuts filter through the economy.

This report by The Canadian Press was first published Oct. 31, 2024