Hello. Today we look at the challenges facing the world economy, this week’s U.S. employment report and how a Chinese slowdown may impact other countries.

Feeling the Chill

The world economy is running into many headwinds as the year enters its final stretch and the northern hemisphere’s winter beckons:

- The delta variant abounds, limiting activity

- Supply chains are straining and ports are congested

- China is being rocked by a power crunch, regulatory crackdown and turmoil at Evergrande

- Food and commodity prices are surging, propelling inflation

- There are labor shortages in certain industries

- U.S. lawmakers are at odds over spending and the federal debt limit

- Central banks are starting to withdraw stimulus

Put them all together and these different forces suggest the recovery from the pandemic recession is going to be challenged in coming months, as Enda Curran writes in this rundown of all the potential spoilers.

“Expectations of a swift exit from the pandemic were always misplaced,” said Frederic Neumann, co-head of Asian economic research at HSBC in Hong Kong. “Full recovery will be measured in years, not quarters.”

This makes for a difficult job for central bankers as they juggle when best to slow or reverse supportive monetary policies. They could add to the economic weakness by acting prematurely, or alternatively they could let inflation run out of control by acting too late.

It could get even worse. Bank of America analysts told clients on Friday that oil could reach $100 a barrel for the first time since 2014 and spur an economic crisis.

“We may just be one storm away from the next macro hurricane,” analysts including Francisco Blanch wrote.

Perhaps among those faring worst is the U.K. economy.

In Bloomberg’s Big Take today, Joe Mayes, Lizzy Burden and Isis Almeida detail how Brexit is leaving the country even more isolated as it runs short of workers and faces a winter potentially tougher than any since the 1970s.

The Week Ahead

Employers in the U.S. probably stepped up their hiring in September after lackluster jobs growth a month earlier, illustrating gradual yet choppy progress toward filling a record number of vacancies.

Friday’s report from the Labor Department is predicted to show payrolls increased by about half a million last month, almost twice as much as in August, according to the median projection in a Bloomberg survey of economists. Unemployment is forecast to have fallen to 5.1% from 5.2%.

Elsewhere, global negotiators meeting to agree on a new landscape for corporate taxation will try to keep their ground-breaking deal alive in a crucial Oct. 8 gathering.

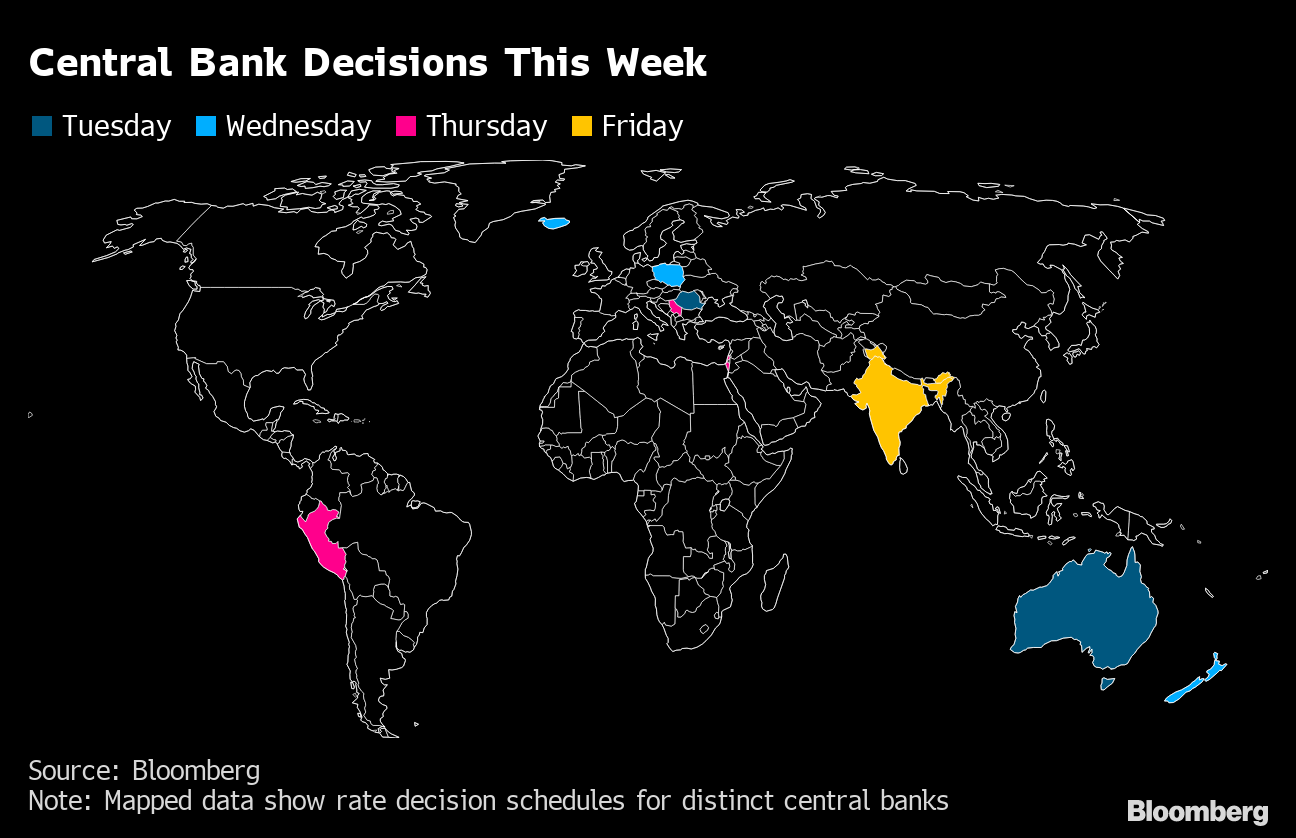

Central Bank Decisions This Week

Source: Bloomberg

Note: Mapped data show rate decision schedules for distinct central banks

.chart-js display: none;

Meanwhile, central banks in New Zealand, Iceland and Peru are among those likely to raise interest rates among several decisions due, and Japan may get a new finance minister.

Check out the world economy’s full diary here.

Today’s Must Reads

- Biden on China | The U.S. administration will directly engage with Beijing in the coming days to enforce commitments in their trade deal and start a new process to exclude certain products from U.S. tariffs.

- Debt drama | U.S. politicians are locked in a huge fight over the size of the national debt, even though investors, economists and officials are much more focused on what it costs.

- Fed trading | Federal Reserve Vice Chair Richard Clarida traded between $1 million and $5 million out of a bond fund into stock funds one day before Chair Jerome Powell flagged possible policy action as the pandemic worsened, his 2020 financial disclosures show.

- European real estate | A boom in the region’s property prices is widening the gulf between the haves and have nots, feeding anger about inequality and accusations that property markets are broken and unfair.

- American restaurants | The fragile recovery in U.S. food hospitality is sputtering. A survey found that 51% of small restaurants in the country couldn’t pay their rent in September, up from 40% in July.

- New Japanese finance chief | Former Olympics Minister Shunichi Suzuki on Monday became Japan’s first new finance minister in nearly nine years, replacing Taro Aso as the ruling party reboots its cabinet in the run-up to a general election.

- Rich pickings | Nordic countries are placing themselves in the vanguard of economies trying to get wealthy people to fund public finances more in the aftermath of the ordeal.

- Christmas at risk | Supply chain strains mean retailers are already in various forms of panic that usually don’t take hold until the weeks before the holidays hit.

Need-to-Know Research

China’s slowdown is a potential challenge for global growth.

At Citigroup, a vulnerability index indicates that exporters of manufacturers and commodities are particularly at risk to a weakening Chinese economy.

Neighbors like Taiwan and Korea are sensitive to a slowdown as are metal exporters such as Australia and Chile. Key trading partners such as Germany are also somewhat exposed.

On #EconTwitter

Read more reactions on Twitter

Enjoy reading the New Economy Daily?

- Click here for more economic stories

- Tune into the Stephanomics podcast

- Subscribe here for our daily Supply Lines newsletter, here for our weekly Beyond Brexit newsletter

- Follow us @economics

The fourth annual Bloomberg New Economy Forum will convene the world’s most influential leaders in Singapore on Nov. 16-19 to mobilize behind the effort to build a sustainable and inclusive global economy. Learn more here.