Reviews and recommendations are unbiased and products are independently selected. Postmedia may earn an affiliate commission from purchases made through links on this page.

After months of belt tightening by low- and middle-income families, it’s wealthy Canadians’ turn to worry about the economy’s impact on their pocketbooks.

People who have assets of $1 million or more say they’re more stressed out about their finances than they were this time last year, according to a new study out this morning from IG Wealth Management. More than three-quarters, or 82 per cent, say they’re worried about the economy, while 72 per cent are fretting about the cost of energy. Close to half, or 49 per cent, are concerned about rising interest rates.

“Much like other groups, high-net-worth Canadians are concerned about where the economy is going and its impact on their personal situation,” Damon Murchison, chief executive of IG Wealth Management, said in a news release.

Economic worries have become universal as inflation and climbing interest rates take a toll on most people’s budgets. Every day expenses such as grocery bills have been especially squeezed. Prices for food bought in stores rose 11 per cent in October from the same time last year, Statistics Canada data show. But the costs of some dinner staples have surged even more, with pasta prices up 44.8 per cent, lettuce up 30.2 per cent and rice up 14.7 per cent on a year-over-year basis. Meanwhile, gas prices rose 17.8 per cent in October from the same month last year. Combine that with higher debt costs from rising interest rates, and many have been forced to take an axe to their spending by cutting back on streaming services, or other discretionary purchases, to pay the bills.

And not unlike Canadians’ with lower incomes, the wealthy are also making moves to delay their retirement start dates as life grows more expensive. Close to half, or 46 per cent, say they’re changing when they’ll make the leap to full retirement. More than 50 per cent say they’ll need to keep working longer to reach their savings goals because their investments aren’t performing the way they expected.

But for high-net-worth individuals, the solution to getting through these “complicated times” financially intact is simple: get a comprehensive plan in place. That’s where a professional can step in and help, IG Wealth Management said.

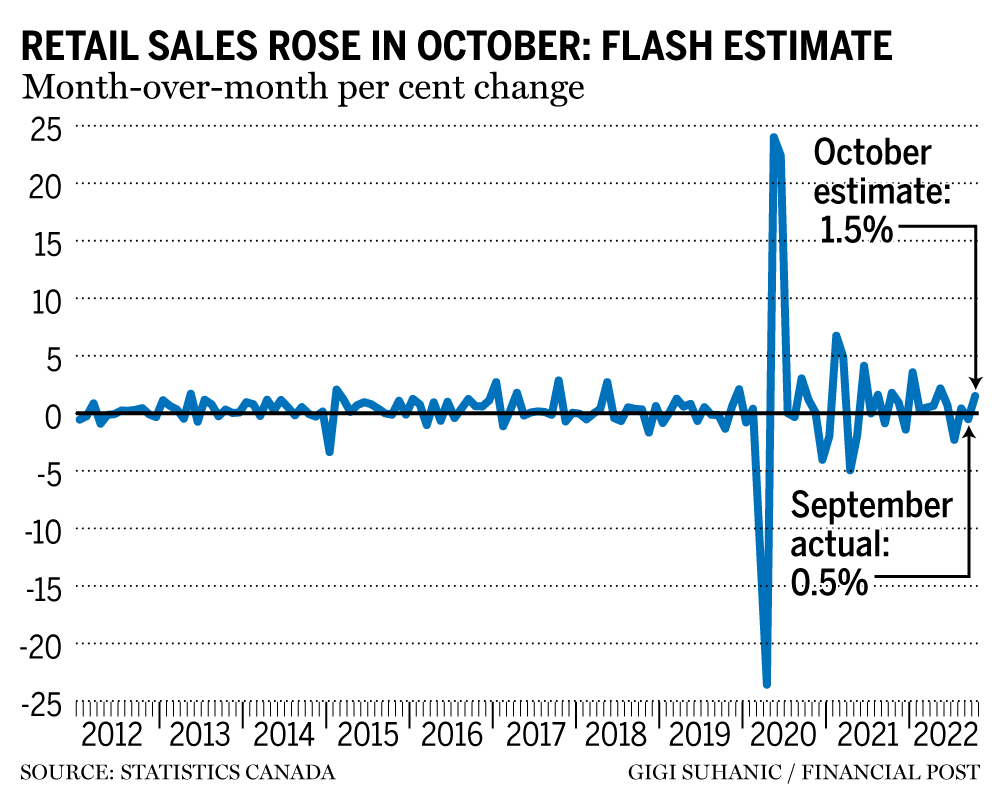

Retail sales are estimated to have risen 1.5 per cent in October, Statistics Canada said Wednesday, casting doubt on just how much the economy slowed in the fourth quarter.

Sales dropped 0.5 per cent in September and fell in seven of the 11 subsectors, representing 74.9 per cent of retail trade. It was led by lower sales at gasoline stations and food and beverage stores.

___