The surging coronavirus is stoking fears of a fresh downturn for the world economy, heaping pressure on central banks and governments to lay aside other concerns and do more to spur demand.

Hopes are mounting that COVID-19 vaccines will become available as soon as December, but widespread delivery will take months and infections are rising again in many large economies. Authorities are responding with more restrictions to limit the virus’s spread at the price of weaker economic activity.

Wall Street economists now say that it wouldn’t take much for the U.S., euro area and Japan to each contract again either this quarter or next, just months after they bounced from the deepest recession in generations. Bloomberg Economics guages of high-frequency data point to a double-dip downturn, with European factory indexes on Monday justifying that worry, though a U.S. measure of business activity was upbeat.

That leaves policy makers hearing calls for more stimulus, even when central banks are already stretched and starting to worry about froth in financial markets. Meantime, politicians from the U.S. to Europe are clashing over just how much they can and should do with fiscal policy.

“While there is much excitement over the progress of vaccine development, it will not be the quick fix that many expect it to be,” Singapore’s Trade & Industry Minister Chan Chun Sing told reporters on Monday. “Manufacturing enough doses, then distributing and vaccinating a significant population of the world, will take many months, if not years.”

Against such a backdrop, the European Central Bank is set to ease monetary policy again next month, while the Federal Reserve could concentrate more of its bond purchases on longer-term securities to push down interest rates.

But there are concerns the central banks have run out of room to act decisively and that even easier financial conditions won’t translate into an economic boost. The International Monetary Fund is among those also warning elevated asset prices potentially point to a disconnect from the real economy and so may pose a financial stability threat.

“There is a glut of savings and a shortage of investment,” which is the core problem facing developed economies, former Fed Chair Janet Yellen, who is set to be nominated for Treasury Secretary by President-elect Joe Biden, told Bloomberg’s New Economy Forum last week. “We have to have fiscal policy, structural policy other than just relying on central banks to achieve healthy growth.”

The problem is fiscal policy in the U.S. and Europe isn’t racing to the rescue. Lawmakers in the U.S. are at loggerheads over how much more to spend as Biden prepares to take office. President Donald Trump’s Treasury Department last week reduced the Fed’s ability to aid some credit markets.

In Europe, US$2 trillion in aid is being held up by a fight over political control.

“Exactly at the time central banks everywhere are acknowledging the centrality of fiscal policy in dealing with the economic consequences of the pandemic, governments are facing difficulties in implementing the next leg of their stimulus,” said Gilles Moec, chief economist at AXA SA.

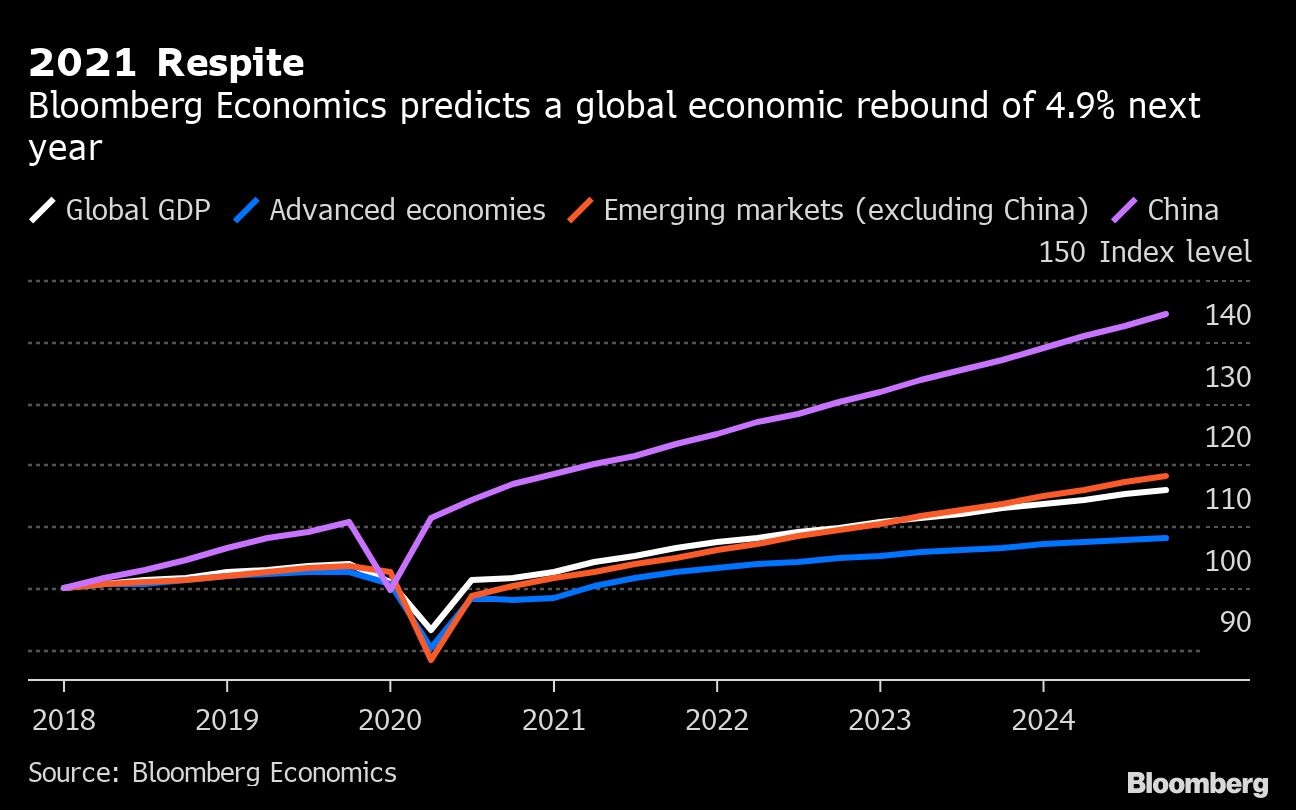

What Bloomberg Economics Says...

“Our base case is a contraction of 4.1 per cent in global output in 2020, followed by a rebound to 4.9 per cent growth in 2021. Uncertainty on the course of the virus, extent of stimulus, and timing of a vaccine mean the range of possible outcomes remains unusually wide.”

— Tom Orlik

For the U.S., the pace of infections prompted JPMorgan Chase & Co. analysts to forecast an economic shrinkage next quarter as various states impose social distancing curbs and some government benefits expire. Recent data show more people filing for unemployment benefits and fewer dining out at restaurants.

“It is possible we could have negative growth if this resurgence gets bad enough and mobility falls off enough,” Dallas Fed President Robert Kaplan told Bloomberg Television last week.

In Europe, further evidence arrived on Monday that a double-dip recession is on the way, with a survey of purchasing managers dropping sharply.

Japan’s manufacturing and service sectors worsened at a faster pace in November, early purchasing managers’ indexes showed, adding to concern over the strength of the recovery. Prime Minister Yoshihide Suga has called for a third extra budget to keep the economy on a growth path.

Both the International Monetary Fund and the Group of 20 — which comprises the world’s richest nations — warned during the G20’s meetings last weekend that the recovery is at risk of derailing despite positive news around vaccines buoying global stocks.

China is the world’s only major economy tipped to grow in 2020 as the government’s early control of the virus allowed lockdowns to be eased months ago. While its trade-led recovery is offering a boost to global commerce for now, even it’s vulnerable to the global outlook.

Reality Check

Fed Chair Jerome Powell and ECB President Christine Lagarde are among the central bankers warning against exuberance on news of successful vaccine trials.

The main reason for caution is the time needed to roll out shots for the world population to an extent enabling an end to growth-sapping movement restrictions. The announcement of a vaccine itself may drive market optimism, but doesn’t re-open economies for now.

“The vaccine gives more of a vision for what may be late next year, and what 2022 will look like, but not for the next six months,” ECB chief economist Philip Lane said in an interview with Les Echos. “The situation will not materially improve in the last weeks of 2020.”

The ECB’s downbeat tone on the immediate outlook is the backdrop to the likely arrival of a boost to the central bank’s 1.35 trillion-euro (US$1.6 trillion) emergency bond-buying program and its cheap bank loans. Policy makers meet on Dec. 10.

The worst affected sectors continue to shed jobs as companies warn on profits. Boeing Co. is almost doubling its planned job cuts while Adidas AG became one of the first consumer-goods companies in Europe to warn that renewed lockdowns will weigh on its earnings again and bring a swift end to a recent sales rebound.

The JPMorgan analysts are though hopeful that a vaccine and another round of fiscal support totaling US$1 trillion in the U.S. will be enough to deliver average growth of more than five per cent in the middle quarters of 2021. Even then, the virus’s legacies of record debt and elevated unemployment will endure.

Economists at ABN Amro Group NV however see mobility restrictions around the world lasting well into 2022.

“Only then can the global economy break into a growth spurt to make up the lost output versus trend growth,” analysts including chief economist Sandra Phlippen wrote in a report on Monday. “The vaccine is tantalizingly close, but still out of reach.”