With the latest average sale price in London, Ont., sitting well above $500,000, it’s easy to see why buying a home may be a daunting task for those making their first venture into real estate.

On top of soaring prices, buyers are also contending with competitive bidding wars and everything that comes with the COVID-19 pandemic.

Kathleen Bunt was able to come out the other side with a place to call her own in the east end of town, but the 26-year-old first-time buyer says finding her home was far from easy.

With a budget in the range of $300,000, Bunt sought a starter home that wouldn’t require a lot of work. This led Bunt to viewing more than 10 houses before deciding on her home.

“This was my first time buying a house, so I’ve actually never seen what the real estate market looks like when COVID-19’s not around,” said Bunt.

The first-time buyer said pandemic-related health guidelines forced sellers to provide tight time blocks for showing their homes to potential buyers.

“If you were even five minutes late to your showing you would lose it,” said Bunt.

“When I was buying, there was like 30 people coming to see a house in one day and by the end of day there were already offers coming in on the house, so you literally had an hour to decide if you wanted to buy the house or not.”

On top of time constraints, Bunt says current trends with offers made bidding on a home a very serious matter.

“(Offers) have to be non-conditional on anything, so you have to have your financing ready to go, you have to make sure you’ve done some sort of home inspection because if you make it contingent on a home inspection, they’ll take another offer,” said Bunt, adding that of the more than 10 houses she viewed, she only made an offer on two.

The home Bunt eventually settled on came into her hands after she outbid six other potential buyers all making offers on the same day.

“(My real estate agent) had a background in construction, so we felt comfortable forgoing the home inspection… We went kind of as high as we could go because we really didn’t want to lose this house,” said Bunt.

Even with the end in sight, Bunt still ran into issues that almost shut the door on her first home purchase.

“When it actually came down to the buying, I had a big issue with my mortgage lender and things got pushed to the end of the day,” said Bunt.

“We literally had 10 minutes to spare when I got my offer.”

Kathleen Bunt’s new home in east London.

Kathleen Bunt / Supplied

Bunt’s story is far from unique compared to what’s been seen in the London-area real estate market.

Jeremy Odland is a sales representative with the Odland and Blair Real Estate Group, which operates under Royal LePage Triland Realty.

Odland says September marked one of the busiest months he’s seen and painted a dire picture for first-time buyers.

“We actually took offers for a property that is ideal for first-time buyers (on Monday) listed at $375,000. We ended up with 21 offers and it sold for $90,000 over asking,” said Odland. “Unfortunately, that leaves 20 first-time buyers who are now very disappointed and still out there looking for that perfect home.”

With first-time buyers forced to sift through so many houses, Odland worries it may lead to buyers settling on a less-than-favourable purchase.

“It’s kind of causing a little bit of panic for some buyers… The most that I’ve had one particular client lose out on was 17 offers before they finally got a home.”

A common tactic for those failing to secure a home in London is to make a purchase in surrounding towns and cities, where prices tend to be lower, but Odland says that strategy may not always work.

“When Toronto has a crazy market, it drives Toronto-buyers out of Toronto… Now that London is so hot, we’re seeing that same trickle-down effect here,” said Odland.

“It used to be Ilderton or Kilworth was kind of where you could get a bang for your buck, but now they’re really as expensive as London, so people are kind of going further and further.”

On top of a competitive market, buyers also need to be more prepared than ever when it comes to seeking a mortgage.

That’s according to Michael Mullis, a local accredited mortgage professional with more than 10 years of experience in the industry.

“You can’t just take the mortgage company’s word for it any more it seems, you really need to educate yourself and know what is going to get you the mortgage and possibly what may hold you back from getting the mortgage,” said Mullis. “The less conditions, the better.”

Mullis warns buyers should also be aware that pre-approved mortgages are not a guarantee, adding that he had two clients as recently as Tuesday report having pre-approved mortgages denied last minute.

“Basically, look at this way: ‘Here’s what I want to do, is there anything that could stop me?’ Don’t paint a pretty picture, if anything, go through things that could go wrong.”

September brought in record numbers for the London and St. Thomas Association of Realtors (LSTAR).

With 960 homes exchanging hands, the month saw sales jump 25 per cent from the same time last year. It also marked the busiest September since LSTAR began tracking data in 1978.

LSTAR president Blair Campbell says the busy market stems from transactions that had to be put off early in the pandemic.

“We’ve had the buyers that probably would’ve transacted during the April and May period just move the timing,” said Campbell. “Really, it’s just a shift in when that volume is taking place.”

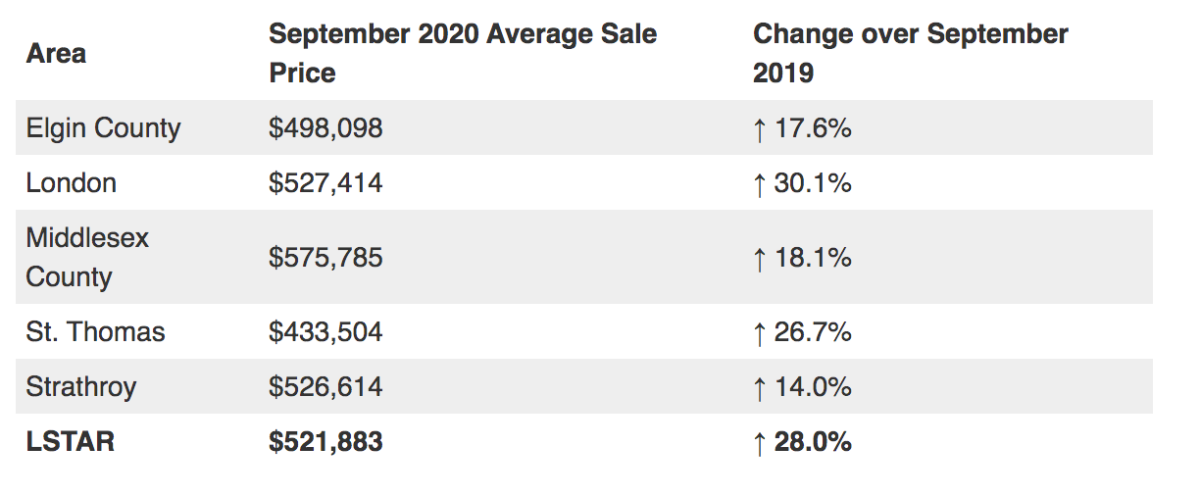

The average sale price of homes for September 2020, according to the London and St. Thomas Association of Realtors.

London and St. Thomas Association of Realtors

The average price for homes in the region also shot up to nearly $522,000, which is nearly double the price seen at the same time five years ago.

Campbell says this is partly influenced by the pandemic, with stay-at-home orders emphasizing the importance of a home.

“We have a number of buyers that are looking for more space than what they currently have,” said Campbell.

Rural areas are also seeing a spike in prices, with Elgin County’s average sale price sitting just under $500,000 while Middlesex County’s average stands just over $575,000.

“That’s a little bit of a pandemic-effect as well, where people are looking for less populous areas… either smaller towns or country properties where they’ve got more space, their neighbours are a little more spaced out,” said Campbell. “If you’re working from home, the commute’s no longer an issue.”

For those looking to make a purchase, Campbell says it’s important to be prepared for offers to fail and have a place to live in the meantime.

“If you’re not the person who gets that property, say, ‘well we’ll move onto the next one.’ That’s kind of the mindset you need to have in order to be successful,” said Campbell.

“It is a tough time, so I certainly sympathize with the first-time buyers right now.”

© 2020 Global News, a division of Corus Entertainment Inc.