Growth in services-producing industries was offset by a decline in goods-producing industries

Author of the article:

Publishing date:

Jul 29, 2022 • 6 hours ago • 2 minute read • 5 Comments

Article content

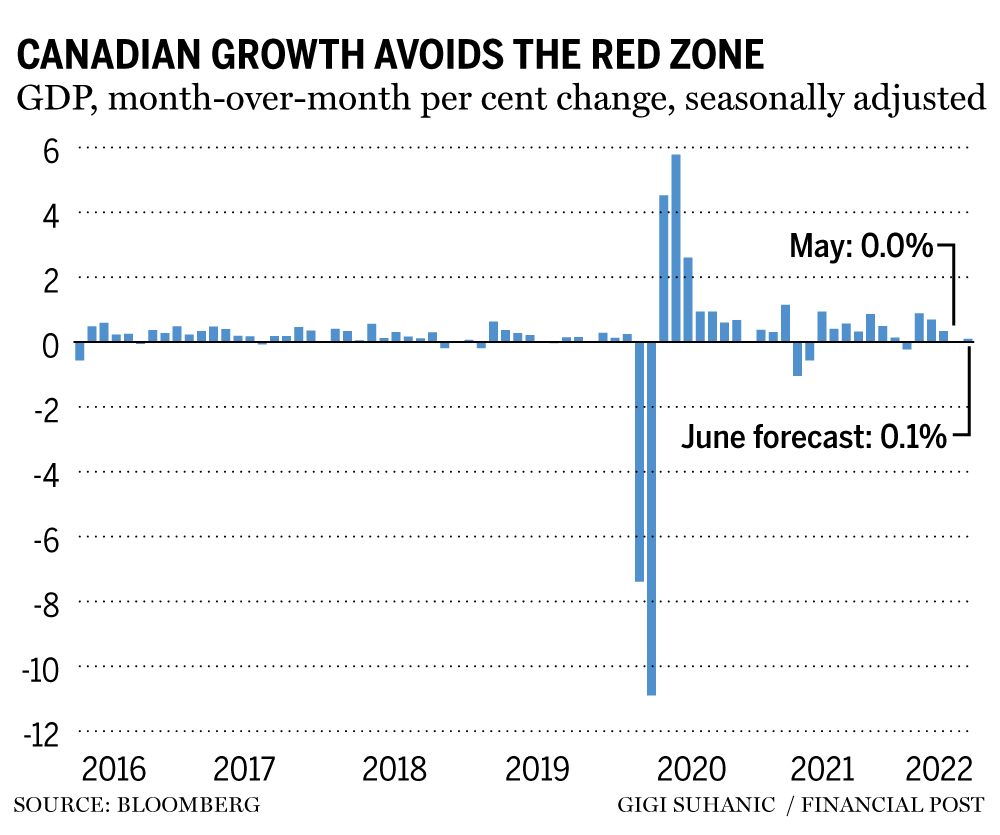

Canada’s economic expansion showed signs of moderation in May and June, pulling back from a strong start to the year in the face of high inflation and rising interest rates.

Article content

Output in June was on track for a small increase of 0.1 per cent after stalling in May, Statistics Canada said on Friday. That follows three months of strong growth between February and April that helped fuel a robust expansion in the second quarter, which the agency estimated at about 4.6 per cent annualized.

The results show a picture of an economy that was unscathed from the global slowdown in the first part of the year but may be entering a period of much slower growth.

The Bank of Canada has raised its benchmark policy rate by more than two percentage points since March to slow four-decade high inflation, and is expected to continue hiking by at least another half-percentage point at its next policy decision in September.

Article content

The second-quarter growth number was even stronger than the four per cent annualized pace estimated by the central bank earlier this month, and represents an acceleration from growth of 3.1 per cent in the first quarter.

“The Bank of Canada is still on course to deliver another non-standard rate hike at its next meeting,” Andrew Grantham, an economist at Canadian Imperial Bank of Commerce, said in a report to investors.

The Canadian dollar was little changed on the report, down 0.2 per cent to $1.2838 per U.S. dollar at 8:51 a.m. in Toronto trading. Yields on Canadian government two-year bonds rose about four basis points to 2.97 per cent.

While the global economy has been hit hard by rising energy costs, Canada’s resource-based economy has been benefiting from elevated oil, grain and gas prices. The strong first half pace also reflects reopening effects earlier this year, after strict COVID-related lockdowns last winter.