Some economists are proclaiming that the Canadian housing bubble has burst. Housing markets have indeed slowed considerably since their peak in February and March, but, unfortunately, economic bubbles are notoriously hard to identify and are often observed only after they burst.

Article content

A review of housing market indicators quickly reveals that any conclusions about the state of housing markets depend upon the benchmarks used to study them. The peak-to-trough comparisons suggest much higher price declines than what year-over-year comparisons reveal. The reference points are not as material in comparing the decline in sales, which are considerably down year over year and from peak to trough.

Advertisement 3

Article content

A recent report by RBC Economics concluded that the expected slowdown in housing sales and prices has been the result of soaring interest rates. RBC expects interest rates to rise further and forecasts the “national benchmark price to drop 14 per cent from (quarterly) peak to trough.”

Again, benchmark prices can differ from average prices, which do not account for the differences in housing quality and size over time. The sales activity during recessionary times can switch from larger, higher-quality homes to smaller, lower-quality homes; hence, any change in average prices will not represent the change in the price of an average home.

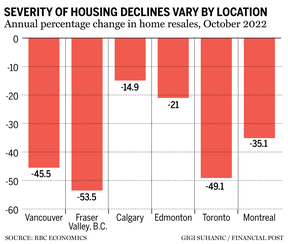

At the same time, some housing markets will experience a more significant decline in sales and prices than others. For example, the RBC report shows housing activity in Calgary has shown more resilience than in Toronto.

Consider that the MLS Home Price Index (HPI), which controls for differences in housing size and quality, declined in Toronto by 1.3 per cent in October from the same time last year, while Calgary was up by 9.1 per cent.

The peak-to-trough declines were also more pronounced in Toronto than in Calgary. The HPI in Calgary declined by 4.2 per cent in October after peaking in May. In Toronto, the index was down 18 per cent from its peak in March. The RBC report noted that declining prices in Toronto have already returned half the gains realized during the pandemic.

The decline in housing transactions is steeper than prices. October sales were down by 49 per cent in Toronto from the same time a year ago. Other large housing markets showed lower annual declines, with Vancouver declining by 45.5 per cent and Montreal by 35 per cent. Annual housing sales in Calgary dropped even less, at 14.9 per cent.