How will Canadians service $1.56 trillion in mortgage debt plus other debts such as credit cards? What about tenants who can’t pay their rent?

By Steve Saretsky, Vancouver Residential Realtor, Stevesaretsky.com:

We live in interesting times. I have been fielding a lot of questions regarding the market turmoil and what it may mean for the Canadian Real Estate market, particularly Vancouver. Yes it’s true, the S&P/TSX Composite Index fell 12% on Thursday, the biggest one day drop since May 1940 per Bloomberg. Surely this will all have serious implications, but what does it mean for our beloved housing?

The short answer is, I don’t know. Nobody does. What I can tell you is there are a few things I’m watching very closely and a few possible outcomes worth considering.

First, this is absolutely an economic shock, one that the Bank of Canada is probably ill-prepared for, just like the rest of us. Canadian households are the most indebted in the G7. We chose not to take the medicine in 2008, and thus, household balance sheets remain bloated today. The household debt servicing ratio sits at a record high, despite low interest rates.

Further, household savings rates are near 60 year lows. In other words, there’s not a whole lot of cash put aside for a rainy day, households are not well positioned for an economic shock.

This shock will unfortunately result in a hit to incomes, and will bring rise to job layoffs. Thus, servicing debts becomes increasingly difficult. Further, this is not something that can be fixed by lowering interest rates. We have a global pandemic where policy makers are encouraging people to disengage from economic activity. In other words, avoid restaurants, organized events, and travel — the very thing that makes society function and drives consumer spending, which accounts for over 65% of GDP. Remember, one man’s spending is another man’s income.

And so, this leaves us with a host of questions to ponder. How will Canadians service $1.56 trillion in mortgage debt, not to mention other debts such as credit lines and credit cards? What about tenants who can’t pay their rent?

Perhaps we should look at how other countries are coping. In Hong Kong, the Government will cut a check for HK$10,000 to every resident. In Italy, the Government is working with the banks to get a moratorium on mortgage payments. In the city of San Jose, they have adopted a moratorium on evictions for residents who can’t pay rent because of lost income resulting from the coronavirus outbreak.

These all seem entirely plausible in Canada. You can debate the moral hazard around it, and whether it’s the right or wrong thing to do, however we might not have a choice.

In terms of the overall real estate market, I suspect we will see a halt in activity. Not just a slowdown in sales, but in new listings as well. You won’t see this reflected in the data for several months, mostly because of the lag time for data processing. Further, while it seems logical prices could drop, if they do, that also won’t be reflected in official price metrics for many months. Due to the emotional nature of real estate, nobody cuts their price overnight. Unlike stocks, there is no mark to market on a daily basis.

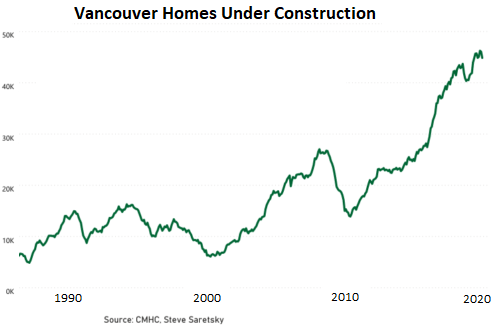

I’m also thinking a lot about new construction projects, which are capital-intensive and often funded using significant amounts of leverage. Every month sales are delayed, carrying costs add up, putting profit margins under pressure. Further, closing risks are no doubt something to consider, should pre-sale buyers have a change in their employment status upon completion.

This comes as we are expected to see a record number of new completions this year with the number of units under construction at all time highs. Units under construction across Metro Vancouver.

Lastly, I am thinking a lot about the private credit market. We know private mortgage lending has been growing at a rapid pace these past few years. It’s estimated to be about 10% of new mortgage loans issued. This increases renewal risks for buyers who, again, might have a change in employment as the loan comes due. Most of these mortgage are one year terms.

.adsense_mobile_unit display: none;

@media only screen and (min-width:320px) and (max-width:480px) .adsense_mobile_unit display: inline-block; width: 320px; height: 50px; text-align: center;

Further, I would not be surprised to see Mortgage Investment Corporations halt redemptions on their investors, in order to stem liquidity issues from investors wanting to pull their money from the fund. Many of these mortgage investment corporations borrow on a line of credit from a bigger bank. Will these loans be recalled? In a best case scenario, we should at least expect an increase in private mortgage rates in order to account for the increased market risks.

As I have said, nobody knows how this will play out. I have heard from others in the industry that they expect real estate to act as a “flight to safety” and thus it won’t be impacted. I personally don’t share that same view. But perhaps they are proven correct and my concerns fail to materialize. To be honest, I hope they are right. Nothing is more destructive than a sharp decline in home prices. However, I am well aware there are others desperately hoping for this type of event.

Regardless, I will keep you all updated on how the situation develops. We all know how important Real Estate is to the Canadian economy, irrespective of your views of the current housing market. Now more than ever, we will need to navigate these waters carefully. Stay tuned, and stay safe. By Steve Saretsky.

The Fed is going nuts trying to contain this. Read… As Everything Bubble Implodes, Frazzled Fed Rolls Out Fastest Mega-Money Printer Ever, up to $4.5 Trillion in Four Weeks

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.