Upscale market likely in a position to better weather higher rates: Sotheby’s report

Reviews and recommendations are unbiased and products are independently selected. Postmedia may earn an affiliate commission from purchases made through links on this page.

Article content

_____________________________________________________________

Advertisement 2

Article content

Good morning!

You might not expect it, but even Canada’s luxury housing market has come down to earth — sort of.

“Canada’s luxury market is normalizing following its historically anomalous performance as rising mortgage rates, escalating inflation and global geo-economic headwinds progressively temper real estate consumer sentiment,” said a report this week from Sotheby’s International Realty Canada.

Luxury homes sold at a frenetic pace through the pandemic, peaking in the first quarter of 2022 when sales of homes costing more than $4 million in the Greater Toronto Area (GTA) soared 30 per cent from the year before. The pace has since “moderated,” the report said. Sales and prices are still up in the luxury sector, just not as much.

Advertisement 3

Article content

Calgary leads the luxury pack as revived economic prosperity returns to Canada’s energy capital. Sotheby’s said strong gains were posted in the city’s luxury $4 million-plus market, with five single-family homes sold in the first half of 2022, compared with none sold in that price range during the same period last year. Further, sales of single family homes and luxury attached properties over $1 million rose 36 per cent year-over-year and 85 per cent, respectively.

“By mid-year, the Calgary luxury market was recalibrating to a healthy, active, but more balanced market. Sales velocity moderated, multiple offer scenarios became less frequent, and prices stabilized in many neighbourhoods,” the report said.

Advertisement 4

Article content

In the GTA, sales of properties worth more than $4 million were up seven per cent from the first half of 2021. Sixteen homes worth more than $10 million sold in the first half, one more than at the same time last year. Condominium and attached home sales in the $4-million-plus category rose 13 per cent and 100 per cent, respectively, in the first half of 2022.

Sales of luxury condos, attached and single-family homes topping $4 million soared 71 per cent in Montreal during the first half of the year. Sales of $1 million-plus homes, however, dropped one per cent.

Vancouver was the laggard, moving from “frenzied” buying in the first quarter to a “retreat” in the second quarter. During the first half of 2022, luxury residential real estate sales, including condominiums, attached and single-family homes, declined 18 per cent year over year to 203 properties. Nine ultra-luxury residential sales ($10-million-plus) were recorded in the first half, down from 16 a year earlier.

Advertisement 5

Article content

Overall, the “conventional market” appears to be faring worse, with sales down 24 per cent in June from the year before and the average price falling two per cent, according to data from the Canadian Real Estate Association last week.

Sotheby’s chief executive Don Kottick said the luxury and ultra-luxury sectors are likely to strike their own paths in Canada’s shifting housing market based on the fact, among others, that wealthier buyers will have “greater financial resilience to adapt to rising interest,” he said in a press release. “Conventional homebuyers may require more time to adapt budgets to the new reality.”

In the meantime for those in the ultra-luxury market, here are some listings billed as the most expensive properties for sale in Canada, according to Point2 analysts. The international real estate portal compiled a list of the top homes on the market by province and by major metropolitan area.

Advertisement 6

Article content

The most expensive property on a provincial basis is an 8,700-square-foot mountain estate listed at $39 million in British Columbia.

In the city category, Point2 found a Mississauga, Ont. home listed at $37.5 million is the most expensive home in the country.

If you are looking for a place to hang your hat that has 14 bathrooms and a nightclub, this is it.

_____________________________________________________________

Was this newsletter forwarded to you? Sign up here to get it delivered to your inbox.

_____________________________________________________________

- Prime Minister Justin Trudeau will make a clean energy announcement in Halifax

- Transport Minister Omar Alghabra, Mayor Amarjeet Sohi and Tom Ruth, CEO of Edmonton international airport, will make a funding announcement to support trade corridors

- Minister of Finance Selina Robinson and Jonathan Sheppard, president of the Home Inspectors Association BC, announce new consumer protections in the real estate market, based on advice from the B.C. Financial Services Authority.

- Minister of Jobs, Economic Recovery and Innovation Ravi Kahlon, Abbotsford Mayor Henry Braun and Joy Johnson, president and vice-chancellor of Simon Fraser University, make an announcement relating to the future of agritech in B.C.

- Today’s Data: U.S. initial jobless claims

- Earnings: Mullen Group Ltd., AT&T, Snap

Advertisement 7

Article content

_______________________________________________________

_______________________________

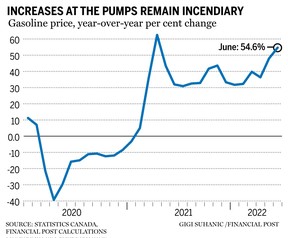

Inflation in Canada registered at a bone-chilling 8.1 per cent in June compared with a year earlier, the largest increase since January 1983, according to Statistics Canada, which released the anxiously awaited Consumer Price Index (CPI) reading on Wednesday.

Advertisement 8

Article content

Once again, the largest culprit in the unrelenting rise in the cost of living was the price of gasoline. It was up 54.6 per cent in June from the same month in 2021. Still, remove gasoline from the equation and the June CPI rose 6.5 per cent from the same time last year.

Based on these numbers, FP editor-in-chief Kevin Carmichael warns that the Bank of Canada’s goal of a soft-landing is looking harder and harder to pull off. Read the full story here.

____________________________________

Despite the ongoing pandemic, a looming recession and inflation hitting a 40-year-high in May, many Canadians are still eager to take to the skies this summer.

And because money is tight, sales and discount codes will be an important part of planning for their dream getaway.

Advertisement 9

Article content

Our content partner MoneyWise can help you to save and spend at the same time, by making smart use of your travel and credit card loyalty points.

Knowing the dollar value of your points and the best times to use them can help you budget for your next big trip

____________________________________________________

Today’s Posthaste was written by Gigi Suhanic (@GSuhanic), with additional reporting from The Canadian Press, Thomson Reuters and Bloomberg.

Have a story idea, pitch, embargoed report, or a suggestion for this newsletter? Email us at [email protected], or hit reply to send us a note.

Listen to Down to Business for in-depth discussions and insights into the latest in Canadian business, available wherever you get your podcasts. Check out the latest episode below: