Maybe it’s too many months living and working in the same cramped quarters. Or the ultra-low mortgage rates. For some, spending less during the pandemic means they finally have enough saved for a down payment.

All that is prompting people to ask themselves whether now is the time to buy a home — even as the long-term outlook for the real-estate market remains uncertain.

There’s been a burst of home buying across the U.S., especially in suburbs outside cities where people were cooped up during the spring Covid-19 lockdown. In August, contracts to buy single-family houses in Greenwich, Connecticut, nearly tripled from a year earlier. Contracts were up 57% in nearby Westchester County.

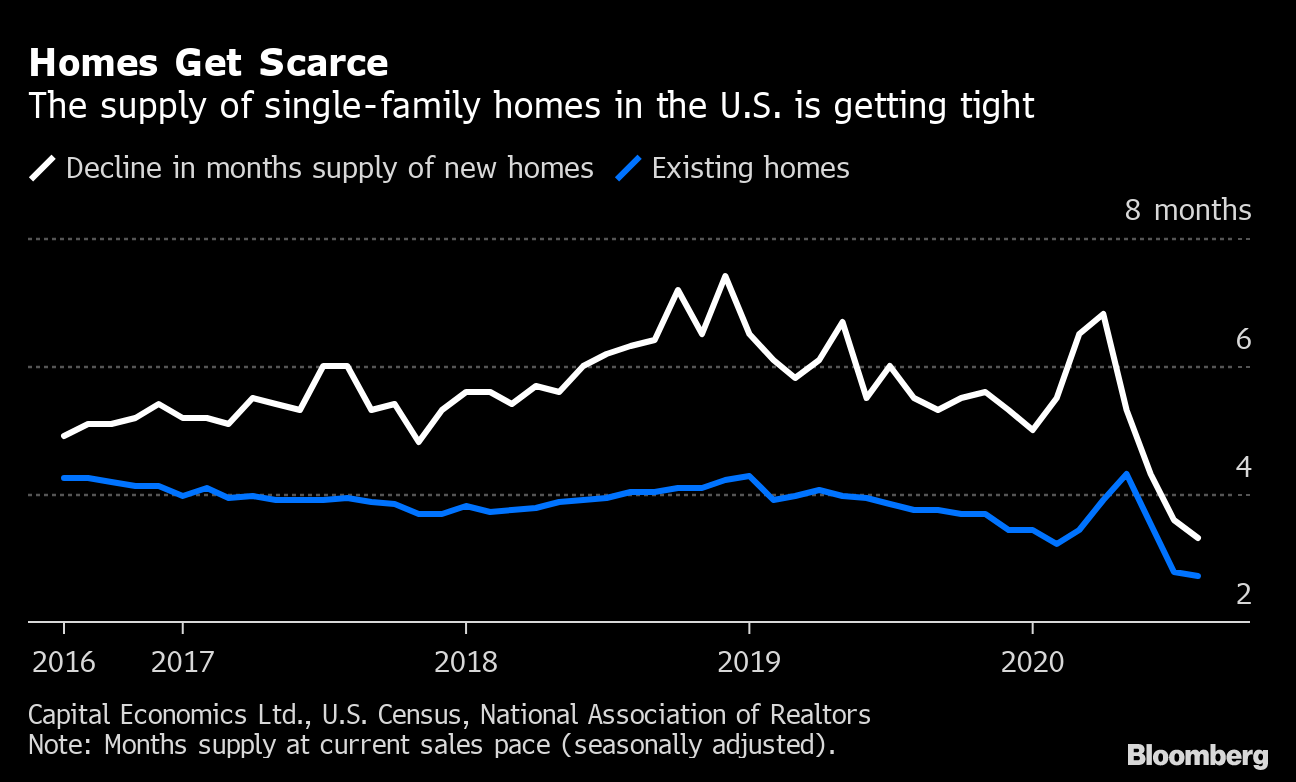

Homes Get Scarce

The supply of single-family homes in the U.S. is getting tight

Capital Economics Ltd., U.S. Census, National Association of Realtors

Note: Months supply at current sales pace (seasonally adjusted).

.chart-js display: none;

The U.S. market is so hot that the supply of homes for sale is running low, threatening to push up prices and put ownership out of reach for many Americans. Homebuilders are struggling to alleviate the supply problem as they deal with building-material shortages and surging lumber costs. And bidding wars have become common again.

It’s not just the U.S. In the U.K., July home sales were the highest in more than a decade. A new report from UBS Group AG found that hot housing markets in cities including Munich, Frankfurt, Toronto and Hong Kong are vulnerable and at risk of a “sharp correction.”

“In almost every community you’re probably overpaying by some metric right now,” said Ilyce Glink, author of “100 Questions Every First Time Home Buyer Should Ask.” “Prices are getting pushed to where they aren’t affordable even with the historically low interest rates.”

Glink still recommends buying to those who can swing it. Overpaying a bit now doesn’t matter as much if you’re planning to stay in the home long term, she said. The questions she says first-time buyers should ask themselves include:

How long do you plan to stay in the area?

How much money do you have for a down payment?

If companies require workers to begin commuting again, will that large, leafy property in the suburbs still seem as attractive?

How set are you financially with your job? Do you see a career change ahead?

Are you prepared to spend much more on maintenance and taxes than you have as a renter?

Home buying isn’t for everyone. While there are financial benefits to owning property — the value could increase, and mortgage interest can be tax-deductible — you lose the flexibility that comes with renting. And property taxes, maintenance, insurance and unplanned expenses mean there is much more to consider than just whether or not a mortgage payment is cheaper than rent.

Bloomberg spoke with people across the world about what went into their decision to buy — or wait.

Alexis Strober and her husband, Ben, outside their new home in High Falls, New York.

Courtesy: Alexis Strober

Alexis Strober had been living in New York City for the past 14 years, most recently in Battery Park City.

She’d enjoyed getting away to the Hudson Valley with her husband and their two young boys, and they’d looked at vacation homes to buy in the area, about a two-hour drive from the city.

When the pandemic hit, they decided to transform their lives, give up their city lease entirely and move upstate. In April, they closed remotely on a house they had previously considered for a second home, paying $303,500.

“The big driver to get rid of the apartment and be up here full time was really because of the childcare and the schooling options,” Strober said. “Our younger son is two and a half, so it’s really impossible to get any work done with him in the house. We found great day care and nursery school options for him here.”

The new home in rural High Falls has a fireplace, a large backyard, and much more space, something they were missing in Manhattan after lockdown began. The family has been doing a lot more hiking and just bought a car.

The savings have been enormous. The Strobers’ new mortgage payment is a little more than $1,000 a month, versus $5,500 rent for the Battery Park City apartment.

One downside: Fewer food options. “It’s been a little bit of a culture shock,” Strober said. “There’s three restaurants in town, and they are all closed on different days. I’ve been doing so much cooking.”

Plenty of Choice

The number of apartments for rent in Manhattan is soaring

Source: Miller Samuel Inc. and Douglas Elliman Real Estate

.chart-js display: none;

After sending their youngest child off to college this fall, Gerard O’Beirne thought he and his wife Anne would sell their Westchester County house after more than two decades and buy an apartment in Manhattan.

But the pandemic made them question whether that was the smart move. They decided to rent in the city instead.

“A lot of my clients are fleeing New York City,” said O’Beirne, a tax partner at accounting firm EisnerAmper. “Maybe it would be the right thing to rent for a while and see how things play out.”

The flexibility, market uncertainty and tax considerations all contributed to the couple’s decision to rent.

They recently listed their Pelham, New York, home for about $1.2 million. They are looking for rentals on the Upper East Side, to be close to the EisnerAmper midtown office and to their daughter, who lives on the east side. They want to spend $5,000 to $6,000 a month for a three bedroom, which would allow them to keep a home office and a guest bedroom for the kids to stay in. That compares with their old mortgage payments of about $4,800 a month.

O’Beirne said he will save money in other areas by not owning in the suburbs.

“My Metro North ticket was $275 a month,” he said. “Back and forth to the train was another $100 a month. Maintaining two cars and insurance on two cars. Lawn maintenance every week. The utilities to run a house our size. Every time you turn around there’s a new bill, and it all adds up.”

#lazy-img-365218079:beforepadding-top:75%;

Henry Palmer thinks he overpaid for the place in upstate New York, but he is enjoying his new, rural life after moving out of the city.

Photographer: Henry Palmer

Henry Palmer has been a city person his whole life. The British expat and self-described “city-center boy” moved eight years ago from London to New York, where he worked as a vice president at Citigroup Inc. before joining a software startup.

Until now. Palmer and his wife, in their late 30s, packed up their 600-square-foot downtown Brooklyn apartment and headed somewhere more bucolic where they could work remotely. They settled on a home in Smallwood, New York, a rural area about two hours northwest of New York City.

The new home is surrounded by forest instead of concrete. At 1,100 square feet, it’s nearly twice the size of Palmer’s old apartment.

Palmer paid $365,000 for the Smallwood home. His new $2,500 mortgage payment is a nice discount from the $3,600 rent paid in Brooklyn.

Palmer said he and his wife were worried about the market — but because they were part of the frenzy of city dwellers that snapped up places in the country. They had to put offers on five or six different houses and move toward the top of their budget after repeatedly getting beat out by all-cash offers from tech workers fleeing the city. He thinks he probably overpaid.

“The knock-on effect of the pandemic was quite shocking,” he said. “The place we ended up buying is worth maybe 75% of what we paid.”

Palmer has been in the new home for about a month. He’s enjoyed the quiet outdoor space, the savings, and having a car for the first time — even though it’s a bit strange that he now needs to drive just to get some milk.

Greg McVay gave up his rental apartment in March and moved into his boyfriend’s Lower East Side studio to spend lockdown together. It was the two of them, a poodle and an overweight cat in 550 square feet. They soon began looking for a rental one-bedroom with outdoor space in Brooklyn’s Williamsburg neighborhood. When they crunched the numbers, they realized something surprising: They could afford to buy.

“We didn’t really have to compromise on anything, and money is cheap now,” said McVay, 34, a manager for a life sciences company.

In June, they toured their first condo listing — on the waterfront with a terrace and a home office — and put in a half-serious, low-ball bid. They offered $999,000 for a 892-square foot apartment listed for $1.195 million.

“We were just trying to test the market,” said McVay’s boyfriend, Scott Topel, 29, an interior designer.

In the next two months, they toured 40 other places before returning to the original apartment. The seller had dropped the price to $1.175 million; they came to a deal at $1.15 million — with a $25,000 credit to cover closing costs. The couple, who secured a 10-year adjustable-rate mortgage at 2.85%, will complete the deal in October.

It was a different experience from when Topel bought his Lower East Side studio in 2015, when there were already two competing offers for the place within hours of the first open house, he said. He plans to rent it out when they move.

“There’s an opportunity for people who couldn’t afford New York — and now, New York is slightly more affordable,” McVay said. “I’ve been in the city nine years and could never imagine buying something like this.”

After years of renting, Ashley Brown and her partner decided to buy this Atlanta home.

Courtesy: Ashley Brown

Ashley Brown, 31, and her fiancée Aaron Shuman, 30, have been apartment hopping in Atlanta for the past three years. They’ve had to deal with terrible management companies, crazy utility bills and cockroaches. Renting was losing its appeal.

They thought about buying a place of their own but worried about the economy. They’re self-employed artists who lost business during the pandemic. Back in May, they had their doubts.

“We were still kind of a little uncertain about what was happening with the coronavirus and how that was going to shake out,” Shuman said.

Still, they started looking at houses and were surprised by how much of a seller’s market it seemed to be. When Shuman saw a listing pop up for a $239,000 two-bedroom house in a historic suburb of Atlanta, he cancelled his afternoon meetings. That afternoon, they took a look and made an offer.

Four other people also made offers, some higher, but Brown wrote a personal letter that the sellers said they loved. The sellers asked them to match the next-highest bid of $245,000 and threw in $6,000 in closing costs.

Brown is a musical theater artist and web designer while Shuman is a music instructor and business owner, and they wanted to have a cash cushion even after the purchase. They assumed they needed to put down 20%, but the numbers started to work when a lender offered a mortgage with 5% down and around $100 a month in private mortgage insurance.

Within the first week of moving in, Brown posted in a local Facebook group asking how to take care of the plants in the front yard. To her surprise, the former owner of the house responded and offered to help.

“She came over 10 minutes later,” Brown said.

CHICAGO

Matt Smith-Daniels, a 30-year-old career consultant, was finding it difficult to work from home in downtown Chicago. His 27th floor rental, a 750-square-foot studio with floor-to-ceiling windows, used to be his dream apartment. That changed after spending his entire day working and living in the same room.

He revved up his search to buy a place for himself. He was looking at townhouses, but he was surprised to find that property values in Chicago had gone up, and not down. He also worried that higher taxes and more people working from home would mean less interest in downtown property.

“I took the long-term view,” Smith-Daniels said. “I’m probably buying this place at its most expensive price, and it’s just not worth it right now.”

Meanwhile, rental prices were low. So he upgraded to a more spacious apartment. His new place is $2,700 a month for two bedrooms and two bathrooms. It’s only three blocks down from his current studio — for which he pays $2,550 a month — and this apartment has an even better view, he said.

SYDNEY

Joel Grant, 30, and his partner had been living with his parents for two years when the pandemic hit. Reduced rent meant they saved money, but it became too tight a squeeze with everyone working from home.

“Our attitude with the property market is that we wanted to get in,” said Grant, a manager for the Duke of Edinburgh’s International Award Foundation. “We’re not looking to sell in the next five years anyway, so even if it does dip, we’re not going to suffer too much.”

As he went back and forth with his partner about whether now was the right time to buy — Were their incomes secure? Were prices about to plummet? — a slew of Australian government support bolstered his confidence. There were incentives for first-time home buyers, for builders and breaks from mortgage payments. The perks kept coming.

“The government will put in place things to keep the property market alive at all costs,” Grant said. “If the property market really crashes, then Australia is doomed economically.”

Searching during the height of uncertainty about the pandemic actually had one plus: less competition, particularly from investors who’ve been blamed for pushing first-time buyers out of the market.

In August, they managed to find a two-bedroom townhouse on a quiet road in Ashfield, an up-and-coming suburb about 6 miles from Sydney’s central business district. Like many properties in Sydney it was scheduled to go to auction — a frenetic affair where prospective buyers and onlookers gather on the front lawn with an auctioneer whipping-up emotions and driving the price higher.

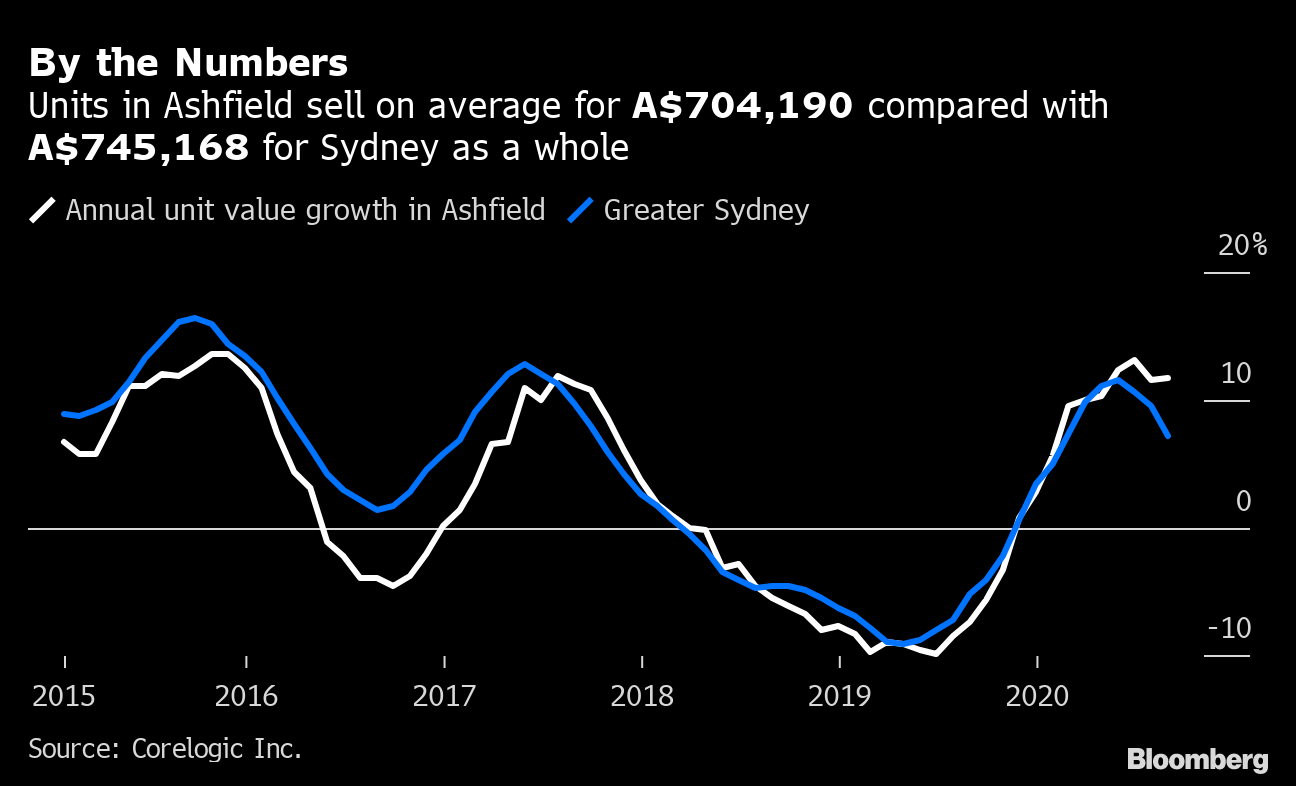

By the Numbers

Units in Ashfield sell on average for A$704,190 compared with A$745,168 for Sydney as a whole

Source: Corelogic Inc.

.chart-js display: none;

Sensing there was less competition in the market, they took a chance and made an offer four days before auction. It was accepted the next day. Grant declined to say how much they paid.

“Covid worked in our favor there,” Grant said. “I think the vendor was unsure about auction interest because of the pandemic, so they jumped on our offer.”

Rendering of what Katie Larson’s home in the English countryside will look like when finished. Her family considered renting but ultimately decided to buy.

Courtesy: Katie Larson

Katie Larson and her husband needed to move out of London to enroll their son in a specialized school in the English countryside. They were renting in London — a 5-bedroom, 1,600-square-foot flat that cost 3,400 pounds ($4,430) a month — and figured they would do the same in the Cotswolds.

That quickly proved difficult. Like many others during the pandemic, they adopted a dog — and finding a landlord who would allow pets narrowed their choices. Every time they wanted to view a property, they’d drive two hours only to find houses in “awful” condition and yet in high demand.

“It was depressing,” she said. “You would look at a house and it would get taken, or there’ll be a waiting list for it.”

They looked at older homes, but most needed work just to move in. One, she recalled, had carpeted bathrooms.

She decided to go with a newly built home in Chipping Norton, a town of about 6,300 people in Oxfordshire. They are spending more than £600,000 for the 1,800-square-foot, four-bedroom house. Their monthly mortgage payment is £2,250.

They took advantage of a property tax break offered this year by the U.K. government to stimulate the economy during the pandemic, saving about £15,000.

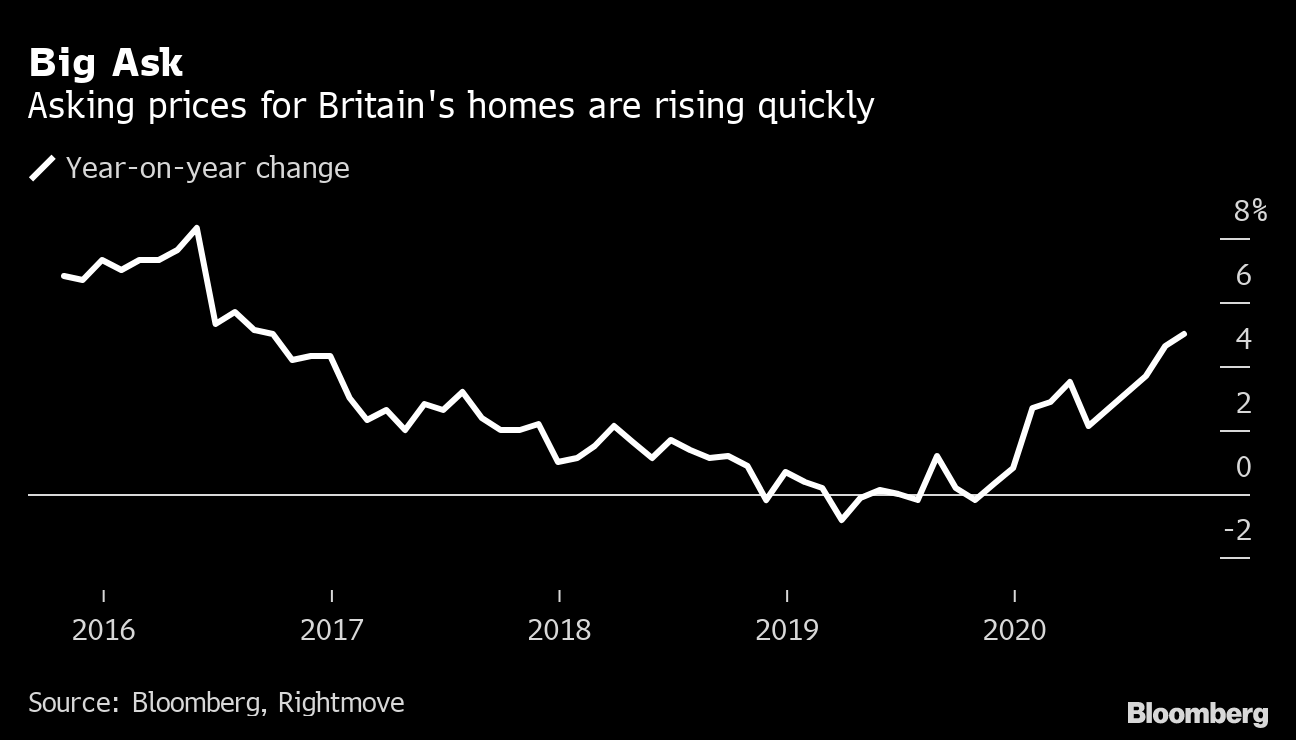

Big Ask

Asking prices for Britain’s homes are rising quickly

Source: Bloomberg, Rightmove

.chart-js display: none;

“Do I miss London, and where we lived for the past five years? Yes, totally. But it’s beautiful here, and I think we’ll really get to start to enjoy it once we do get in our house,” she said.

Even though she doesn’t consider this a “forever home,” she says the family is planning on staying for at least five years, so she isn’t worried about the market slipping in the short term.

Housing affordability is a key issue in the provincial election campaign in British Columbia, particularly in major centres.

Here are some statistics about housing in B.C. from the Canada Mortgage and Housing Corporation’s 2024 Rental Market Report, issued in January, and the B.C. Real Estate Association’s August 2024 report.

Average residential home price in B.C.: $938,500

Average price in greater Vancouver (2024 year to date): $1,304,438

Average price in greater Victoria (2024 year to date): $979,103

Average price in the Okanagan (2024 year to date): $748,015

Average two-bedroom purpose-built rental in Vancouver: $2,181

Average two-bedroom purpose-built rental in Victoria: $1,839

Average two-bedroom purpose-built rental in Canada: $1,359

Rental vacancy rate in Vancouver: 0.9 per cent

How much more do new renters in Vancouver pay compared with renters who have occupied their home for at least a year: 27 per cent

This report by The Canadian Press was first published Oct. 17, 2024.

VANCOUVER – Voters along the south coast of British Columbia who have not cast their ballots yet will have to contend with heavy rain and high winds from an incoming atmospheric river weather system on election day.

Environment Canada says the weather system will bring prolonged heavy rain to Metro Vancouver, the Sunshine Coast, Fraser Valley, Howe Sound, Whistler and Vancouver Island starting Friday.

The agency says strong winds with gusts up to 80 kilometres an hour will also develop on Saturday — the day thousands are expected to go to the polls across B.C. — in parts of Vancouver Island and Metro Vancouver.

Wednesday was the last day for advance voting, which started on Oct. 10.

More than 180,000 voters cast their votes Wednesday — the most ever on an advance voting day in B.C., beating the record set just days earlier on Oct. 10 of more than 170,000 votes.

Environment Canada says voters in the area of the atmospheric river can expect around 70 millimetres of precipitation generally and up to 100 millimetres along the coastal mountains, while parts of Vancouver Island could see as much as 200 millimetres of rainfall for the weekend.

An atmospheric river system in November 2021 created severe flooding and landslides that at one point severed most rail links between Vancouver’s port and the rest of Canada while inundating communities in the Fraser Valley and B.C. Interior.

This report by The Canadian Press was first published Oct. 17, 2024.

British Columbia voters face no shortage of policies when it comes to tackling the province’s housing woes in the run-up to Saturday’s election, with a clear choice for the next government’s approach.

David Eby’s New Democrats say the housing market on its own will not deliver the homes people need, while B.C. Conservative Leader John Rustad saysgovernment is part of the problem and B.C. needs to “unleash” the potential of the private sector.

But Andy Yan, director of the City Program at Simon Fraser University, said the “punchline” was that neither would have a hand in regulating interest rates, the “giant X-factor” in housing affordability.

“The one policy that controls it all just happens to be a policy that the province, whoever wins, has absolutely no control over,” said Yan, who made a name for himself scrutinizing B.C.’s chronic affordability problems.

Some metrics have shown those problems easing, with Eby pointing to what he said was a seven per cent drop in rent prices in Vancouver.

But Statistics Canada says 2021 census data shows that 25.5 per cent of B.C. households were paying at least 30 per cent of their income on shelter costs, the worst for any province or territory.

Yan said government had “access to a few levers” aimed at boosting housing affordability, and Eby has been pulling several.

Yet a host of other factors are at play, rates in particular, Yan said.

“This is what makes housing so frustrating, right? It takes time. It takes decades through which solutions and policies play out,” Yan said.

Rustad, meanwhile, is running on a “deregulation” platform.

He has pledged to scrap key NDP housing initiatives, including the speculation and vacancy tax, restrictions on short-term rentals,and legislation aimed at boosting small-scale density in single-family neighbourhoods.

Green Leader Sonia Furstenau, meanwhile, says “commodification” of housing by large investors is a major factor driving up costs, and her party would prioritize people most vulnerable in the housing market.

Yan said it was too soon to fully assess the impact of the NDP government’s housing measures, but there was a risk housing challenges could get worse if certain safeguards were removed, such as policies that preserve existing rental homes.

If interest rates were to drop, spurring a surge of redevelopment, Yan said the new homes with higher rents could wipe the older, cheaper units off the map.

“There is this element of change and redevelopment that needs to occur as a city grows, yet the loss of that stock is part of really, the ongoing challenges,” Yan said.

Given the external forces buffeting the housing market, Yan said the question before voters this month was more about “narrative” than numbers.

“Who do you believe will deliver a better tomorrow?”

Yan said the market has limits, and governments play an important role in providing safeguards for those most vulnerable.

The market “won’t by itself deal with their housing needs,” Yan said, especially given what he described as B.C.’s “30-year deficit of non-market housing.”

IS HOUSING THE ‘GOVERNMENT’S JOB’?

Craig Jones, associate director of the Housing Research Collaborative at the University of British Columbia, echoed Yan, saying people are in “housing distress” and in urgent need of help in the form of social or non-market housing.

“The amount of housing that it’s going to take through straight-up supply to arrive at affordability, it’s more than the system can actually produce,” he said.

Among the three leaders, Yan said it was Furstenau who had focused on the role of the “financialization” of housing, or large investors using housing for profit.

“It really squeezes renters,” he said of the trend. “It captures those units that would ordinarily become affordable and moves (them) into an investment product.”

The Greens’ platform includes a pledge to advocate for federal legislation banning the sale of residential units toreal estate investment trusts, known as REITs.

The party has also proposed a two per cent tax on homes valued at $3 million or higher, while committing $1.5 billion to build 26,000 non-market units each year.

Eby’s NDP government has enacted a suite of policies aimed at speeding up the development and availability of middle-income housing and affordable rentals.

They include the Rental Protection Fund, which Jones described as a “cutting-edge” policy. The $500-million fund enables non-profit organizations to purchase and manage existing rental buildings with the goal of preserving their affordability.

Another flagship NDP housing initiative, dubbed BC Builds, uses $2 billion in government financingto offer low-interest loans for the development of rental buildings on low-cost, underutilized land. Under the program, operators must offer at least 20 per cent of their units at 20 per cent below the market value.

Ravi Kahlon, the NDP candidate for Delta North who serves as Eby’s housing minister,said BC Builds was designed to navigate “huge headwinds” in housing development, including high interest rates, global inflation and the cost of land.

Boosting supply is one piece of the larger housing puzzle, Kahlon said in an interview before the start of the election campaign.

“We also need governments to invest and … come up with innovative programs to be able to get more affordability than the market can deliver,” he said.

The NDP is also pledging to help more middle-class, first-time buyers into the housing market with a plan to finance 40 per cent of the price on certain projects, with the money repayable as a loan and carrying an interest rate of 1.5 per cent. The government’s contribution would have to be repaid upon resale, plus 40 per cent of any increase in value.

The Canadian Press reached out several times requesting a housing-focused interview with Rustad or another Conservative representative, but received no followup.

At a press conference officially launching the Conservatives’ campaign, Rustad said Eby “seems to think that (housing) is government’s job.”

A key element of the Conservatives’ housing plans is a provincial tax exemption dubbed the “Rustad Rebate.” It would start in 2026 with residents able to deduct up to $1,500 per month for rent and mortgage costs, increasing to $3,000 in 2029.

Rustad also wants Ottawa to reintroduce a 1970s federal program that offered tax incentives to spur multi-unit residential building construction.

“It’s critical to bring that back and get the rental stock that we need built,” Rustad said of the so-called MURB program during the recent televised leaders’ debate.

Rustad also wants to axe B.C.’s speculation and vacancy tax, which Eby says has added 20,000 units to the long-term rental market, and repeal rules restricting short-term rentals on platforms such as Airbnb and Vrbo to an operator’s principal residence or one secondary suite.

“(First) of all it was foreigners, and then it was speculators, and then it was vacant properties, and then it was Airbnbs, instead of pointing at the real problem, which is government, and government is getting in the way,” Rustad said during the televised leaders’ debate.

Rustad has also promised to speed up approvals for rezoning and development applications, and to step in if a city fails to meet the six-month target.

Eby’s approach to clearing zoning and regulatory hurdles includes legislation passed last fall that requires municipalities with more than 5,000 residents to allow small-scale, multi-unit housing on lots previously zoned for single family homes.

The New Democrats have also recently announced a series of free, standardized building designs and a plan to fast-track prefabricated homes in the province.

A statement from B.C.’s Housing Ministry said more than 90 per cent of 188 local governments had adopted the New Democrats’ small-scale, multi-unit housing legislation as of last month, while 21 had received extensions allowing more time.

Rustad has pledged to repeal that law too, describing Eby’s approach as “authoritarian.”

The Greens are meanwhile pledging to spend $650 million in annual infrastructure funding for communities, increase subsidies for elderly renters, and bring in vacancy control measures to prevent landlords from drastically raising rents for new tenants.

Yan likened the Oct. 19 election to a “referendum about the course that David Eby has set” for housing, with Rustad “offering a completely different direction.”

Regardless of which party and leader emerges victorious, Yan said B.C.’s next government will be working against the clock, as well as cost pressures.

Yan said failing to deliver affordable homes for everyone, particularly people living on B.C. streets and young, working families, came at a cost to the whole province.

“It diminishes us as a society, but then also as an economy.”

This report by The Canadian Press was first published Oct. 17, 2024.