(Bloomberg) — Britain’s economy will retain deep scars long after the pandemic has passed, slowing growth and adding to the strain on the public finances, a major report ahead of the government’s budget concluded.

The findings from the Institute for Fiscal Studies illustrate the pressures facing Chancellor of the Exchequer Rishi Sunak, with rising prices and interest rates likely to add 15 billion pounds ($20 billion) to the Treasury’s debt payments this year and beyond.

The projection sketch out the tensions from inflation to increased demands on the public purse that Sunak will have to juggle in his statement on Oct. 27. It also leaves Prime Minister Boris Johnson’s government little cash to splurge on big projects like improvements to road and railways popular with voters.

With pressure to increase funds on health care, “there will be little or no scope to increase spending on things like like local government, the justice system and further education after a decade of sharp cuts,” said IFS Director Paul Johnson.

Economists at Citi, which helped produce the report, said output is on course to remain below its pre-pandemic level at the end of this year, and as much as 3% of output has been lost permanently due to the the crisis and Britain exit from the European Union.

The chancellor wants to repair the unprecedented fiscal damage inflicted by Covid-19, when the government extended aid to people and companies prevented from working during lockdowns to control the virus.

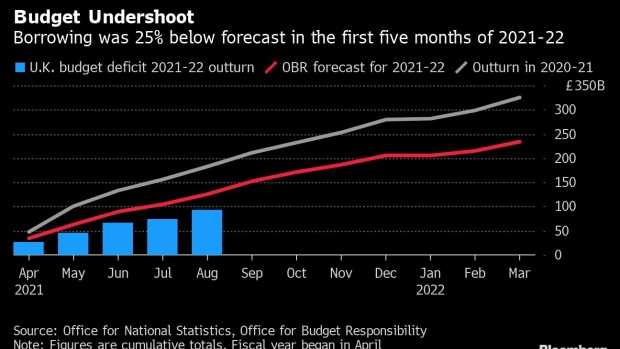

While borrowing this year is set to significantly undershoot officials forecast due to a stronger-than-expected recovery, slower growth is likely to squeeze finances in the future. The IFS predicted that the deficit in 2025-26 will be only around 20 billion pounds lower than the Office for Budget Responsibility predicted in March.

The public finances are more sensitive to inflation than they were in the past because a quarter of government borrowing is tied to the retail price index, which is being driven higher by rising energy cost and shortages of goods and workers. Borrowing is also more responsive to changes in short-term interest rates because of the huge amount of debt now held by the Bank of England.

On a brighter note, Citi expects the upsurge in inflation to prove temporary, with CPI price growth reaching around 4.5% to 5% in the spring of next year before dropping back below the 2% target before the end of 2022. It sees the benchmark interest rate leveling off at around 0.5% after increases in both February and May next year.

The IFS acknowledged that “huge uncertainty” surrounded the outlook. It calculated that the deficit could be around 19 billion pounds lower in 2023-24 if the economy follows the path projected by the Bank of England, which sees GDP returning to pre-pandemic levels early next year.

On the other hand, a pessimistic scenario could force the government to increase taxes that are already at their highest levels in peacetime after Johnson’s government last month announced plans to hike payroll levies to pay for health care. It would also make it hard for Sunak to deliver on his ambition of balancing day-to-day spending and revenue by the middle of the decade.

©2021 Bloomberg L.P.