The global oil market is in flux once again. The bulls are fighting it out with the bears as COVID lockdowns come into force around the world. Oil prices may have hit 10-month highs on the back of extended production cuts from OPEC+ but black clouds have re-emerged on the horizon as the majority of OECD markets appear to be struggling with a new strain of COVID. The new strain was first identified in the UK but has now been reported in China, Japan, and other major Asian markets. Optimism about short-term oil prices should be subdued as demand for fuels will undoubtedly take a hit as lockdowns continue. A potential new oil glut could be in the making for H1 2021 if exporters fail to keep their promises.

Still, there will be a post-COVID era at some point, hopefully shortly after summer. Optimism remains tempered, but global vaccination programs are in place, which could lead to a reopening in the near future. The real market threats in the years to come, however, are currently being ignored. After several years of being bombarded by peak oil demand or oil glut scenarios, the market is without any doubt heading towards a major supply crisis. The COVID-era has not only removed short-term demand and increased interest in a global energy transition, it has also brought down global upstream investments. Analysts have already indicated a possible peak oil investment scenario, but that has been countered by many claiming that renewables will make up for losses. The reality, however, is very worrying. Demand for crude oil, natural gas, and petroleum products is going to hit a plateau in the coming decades, but it will still likely reach a level of more than 108-110 million bpd for a long period of time. Demand is likely to grow by at least 10 million bpd from current levels. So where are these additional volumes going to come from? With upstream investment faltering and majors turning their back on oil, it remains unclear how this demand will be met.

Related: Big Oil Is An Unsung Hero In The Fight Against COVID

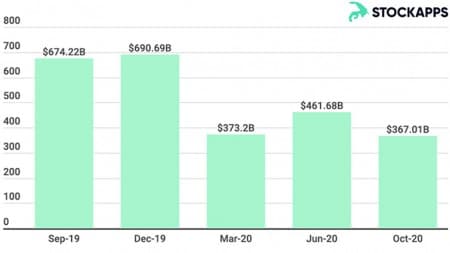

During COVID, international oil companies have seen a steep decline in their revenues, market value, and interest from institutional investors. The ongoing financial plunge has had an enormous effect on their total market capitalization, which plunged to unforeseen levels. In October 2020 reports showed that the combined market cap of the top-5 oil companies in the U.S. fell by 45% to $367 billion, in comparison to $690 billion in December 2019 or $674 billion in October 2019. It wasn’t only COVID that was responsible for this drop, but also global macro-economic drivers, such as the U.S.-China trade war and continuing oil overproduction. In the last year, instability in the market has increased due to lower revenues, increased market cooperation, and a tsunami of bankruptcies, divestments, and consolidation. A significant indicator of just how much the industry was suffering was the removal of ExxonMobil, once the world’s largest publicly traded company, from the Dow Jones Industrial Average in August 2020. Exxon suffered a huge market cap drop in 2020, falling from $300 billion in September 2019 to $144 billion in October 2020.

European oil and gas companies also suffered in 2020. Almost all 25 NA-European oil and gas companies have seen a market capitalization crash in 2020.

European supermajors Royal Dutch Shell and BP, which are in the midst of diversifying their businesses, declined in value by 33.5% and 34.5%, respectively. At the end of 2020, overall energy indexes were still around 20% lower than at the start of 2020.

Major investment institutions are currently turning their backs on hydrocarbon investments. A growing political emphasis on renewables, low-carbon or even Net-Zero production, and other energy transition policies are massively hurting oil and gas investment. The IMF, WB, EBRD, EIB, and others have also stated that they are ending hydrocarbon project financing. The well-recorded oil demand destruction during 2020 has pushed oil supply risks out of the mind of analysts is seems. Most E&P companies have curtailed their spending on upstream operations dramatically. These lower 2020 investment levels, combined with several low investment years before, are now a serious threat to the future of the oil market. Market volatility is expected to increase in the coming years, mainly due to the lower investment levels reducing supply.

Related: U.S. Oil Drillers To Face More Pain Despite Higher Prices

2021 could be a watershed year for oil markets, in which falling investments and bankruptcies will create a supply crunch the likes of which we have never seen before. With an ever-growing list of delayed upstream projects and FIDs, the threat is growing. In a report by the International Energy Forum (IEF) and consultancy BCG in December 2020, warnings were given that lower CAPEX levels and low investment appetite will be a real threat to markets. OPEC, IEA, and others, have already made it clear that cumulative hydrocarbon related investments are dwindling. As OPEC has indicated before, investment volumes of around $12.6 trillion are needed to keep the oil supply for the coming decades at the current level. Norwegian oil consultancy Rystad Energy said that even though demand has declined in 2020, 2019 levels could return before 2024/25, necessitating future upstream spending of an average of $380 billion p.a. over the long-term. The need for large scale new investments is clear, as the upstream sector has already been fighting an uphill battle to get access to the necessary investment volumes in recent years. Larger investments are necessary to avoid a future of higher prices and increased market volatility. Inadequate investments will set off another wave of unwanted boom-and-bust pricing. With oil majors indicating that CAPEX reductions will be in place throughout 2021, and some even seeing 2022 as a difficult year, production is undoubtedly being threatened.

Technology alone cannot be the savior. IEF research indicated that every dollar of CAPEX that is cut today will have twice as powerful an effect in terms of reducing activity as the cuts made following the 2014 fall in prices had. As demand for oil and gas is expected to increase after COVID, low CAPEX supply will become a major constraint. At the moment, no real new immense oil and gas resource is available to counter demand growth without trillions of investment dollars being poured in.

A peak oil investment crisis is in the making. The current financials of most IOCs and leading NOCs are not accounting for peak investment requirements. As the IEF report clearly states, industry investment will have to rise over the next three years by at least 25% yearly from 2020 levels to stave off a crisis. Peak oil prices also could be a reality if the market doesn’t react.

By Cyril Widdershoven for Oilprice.com

More Top Reads From Oilprice.com:

<!–

Trending Discussions

–>

Cyril Widdershoven

Dr. Cyril Widdershoven is a long-time observer of the global energy market. Presently, he holds several advisory positions with international think tanks in the Middle…

![]()

- 80% of investors end up losing money…

- Learn how to navigate energy markets. Learn how energy insiders think.

- Receive our cutting-edge 3-part investor education series for FREE

- PLUS, get our Weekly Intelligence Report to stay one step ahead of the markets…