Many homeowners are unprepared for flooding because they lack critical information thanks to murky real estate rules, incomplete floodplain maps and an insurance industry pulling back from high-risk areas, a Marketplace investigation has found.

Marketplace also found homeowners who lost their flood protection because of multiple claims or specifically because of the growing risk of climate change. The Insurance Bureau of Canada (IBC) warns it’s a situation more Canadians could find themselves in.

Watch the full Marketplace investigation tonight at 8 p.m. (8:30 NT) on CBC-TV and CBC Gem

The IBC told Marketplace it estimates that anywhere from six to 10 per cent of Canadian homes are currently uninsurable due to flooding and that estimate could go up as more insurance companies update their risk assessments to account for the rising threat of climate change.

“As the risk from climate change increases, yes, more Canadians could become uninsurable,” said Craig Stewart, vice-president, federal affairs with the IBC.

According to a 2019 federal government report, Canada’s climate is warming at double the rate of the rest of the world, and the IBC estimates that currently 1 in 10 Canadian homes is at high risk of flooding and some face possible repeated flooding over the next 20 years.

But would prospective homeowners be warned about that risk? Going undercover, posing as new homebuyers in Ontario, a Marketplace team found there’s no Canada-wide requirement for agents or sellers to warn potential buyers that they’re moving into a flood-prone area. Marketplace was told on two occasions that homes were not in floodplains when public data showed otherwise. In another test, a producer posing as a prospective home seller also found agents didn’t always advise her to disclose past flood damage.

The recent flooding in British Columbia has made the issue of flood insurance coverage top of mind for many homeowners, as some residents there, unable to find coverage, turn to provincial disaster assistance, and others assess what coverage they have as the cleanup begins.

‘They’re trying to protect their money’

But in some cases, even being prepared isn’t enough. Derrick Terakita knew his home in Richmond Hill, north of Toronto, was in a floodplain and thought he had adequate coverage, until he got his insurance renewal this year. In May his insurance provider informed him it was taking away his overland water coverage. The reason: the increasing severity of weather due to climate change.

“I was a little bit ticked off, but then it’s an insurance company, they’re trying to protect their money,” Terakita told Marketplace.

WATCH | Insurance nightmares: Many Canadians not protected from flooding disasters:

Murky real estate rules and insurance eligibility leaving Canadians with big bills after flooding

13 hours ago

Flooding is the most costly and common natural disaster in Canada, but risk-averse insurance companies and the lack of a nationwide requirement for real estate agents to disclose flood risk are leaving Canadians vulnerable. 2:16

Overland flood insurance typically protects homeowners from flooding from a body of water overflowing onto dry land. According to the IBC, protection from flooding due to burst pipes or appliances is typically included in most home policies. Sewer backup protection is also commonly available as an add-on. But overland flood insurance only became an option in Canada in 2015, following massive flooding in southern Alberta in 2013 that, at the time, was ranked as the costliest natural disaster in Canadian history.

Marketplace connected Terakita with an insurance expert to better understand his situation. He then contacted his insurance broker to see if his provider could reinstate his coverage if he took steps to protect his home. The answer was no.

‘Insurance will become a luxury for the rich’

“We can’t really offer the coverage because again, it’s no longer applicable to your territory,” the broker told Terakita over the phone as Marketplace cameras rolled. “Even if there was some sort of mitigation put into place, it’s still not going to be applicable.”

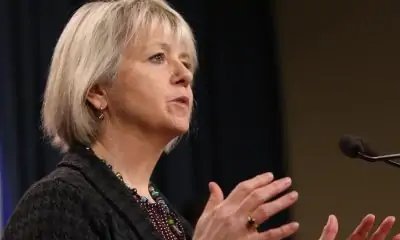

Insurance expert Jason Thistlethwaite says that if we don’t manage climate risk better, insurance may eventually become a luxury and unaffordable for most people. (Steven D’Souza/CBC)

Marketplace showed Terakita’s experience with his insurance company to Jason Thistlethwaite, an associate professor in the School of Environment, Enterprise and Development at the University of Waterloo in Ontario.

“It’s unfortunate but insurance companies are businesses and they’re looking at their bottom line and they are going to make a judgment on their risk appetite,” said Thistlethwaite, who noted that flooding is the most costly and common hazard in Canada.

Thistlethwaite worries that many more Canadians will soon find themselves in Terakita’s shoes.

“Insurability — or markets where insurance is available and affordable — is eroding in Canada,” Thistlethwaite said. “Unless we make more effort to manage climate risk, insurance will become a luxury for the rich and unaffordable for most.”

Insurance industry responds

Stewart from the IBC agrees that insurance companies need to do a better job of giving incentives to customers like Terakita who want to be proactive in protecting their home.

Craig Stewart, seen here evaluating the aftermath of a tornado, is with the Insurance Bureau of Canada. He says the industry can’t shoulder all the risk for insuring high-risk homes and that a government-backed, high-risk insurance pool needs to be created. (Submitted by Craig Stewart)

He says in a competitive marketplace, customers like Terakita can shop around for coverage. Though he acknowledges that finding another option isn’t guaranteed and the industry has its limitations when it comes to overland insurance protection.

“The industry’s new to [overland flood protection] in Canada, but we’re only going to be able to provide a certain amount of protection. We are going to need to collaborate with the government, especially for those who will continue to reside in the highest-risk areas in the country.”

The solution the IBC proposes is a national high-risk residential flood insurance program, which would provide insurance to residents in the most flood-prone areas, funded by the federal government.

It’s one idea the Liberal government is studying as part of it’s National Task Force on Flood Insurance and Relocation, which was formed last year. The group is also studying options to relocate people who live in areas with repeated flooding.

Stewart, a member of the task force through the IBC, says they’ll present recommendations to Minister of Emergency Preparedness Bill Blair in the spring, but programs aren’t likely to roll out until 2023 or 2024.

“We need all hands on deck, and insurers will absolutely play their part in addressing the problem, but we can’t do it alone,” Stewart said.

Debris litters a road in the Sumas Prairie flood zone in Abbotsford, B.C., on Nov. 22. (Ben Nelms/CBC)

Asked by CBC News about the insurance situation during a news conference in Ottawa last week, Blair said the recent flooding in British Columbia underscores the importance of the task force’s work.

“It does, I think, add an element of urgency to our work with the insurance industry and the development of a National Flood Insurance Plan,” Blair said.

Government-backed flood insurance does come with its share of problems. In the U.S., the National Flood Insurance Program has a $20 billion US shortfall and is often criticized for using outdated information and incentivizing rebuilding in problem areas.

Homeowners unaware of the risk

Despite the stark warnings about the impact of climate change and the threat of flooding, the issue isn’t always top of mind. A 2020 survey by Partners for Action, a climate resiliency network based at the University of Waterloo, found only six per cent of Canadians living in designated flood-risk areas knew they lived in such an area, and only a quarter said their insurance company had discussed flood coverage options with them.

In Toronto, Woodee Aboy recently moved into his home but didn’t know the neighbourhood is a floodplain designated by the Toronto and Region Conservation Authority until Marketplace knocked on his door. He was also unsure that his home insurance policy covered him against all types of flooding.

After Marketplace connected him with an insurance expert, he contacted his provider and found he was in fact fully covered for a range of flood scenarios, including overland.

“Gaining that confidence, gaining that peace of mind has been a very fulfilling experience to tell you honestly,” Aboy told Marketplace.

No Canada-wide requirement for disclosing future flood risk

Aboy and other homeowners Marketplace spoke with say they were not informed when they purchased their home that there was a risk of potential flooding.

Toronto resident Woodee Aboy wasn’t aware his home was located in a flood-prone area until contacted by Marketplace. He later confirmed that his home insurance policy does protect him for a range of flood scenarios. (Steven D’Souza/CBC)

Part of the challenge, Marketplace found, is that disclosure rules around future flood risk are vague and vary across the country. It’s not information real estate agents may know how to find, or the flood mapping in the area may be out of date or incomplete.

In an undercover test, Marketplace posed as buyers looking at Greater Toronto Area properties situated in floodplains — areas designated in publicly available maps by the Toronto and Region Conservation Authority. The result: agents selling two of four properties denied the homes were at risk of potential flooding.

Marketplace: “I noticed there’s a waterway nearby. I’m just wondering, are there flooding issues, or is flooding a concern for that area?”

Agent: “For that property? No, it’s too far away.”

Marketplace: “So it’s not on a floodplain or anything?”

Agent: “No no no.”

Marketplace: “So we shouldn’t be worried about that?”

Agent: “No, no.”

Later, posing as a seller looking to unload a home that had had previous flood damage, a producer called agents in five cities: Vancouver, Calgary, Winnipeg, Toronto and Montreal. Marketplace found nine out of 10 agents were clear that past flooding should be disclosed. But one agent said that if the cause of the flood had been repaired, then there was no need for disclosure.

WATCH | Here’s how to protect your home from flooding:

Insurance expert Cheryl Evans explains how to flood-proof your home

18 hours ago

Cheryl Evans, a director at the University of Waterloo’s Intact Centre on Climate Adaptation, explains what steps homeowners can take to try and flood-proof their homes 2:00

The agent’s advice, however, seems to line up with information Marketplace received from the regulator in his home province, the Real Estate Council of Alberta (RECA). “If the defect is properly repaired, there is no longer a defect, and disclosure is not required,” RECA said.

The rules around disclosure in some provinces also leave some room for interpretation. For example, the Real Estate Council of Ontario (RECO), the regulator in that province, says that past flooding is “often” considered a latent defect — defined as “a physical defect that is not discoverable through a visual inspection.” RECO says sellers are only obligated to disclose these when the issue is “dangerous” or could make the property “uninhabitable,” though it notes the issue often ends up in the courts.

“It is to your advantage to be as truthful as you can, for your own protection, when you’re making these declarations,” one agent advised.

Marketplace producers also asked some of those agents whether disclosing future flood risk or floodplains was recommended, but answers were less clear. Some recommended disclosing, some said it was speculative and “buyer beware.”

Toronto real estate agent Chris Chopik wants to see more transparency in the industry around climate risk. (CBC)

The challenge, experts say, is that there is no Canada-wide requirement to disclose future flood risk.

“There’s a requirement to disclose known risks, so the question comes, what is known and what’s knowable?” said Toronto real estate agent Chris Chopik.

Chopik has been pushing for years for more transparency around climate risk in real estate. He’d like to see something akin to a walk score, but for climate: an easy-to-digest number assessing a home’s overall risk from the impacts of climate change.

The federal government has committed $63 million to improving floodplain mapping within three years, but experts say there’s a long way to go.

“I would describe floodplain mapping as saying, right now we’re at the Windows ’95 version of flood mapping,” said Stewart with the IBC. “What we need to do in pretty short order is get up to Windows 10. We are behind other countries.”

Prince Edward Island recently launched a new coastal hazards platform, while a researcher at Western University in Ontario recently released what the university calls the first Canada-wide maps showing how floodplains may be affected by various climate change scenarios over the next 80 years.

Chopik says that while there are fears that more information about potential flood risk could devalue a home, ultimately more information will level the playing field and make potential buyers aware of climate-related risks.

“If we’re going to make this a fair marketplace where we have caveat emptor — buyer beware — we really need a place where everyone can look at the risk soberly and then make decisions.”

Have questions about this story? We’re answering as many as we can in the comments.

VANCOUVER – The federal government is urging both sides in the British Columbia port dispute to return to the table after Saturday’s collapse of mediated talks to end the lockout at container terminals that has entered its second week.

A statement issued by the office of federal Labour Minister Steven MacKinnon on Monday said both the port employers and the union representing more than 700 longshore supervisors “must understand the urgency of the situation.”

The statement also urged both sides to “do the work necessary to reach an agreement.”

“Canadians are counting on them,” the statement from MacKinnon’s office said.

The lockout at B.C. container terminals including those in Vancouver — Canada’s largest port — began last week after the BC Maritime Employers Association said members of International Longshore and Warehouse Union Ship and Dock Foremen Local 514 began strike activity in response to a “final offer” from employers.

The union said the plan was only for an overtime ban and a refusal to implement automation technology, calling the provincewide lockout a reckless overreaction.

On Saturday, the two sides began what was scheduled to be up to three days of mediated talks, after MacKinnon spoke to both sides and said on social media that there was a “concerning lack of urgency” to resolve the dispute.

But the union said the talks lasted “less than one hour” Saturday without resolution, accusing the employers of cutting them off.

The employers denied ending the talks, saying the mediator concluded the discussions after “there was no progress made” in talks conducted separately with the association and the union.

“The BCMEA went into the meeting with open minds and seeking to achieve a negotiated settlement at the bargaining table,” a statement from the employers said.

“In a sincere effort to bring these drawn-out negotiations to a close, the BCMEA provided a competitive offer to ILWU Local 514 … the offer did not require any concessions from the union and, if accepted, would have ended this dispute.”

The employers said the offer includes a 19.2 per cent wage increase over a four-year term along with an average lump sum payment of $21,000 per qualified worker, but the union said it did not address staffing levels given the advent of port automation technology in terminals such as DP World’s Centerm in Vancouver.

After talks broke off, the union accused the employers of “showing flagrant disregard for the seriousness of their lockout.”

Local 514 president Frank Morena said in a statement on Saturday that the union is “calling on the actual individual employers who run the terminals to order their bargaining agent — the BCMEA — to get back to the table.”

“We believe the individual employers who actually run the terminals need to step up and order their bargaining agent to get back to the table and start negotiations and stop the confrontation,” Morena said.

No further talks are currently scheduled.

According to the Canada Labour Code, the labour minister or either party in a dispute can request a mediator to “make recommendations for settlement of the dispute or the difference.”

In addition, Section 107 of the Code gives the minister additional powers to take action that “seem likely to maintain or secure industrial peace and to promote conditions favourable to the settlement of industrial disputes,” and could direct the Canada Industrial Relations Board “to do such things as the Minister deems necessary.”

Liam McHugh-Russell, assistant professor at Schulich School of Law at Dalhousie University, said Section 107 “is very vague about what it allows a minister to do.”

“All it says is that the minister can refer a problem and a solution to the Labour Board. They can ask the Labour Board to try and solve the problem,” he said.

“Maybe the minister will try to do that. It remains to be seen.”

The other option if mediated talks fail — beyond the parties reaching a solution on their own — would be a legislated return to work, which would be an exception to the normal way labour negotiations operate under the Labour Code.

Parliament is not scheduled to sit this week and will return on Nov. 18.

The labour strife at B.C. ports is happening at the same time another dispute is disrupting Montreal, Canada’s second-largest port.

The employers there locked out almost 1,200 workers on Sunday night after a “final” offer was not accepted, greatly reducing operations.

This report by The Canadian Press was first published Nov. 11, 2024.

LONGUEUIL, Que. – A man charged with first-degree murder in the death of his partner in a Montreal suburb was out on bail for uttering threats against her when she was killed.

Shilei Du was charged today with the killing of 29-year-old Guangmei Ye in Candiac, Que., about 15 kilometres southwest of Montreal.

Sgt. Frédéric Deshaies of the Quebec provincial police says their investigators were called by local police to a home in Candiac at about noon on Sunday.

The charges filed at the Longueuil courthouse against 36-year-old Du allege the killing took place on or around Nov. 7.

According to court files, Du had previously appeared at the same courthouse for allegedly uttering threats to cause death or bodily harm against Ye on Sept. 7.

Du pleaded not guilty the following day and was released on bail one day later. He had been present in court on the uttering threats charges on Nov. 6.

Du, whose current address is listed in Montreal, was arrested on Sunday at the home where Ye was killed.

The case is scheduled to return to court on Nov. 19.

This report by The Canadian Press was first published Nov. 11, 2024.

MADISON, Wis. (AP) — The Wisconsin Supreme Court will hear oral arguments Monday on whether a law that legislators adopted more than a decade before the Civil War bans abortion and can still be enforced.

Abortion rights advocates stand an excellent chance of prevailing, given that liberal justices control the court and one of them remarked on the campaign trail that she supports abortion rights. Monday’s arguments are little more than a formality ahead of a ruling, which is expected to take weeks.

Wisconsin lawmakers passed the state’s first prohibition on abortion in 1849. That law stated that anyone who killed a fetus unless the act was to save the mother’s life was guilty of manslaughter. Legislators passed statutes about a decade later that prohibited a woman from attempting to obtain her own miscarriage. In the 1950s, lawmakers revised the law’s language to make killing an unborn child or killing the mother with the intent of destroying her unborn child a felony. The revisions allowed a doctor in consultation with two other physicians to perform an abortion to save the mother’s life.

The U.S. Supreme Court’s landmark 1973 Roe v. Wade ruling legalizing abortion nationwide nullified the Wisconsin ban, but legislators never repealed it. When the Supreme Court overturned Roe two years ago, conservatives argued that the Wisconsin ban was enforceable again.

Democratic Attorney General Josh Kaul filed a lawsuit challenging the law in 2022. He argued that a 1985 Wisconsin law that allows abortions before a fetus can survive outside the womb supersedes the ban. Some babies can survive with medical help after 21 weeks of gestation.

Sheboygan County District Attorney Joel Urmanski, a Republican, argues the 1849 ban should be enforceable. He contends that it was never repealed and that it can co-exist with the 1985 law because that law didn’t legalize abortion at any point. Other modern-day abortion restrictions also don’t legalize the practice, he argues.

Dane County Circuit Judge Diane Schlipper ruled last year that the old ban outlaws feticide — which she defined as the killing of a fetus without the mother’s consent — but not consensual abortions. The ruling emboldened Planned Parenthood to resume offering abortions in Wisconsin after halting procedures after Roe was overturned.

Urmanski asked the state Supreme Court in February to overturn Schlipper’s ruling without waiting for lower appellate courts to rule first. The court agreed to take the case in July.

Planned Parenthood of Wisconsin filed a separate lawsuit in February asking the state Supreme Court to rule directly on whether a constitutional right to abortion exists in the state. The court agreed in July to take that case as well. The justices have yet to schedule oral arguments.

Persuading the court’s liberal majority to uphold the ban appears next to impossible. Liberal Justice Janet Protasiewicz stated openly during her campaign that she supports abortion rights, a major departure for a judicial candidate. Usually, such candidates refrain from speaking about their personal views to avoid the appearance of bias.

The court’s three conservative justices have accused the liberals of playing politics with abortion.