In New Jersey, lenders to the American Dream mall are heading to court, demanding a $389 million payment on their defaulted debt.

Some 25 miles north, just over the state line with New York, investors are looking to foreclose on one of the country’s largest malls. And across the country in Los Angeles county, the owners of a Westfield mall expect it to be foreclosed if they can’t sell the property.

The collapse of the US mall industry, long hyped by billionaire investor Carl Icahn and other doomsayers, may indeed finally be near. The industry has been shaky for years, of course, but now that interest rates are soaring from record-low levels, lenders are beginning to move aggressively against property owners.

“There’s a cost benefit analysis being done with respect to taking an action now — that they’re preserving more value by acting now rather delaying action,” said Cynthia Nelson, a senior managing director who leads real estate restructuring at FTI Consulting.

All of this marks the start of what’s expected to be a wave of defaults in the wider commercial real estate industry as that jump in borrowing costs causes property values to fall. This time around offices are also in the spotlight as the work-from-home phenomenon leads companies to cut the space they lease.

Short sellers have also begun to circle once again. It’s not Icahn out in front on the bet this time but Bruce Richards, the chief executive officer at Marathon Asset Management.

The Short Bet on Offices Is Starting to Look Like Malls

CMBX indexes are used to short real estate debt

Source: Bloomberg

Icahn bet against malls using derivatives linked to a series commercial real estate indexes known as CMBX. It’s a similar instrument that hedge fund trader Michael Burry, one of the main characters in the movie The Big Short, used to short the US housing market more than a decade ago.

But Richards says the mall CMBX trade’s too expensive now. Instead, he’s focused on a more recent version of the CMBX index, Series 13, that’s more heavily tied to office towers. In a recession, the spreads could blow out, he says.

“The better short may be more recent vintage securities with heavy office exposure,” he said.

Richards’ bet comes as borrowers including Brookfield have already handed back the keys to some office properties or are opting to default.

“The mall business can provide a preview to the challenges owners and lenders of office buildings may face in the coming years,” said Vince Tibone, a retail analyst at Green Street.

By the Numbers

A Comeback Story Starts to Fizzle

Chinese junk bonds lose steam after 50% rally

Source: Bloomberg Asia Ex-Japan USD Credit China High Yield index

China‘s aggressive steps last year to prop up its battered property sector slowed a wave of defaults by the country’s developers and kicked off a rebound in the value of their bonds. A Bloomberg index of US dollar-denominated bonds issued by junk-rated Chinese companies — a benchmark dominated by distressed developers — gained about 50% from its lows in November through the end of January. The rally has lost steam this month, however, as a slump in housing sales persists, keeping cash tight for the builders. Despite Beijing’s sweeping efforts to inject liquidity into the sector, a number of developers have kept their bondholders waiting until the final hours before grace periods run out on their interest payments, Alice Huang, Jackie Cai and Lorretta Chen report. One builder, Central China Real Estate, remitted funds this week for a $9.75 million bond payment that was originally due Jan. 14.

High Alert

- Lenders to Cinven-owned Italian life insurer Eurovita have started to write down €300 million of loans after the domestic regulator suspended management and halted redemptions, pushing the private-equity owner into the spotlight. The saga highlights concerns among regulators and banks about private equity’s ownership model when it comes to companies offering financial products to retail customers.

- Lapo Elkann, one of the heirs of the billionaire Agnelli family, reached a deal to restructure the debt of his own fashion company Italia Independent Group. Elkann will inject €13 million, while creditors will write off as much as 90% of their loans.

- US cloud company Avaya filed for bankruptcy in Texas after reaching an agreement with creditors to cut its $3.4 billion debt by more than 75%. Investors led by Apollo and Brigade committed to provide a new loan. The company previously faced the ire of lenders over its lack of disclosures.

- Indonesia’s biggest listed construction company, Waskita Karya Persero, is planning to delay a $151 million bond payment due next week to June. The crisis in the Indonesian building sector has drawn comparison with China and Korea.

- Retailer Americanas appointed Leonardo Coelho Pereira as its third chief executive officer in six weeks as it tries to navigate through the bankruptcy protection process in Brazil.

Click here for the Credit Edge podcast on structured credit and healthcare distress

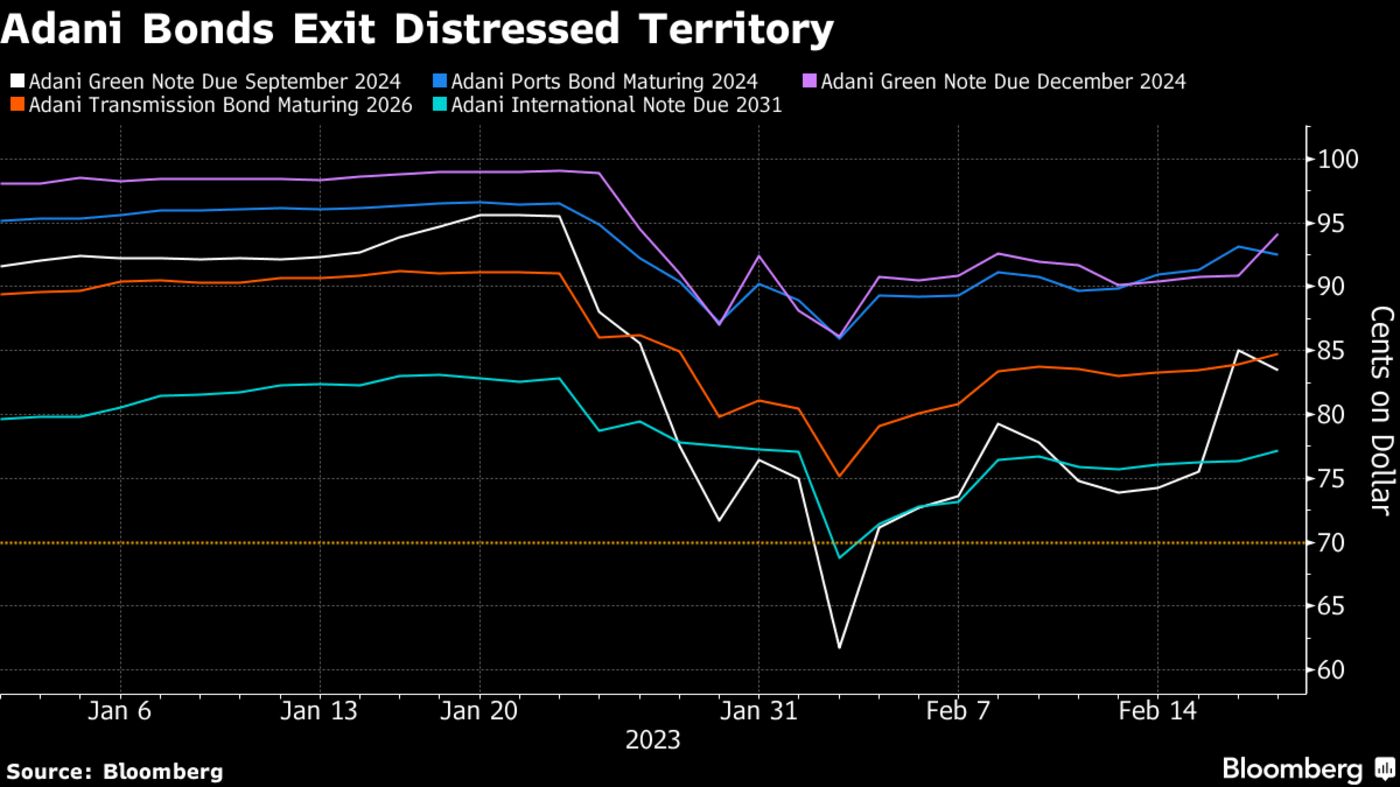

Latest on… Adani

Adani Group moved to reassure investors’ after a damaging short-seller report accused it of fraud.

While a catchy tune in support of founder Gautam Adani got more than 300,000 views on YouTube, executives had to talk money to convince bondholders the group is not spiraling into a full-blown crisis, Giulia Morpurgo and Finbarr Flynn report.

Their strategy seems to be working. Most of the group’s dollar bonds have climbed out of distressed territory after the company held two conference calls on Thursday to lay out plans for the repayment of the nearest debt maturities.

Money managers were worried that access to public funding markets would get more complicated and incredibly expensive for the group given the extra scrutiny Adani’s empire is now under.

However, Adani’s initial plans suggest that the group doesn’t have to tap capital markets to meet its debt maturities; instead, it can take advantage of private markets, issuing long-dated bonds to an undisclosed group of selected investors.

The ability to access new borrowing is key for a group that embraced the era of cheap debt by loading up with it. In recent years, Adani has tapped international bond buyers for more than $8 billion, while also turning to global banks for at least as much in foreign-currency loans.

Seeking private funding would not be a first for Adani; the Indian conglomerate tapped the US private placement markets on multiple earlier occasions before the short-seller report by Hindenburg Research. Entities related to Gautam Adani have counted the likes of Apollo among its private funding backers. The company has also traditionally had strong support from Gulf-based investors.

Notes From the Brink

Credit Suisse used to be big in trading the debt of troubled companies — but now it has problems of its own to worry about.

The Swiss lender is set to get out of distressed debt trading with the sale of a $250 million portfolio. The disparate assets include a loan to autoparts maker Standard Profil Automotive and claims linked to the insolvency of travel agent Thomas Cook, Giulia Morpurgo and Lucca De Paoli write. The team led by Thomas Mathieson, head of special situations and loan trading in London, could also move over to any buyer.

Exiting the distressed debt business allows the lender to allocate capital elsewhere instead of the relatively higher amounts needed to back troubled loans. It’s a sign of the radical changes needed to fix the lender’s balance sheet and comes shortly after the bank sold its structured product business to Apollo.

Read more: Credit Suisse Needs a Cockroach Exterminator

Credit Suisse has been bruised by years of scandals, including losses from the collapse of Archegos and Greensill. At the end of last year the bank hemorrhaged assets and recorded a fifth quarterly loss. The Swiss lender is in the early stages of a restructuring that includes cutting 9,000 jobs.

— With assistance by Giulia Morpurgo, Lucca De Paoli, Finbarr Flynn, Jeanette Rodrigues, Alice Huang, Jackie Cai, Lorretta Chen, Laura Benitez and Marion Halftermeyer