Hello. Today we look at the threat of stagflation, this week’s European Central Bank meeting and how some Americans still aren’t receiving their benefits.

A Concerning Combination

The world economy risks turning stagflationary.

While policy makers once hoped we’d now be seeing decent growth and slowing inflation, obstacles to that outlook are emerging by the day.

The mounting concern now is of a toxic mixture of weak demand and accelerating prices.

Risk one is the delta variant, which, as Enda Curran details, is undermining efforts to rev up factories, offices and schools.

There goes the demand side, but the new form of the coronavirus is also hurting supply chains, limiting the worldwide provision of key products. That shock, which is building just as Christmas nears, threatens to force up inflation too.

Meanwhile, natural gas prices are witnessing a historic surge, catapulting the cost of the fuel to seasonal highs in most major markets just as winter approaches in the northern hemisphere.

Soarings bills could crimp households’ spending and erode their wages through inflation, a stagflationary combination especially if families and businesses react to rising utility charges by pushing up pay and prices.

See more on gas prices here and the brewing aluminum surge here

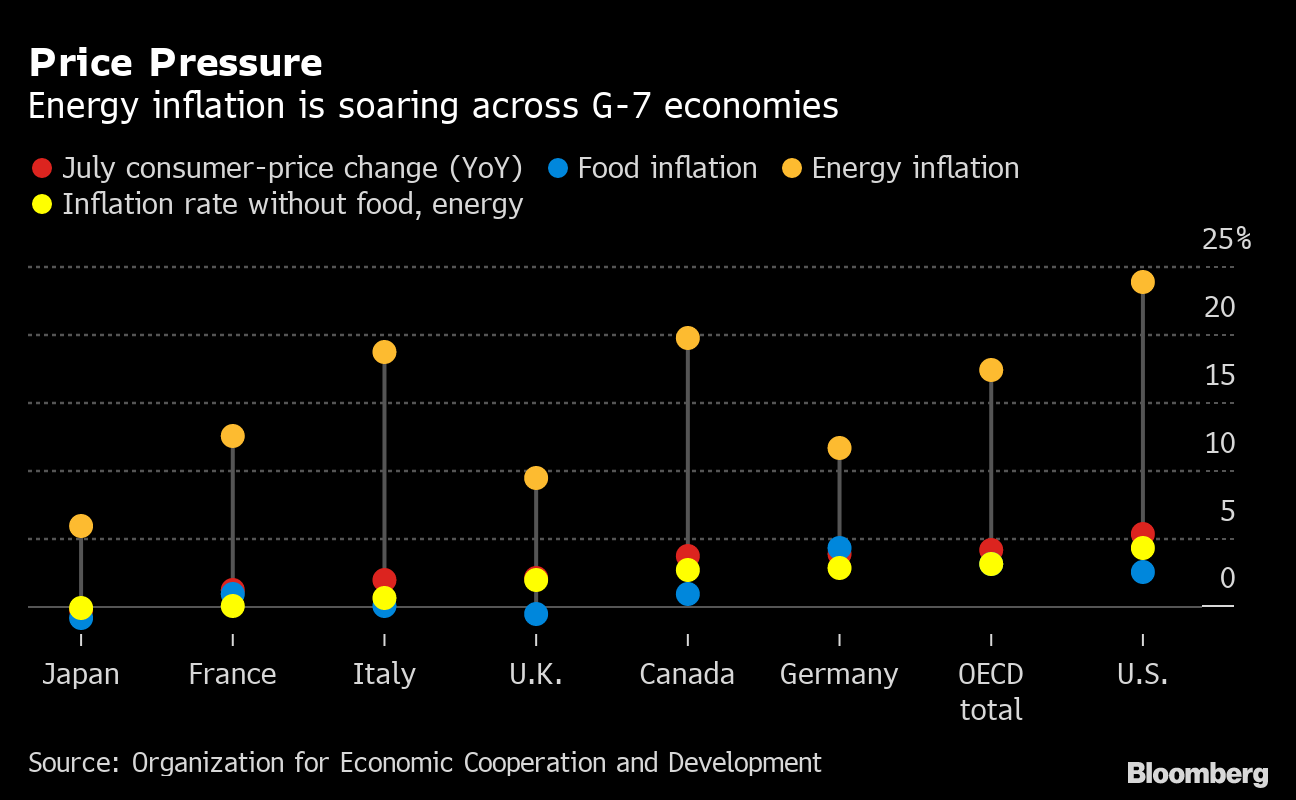

Price Pressure

Energy inflation is soaring across G-7 economies

Source: Organization for Economic Cooperation and Development

.chart-js display: none;

For policy makers, this environment is a conundrum. To date, most have focused on spurring their economies with stimulus, arguing the inflation surge would prove temporary. Now that view will be tested.

Catherine Mann, recently recruited by the Bank of England from Citigroup, has some words of comfort. She used a speech to Australian businesses today to argue inflation isn’t set to follow a 1970s-style spiral, in part because firms have less pricing power and tight labor markets don’t necessarily ignite wages.

For an overall economic recovery, science will ultimately be the key.

High inoculation rates are allowing advanced-world governments to resist another round of shutdowns, opting instead for targeted measures that include vaccination requirements for public places such as restaurants.

Meanwhile, emerging markets could be worse off: Manufacturing and tourism-led economies like Vietnam and Thailand have already been forced to close factories and turn away visitors.

That’s why wealthy countries could face mounting pressure to divert vaccines to lower-income regions. A new analysis shows they’ll likely have about 1.2 billion extra doses available by the end of the year.

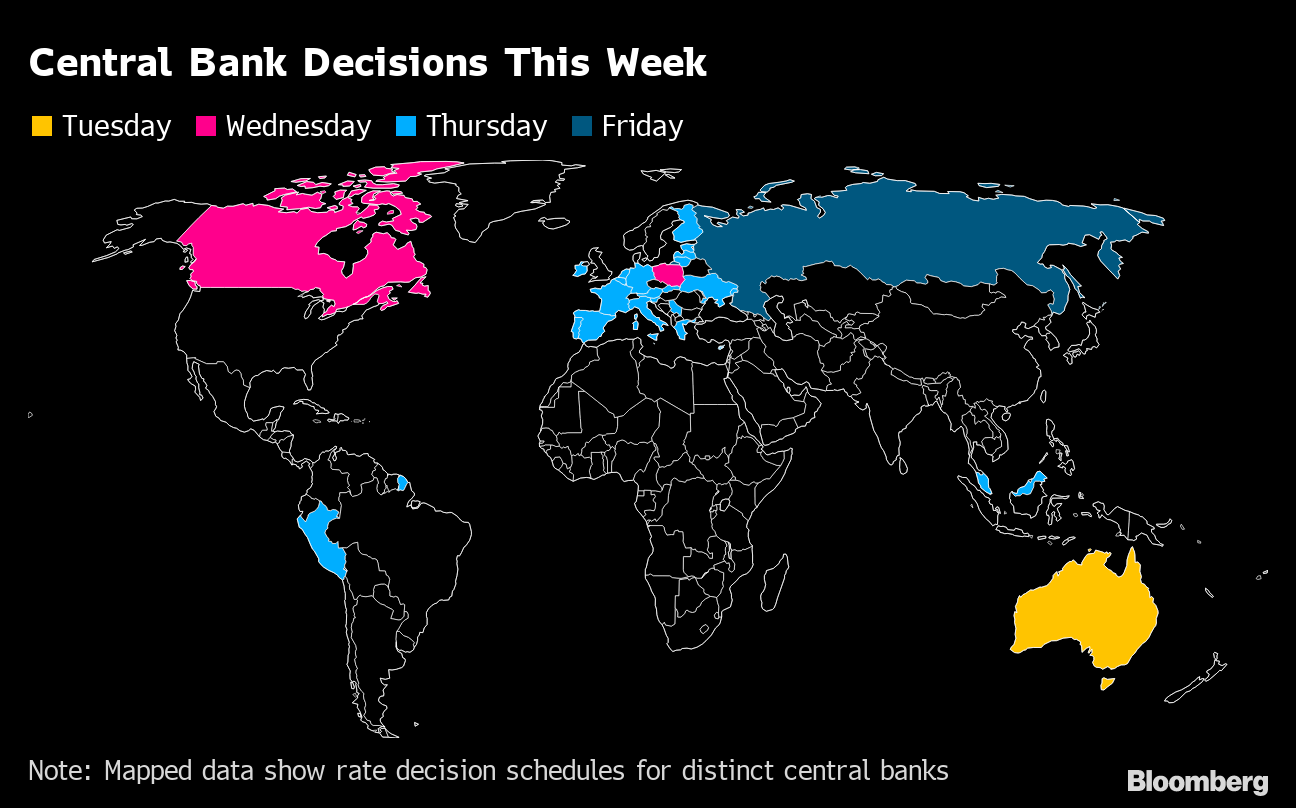

Note: Mapped data show rate decision schedules for distinct central banks

.chart-js display: none;

The European Central Bank will decide this week if it should dare to dial down emergency stimulus while the pandemic still menaces the euro-zone economy.

The threat posed by the delta variant of the coronavirus could yet embolden policy makers on Thursday to keep up the “significantly higher” pace of bond purchases they adopted earlier this year. But advanced vaccination rates, a robust rebound and inflation that is already at the fastest in a decade are all reasons to consider a downward shift in gears.

Elsewhere, at least eight other central banks globally are due to deliver monetary decisions, including Australia and Canada. While most are likely to keep their stance unchanged, Russia and Ukraine could deliver interest-rate increases.

Click on the blue links to read any of the stories in full:

Joblessness nightmare | For millions of Americans, the Labor Day weekend brings the end of federally funded emergency unemployment benefits and a lurch into the uncertain economic recovery.

Income redistribution | China’s push for “common prosperity” is not just about taxing the rich but also directing resources into rural areas and to those on lower incomes, according to one of the country’s most prominent experts studying wage inequality.

UAE trade | The United Arab Emirates plans to deepen its trade ties in fast-growing economies in Asia and Africa, and draw $150 billion in foreign investment from mainly older partners to reposition itself as a global hub for business and finance.

U.K. choices | Chancellor Rishi Sunak is facing five crucial fiscal decisions — including whether to deliver the biggest overnight welfare-benefit cut in history and the largest state pension increase in 30 years, according to the Resolution Foundation think tank.

German ship demand | Factory orders in Europe’s biggest ecnomy unexpectedly rose in July, driven by a surge in export demand for ships.

Taper debate | Australia’s central bankers are set to revisit the question of whether to delay a planned taper of bond purchases as a worsening outbreak of the delta variant dims economic prospects.

Need-to-Know Research

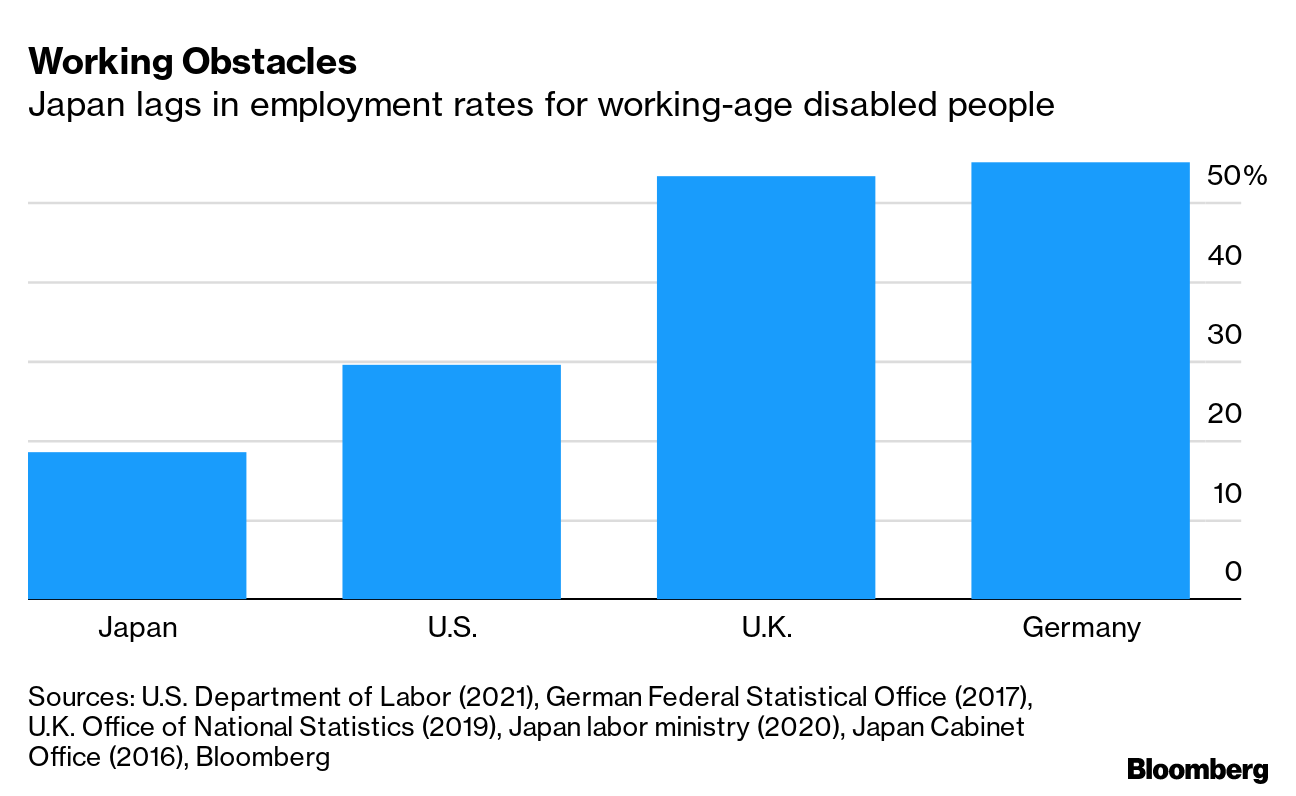

Working Obstacles

Japan lags in employment rates for working-age disabled people

Sources: U.S. Department of Labor (2021), German Federal Statistical Office (2017), U.K. Office of National Statistics (2019), Japan labor ministry (2020), Japan Cabinet Office (2016), Bloomberg

.chart-js display: none;

Paralympics host Japan’s track record for integrating people with disabilities into the workforce lags many of its peers. The proportion of working-age disabled people with a job there is around 19%, based on a Bloomberg calculation, compared with 30% in the U.S.

Disappointment over the U.S. August jobs report is all but certain to push Federal Reserve policy makers to delay considering a move to scale back asset purchases at their Sept. 21-22 meeting.

Bloomberg New Economy Conversations — China’s Tech Crackdown: Join New Economy Forum Editorial Director Andrew Browne on Sept. 8 as he analyzes the sweeping regulatory crackdown underway in China. The private sector helped power China’s economic rise, but President Xi Jinping seems determined to rein in what he sees as its excesses. Is this transitory or a game-changing shift? Joining Andy are Keyu Jin, Associate Professor of Economics at the London School of Economics & Political Science, and Kevin Rudd, President and Chief Executive Officer of the Asia Society. Register here.

OTTAWA – The Canadian economy was flat in August as high interest rates continued to weigh on consumers and businesses, while a preliminary estimate suggests it grew at an annualized rate of one per cent in the third quarter.

Statistics Canada’s gross domestic product report Thursday says growth in services-producing industries in August were offset by declines in goods-producing industries.

The manufacturing sector was the largest drag on the economy, followed by utilities, wholesale and trade and transportation and warehousing.

The report noted shutdowns at Canada’s two largest railways contributed to a decline in transportation and warehousing.

A preliminary estimate for September suggests real gross domestic product grew by 0.3 per cent.

Statistics Canada’s estimate for the third quarter is weaker than the Bank of Canada’s projection of 1.5 per cent annualized growth.

The latest economic figures suggest ongoing weakness in the Canadian economy, giving the central bank room to continue cutting interest rates.

But the size of that cut is still uncertain, with lots more data to come on inflation and the economy before the Bank of Canada’s next rate decision on Dec. 11.

“We don’t think this will ring any alarm bells for the (Bank of Canada) but it puts more emphasis on their fears around a weakening economy,” TD economist Marc Ercolao wrote.

The central bank has acknowledged repeatedly the economy is weak and that growth needs to pick back up.

Last week, the Bank of Canada delivered a half-percentage point interest rate cut in response to inflation returning to its two per cent target.

Governor Tiff Macklem wouldn’t say whether the central bank will follow up with another jumbo cut in December and instead said the central bank will take interest rate decisions one a time based on incoming economic data.

The central bank is expecting economic growth to rebound next year as rate cuts filter through the economy.

This report by The Canadian Press was first published Oct. 31, 2024