The surging coronavirus is stoking fears of a fresh downturn for the world economy, heaping pressure on central banks and governments to lay aside other concerns and do more to spur demand.

Hopes are mounting that COVID-19 vaccines will become available as soon as December, but widespread delivery will take months and infections are rising again in many large economies. Authorities are responding with more restrictions to limit the virus’s spread at the price of weaker economic activity.

Wall Street economists now say that it wouldn’t take much for the U.S., euro area and Japan to each contract again either this quarter or next, just months after they bounced from the deepest recession in generations. Bloomberg Economics guages of high-frequency data point to a double-dip downturn, with European factory indexes on Monday justifying that worry, though a U.S. measure of business activity was upbeat.

That leaves policy makers hearing calls for more stimulus, even when central banks are already stretched and starting to worry about froth in financial markets. Meantime, politicians from the U.S. to Europe are clashing over just how much they can and should do with fiscal policy.

“While there is much excitement over the progress of vaccine development, it will not be the quick fix that many expect it to be,” Singapore’s Trade & Industry Minister Chan Chun Sing told reporters on Monday. “Manufacturing enough doses, then distributing and vaccinating a significant population of the world, will take many months, if not years.”

Against such a backdrop, the European Central Bank is set to ease monetary policy again next month, while the Federal Reserve could concentrate more of its bond purchases on longer-term securities to push down interest rates.

But there are concerns the central banks have run out of room to act decisively and that even easier financial conditions won’t translate into an economic boost. The International Monetary Fund is among those also warning elevated asset prices potentially point to a disconnect from the real economy and so may pose a financial stability threat.

“There is a glut of savings and a shortage of investment,” which is the core problem facing developed economies, former Fed Chair Janet Yellen, who is set to be nominated for Treasury Secretary by President-elect Joe Biden, told Bloomberg’s New Economy Forum last week. “We have to have fiscal policy, structural policy other than just relying on central banks to achieve healthy growth.”

The problem is fiscal policy in the U.S. and Europe isn’t racing to the rescue. Lawmakers in the U.S. are at loggerheads over how much more to spend as Biden prepares to take office. President Donald Trump’s Treasury Department last week reduced the Fed’s ability to aid some credit markets.

In Europe, US$2 trillion in aid is being held up by a fight over political control.

“Exactly at the time central banks everywhere are acknowledging the centrality of fiscal policy in dealing with the economic consequences of the pandemic, governments are facing difficulties in implementing the next leg of their stimulus,” said Gilles Moec, chief economist at AXA SA.

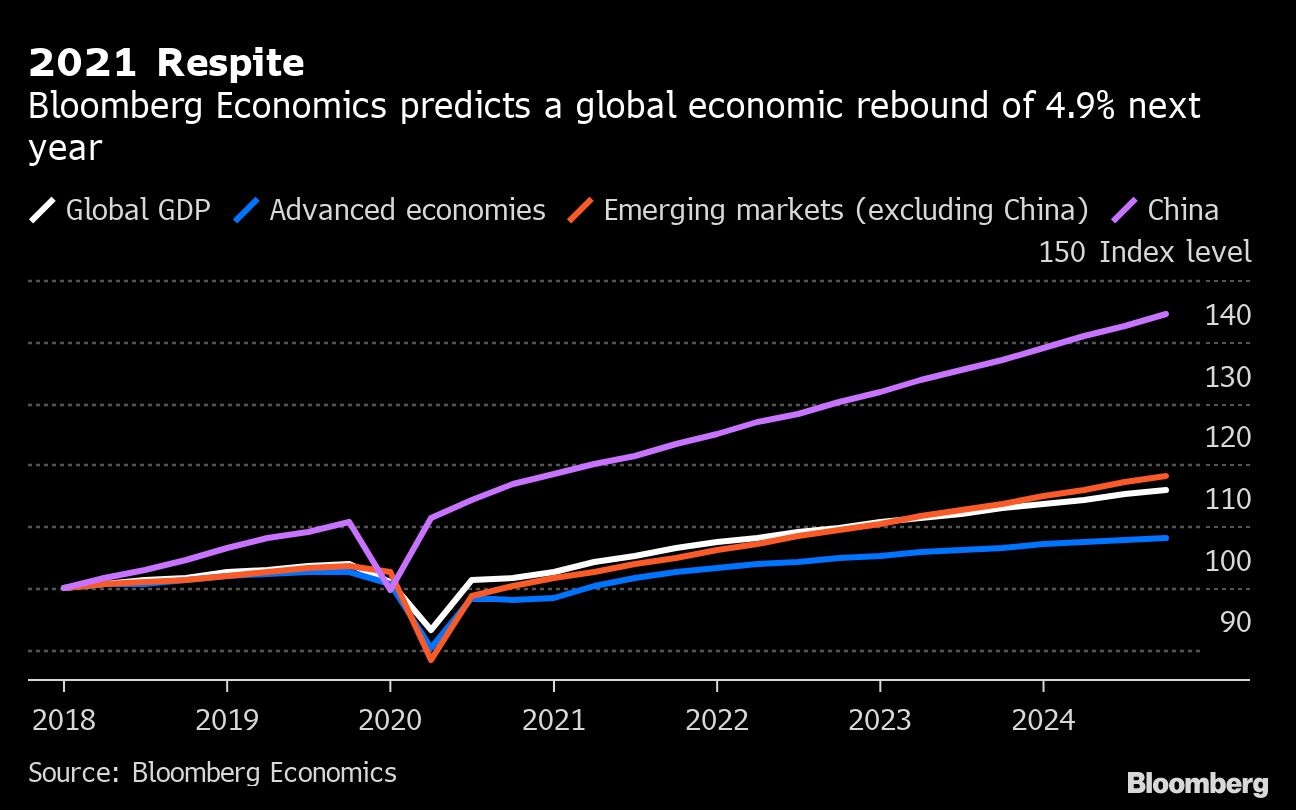

What Bloomberg Economics Says...

“Our base case is a contraction of 4.1 per cent in global output in 2020, followed by a rebound to 4.9 per cent growth in 2021. Uncertainty on the course of the virus, extent of stimulus, and timing of a vaccine mean the range of possible outcomes remains unusually wide.”

— Tom Orlik

For the U.S., the pace of infections prompted JPMorgan Chase & Co. analysts to forecast an economic shrinkage next quarter as various states impose social distancing curbs and some government benefits expire. Recent data show more people filing for unemployment benefits and fewer dining out at restaurants.

“It is possible we could have negative growth if this resurgence gets bad enough and mobility falls off enough,” Dallas Fed President Robert Kaplan told Bloomberg Television last week.

In Europe, further evidence arrived on Monday that a double-dip recession is on the way, with a survey of purchasing managers dropping sharply.

Japan’s manufacturing and service sectors worsened at a faster pace in November, early purchasing managers’ indexes showed, adding to concern over the strength of the recovery. Prime Minister Yoshihide Suga has called for a third extra budget to keep the economy on a growth path.

Both the International Monetary Fund and the Group of 20 — which comprises the world’s richest nations — warned during the G20’s meetings last weekend that the recovery is at risk of derailing despite positive news around vaccines buoying global stocks.

China is the world’s only major economy tipped to grow in 2020 as the government’s early control of the virus allowed lockdowns to be eased months ago. While its trade-led recovery is offering a boost to global commerce for now, even it’s vulnerable to the global outlook.

Reality Check

Fed Chair Jerome Powell and ECB President Christine Lagarde are among the central bankers warning against exuberance on news of successful vaccine trials.

The main reason for caution is the time needed to roll out shots for the world population to an extent enabling an end to growth-sapping movement restrictions. The announcement of a vaccine itself may drive market optimism, but doesn’t re-open economies for now.

“The vaccine gives more of a vision for what may be late next year, and what 2022 will look like, but not for the next six months,” ECB chief economist Philip Lane said in an interview with Les Echos. “The situation will not materially improve in the last weeks of 2020.”

The ECB’s downbeat tone on the immediate outlook is the backdrop to the likely arrival of a boost to the central bank’s 1.35 trillion-euro (US$1.6 trillion) emergency bond-buying program and its cheap bank loans. Policy makers meet on Dec. 10.

The worst affected sectors continue to shed jobs as companies warn on profits. Boeing Co. is almost doubling its planned job cuts while Adidas AG became one of the first consumer-goods companies in Europe to warn that renewed lockdowns will weigh on its earnings again and bring a swift end to a recent sales rebound.

The JPMorgan analysts are though hopeful that a vaccine and another round of fiscal support totaling US$1 trillion in the U.S. will be enough to deliver average growth of more than five per cent in the middle quarters of 2021. Even then, the virus’s legacies of record debt and elevated unemployment will endure.

Economists at ABN Amro Group NV however see mobility restrictions around the world lasting well into 2022.

“Only then can the global economy break into a growth spurt to make up the lost output versus trend growth,” analysts including chief economist Sandra Phlippen wrote in a report on Monday. “The vaccine is tantalizingly close, but still out of reach.”

OTTAWA – Canada’s unemployment rate held steady at 6.5 per cent last month as hiring remained weak across the economy.

Statistics Canada’s labour force survey on Friday said employment rose by a modest 15,000 jobs in October.

Business, building and support services saw the largest gain in employment.

Meanwhile, finance, insurance, real estate, rental and leasing experienced the largest decline.

Many economists see weakness in the job market continuing in the short term, before the Bank of Canada’s interest rate cuts spark a rebound in economic growth next year.

Despite ongoing softness in the labour market, however, strong wage growth has raged on in Canada. Average hourly wages in October grew 4.9 per cent from a year ago, reaching $35.76.

Friday’s report also shed some light on the financial health of households.

According to the agency, 28.8 per cent of Canadians aged 15 or older were living in a household that had difficulty meeting financial needs – like food and housing – in the previous four weeks.

That was down from 33.1 per cent in October 2023 and 35.5 per cent in October 2022, but still above the 20.4 per cent figure recorded in October 2020.

People living in a rented home were more likely to report difficulty meeting financial needs, with nearly four in 10 reporting that was the case.

That compares with just under a quarter of those living in an owned home by a household member.

Immigrants were also more likely to report facing financial strain last month, with about four out of 10 immigrants who landed in the last year doing so.

That compares with about three in 10 more established immigrants and one in four of people born in Canada.

This report by The Canadian Press was first published Nov. 8, 2024.

The Canadian Institute for Health Information says health-care spending in Canada is projected to reach a new high in 2024.

The annual report released Thursday says total health spending is expected to hit $372 billion, or $9,054 per Canadian.

CIHI’s national analysis predicts expenditures will rise by 5.7 per cent in 2024, compared to 4.5 per cent in 2023 and 1.7 per cent in 2022.

This year’s health spending is estimated to represent 12.4 per cent of Canada’s gross domestic product. Excluding two years of the pandemic, it would be the highest ratio in the country’s history.

While it’s not unusual for health expenditures to outpace economic growth, the report says this could be the case for the next several years due to Canada’s growing population and its aging demographic.

Canada’s per capita spending on health care in 2022 was among the highest in the world, but still less than countries such as the United States and Sweden.

The report notes that the Canadian dental and pharmacare plans could push health-care spending even further as more people who previously couldn’t afford these services start using them.

This report by The Canadian Press was first published Nov. 7, 2024.

Canadian Press health coverage receives support through a partnership with the Canadian Medical Association. CP is solely responsible for this content.

As Canadians wake up to news that Donald Trump will return to the White House, the president-elect’s protectionist stance is casting a spotlight on what effect his second term will have on Canada-U.S. economic ties.

Some Canadian business leaders have expressed worry over Trump’s promise to introduce a universal 10 per cent tariff on all American imports.

A Canadian Chamber of Commerce report released last month suggested those tariffs would shrink the Canadian economy, resulting in around $30 billion per year in economic costs.

More than 77 per cent of Canadian exports go to the U.S.

Canada’s manufacturing sector faces the biggest risk should Trump push forward on imposing broad tariffs, said Canadian Manufacturers and Exporters president and CEO Dennis Darby. He said the sector is the “most trade-exposed” within Canada.

“It’s in the U.S.’s best interest, it’s in our best interest, but most importantly for consumers across North America, that we’re able to trade goods, materials, ingredients, as we have under the trade agreements,” Darby said in an interview.

“It’s a more complex or complicated outcome than it would have been with the Democrats, but we’ve had to deal with this before and we’re going to do our best to deal with it again.”

American economists have also warned Trump’s plan could cause inflation and possibly a recession, which could have ripple effects in Canada.

It’s consumers who will ultimately feel the burden of any inflationary effect caused by broad tariffs, said Darby.

“A tariff tends to raise costs, and it ultimately raises prices, so that’s something that we have to be prepared for,” he said.

“It could tilt production mandates. A tariff makes goods more expensive, but on the same token, it also will make inputs for the U.S. more expensive.”

A report last month by TD economist Marc Ercolao said research shows a full-scale implementation of Trump’s tariff plan could lead to a near-five per cent reduction in Canadian export volumes to the U.S. by early-2027, relative to current baseline forecasts.

Retaliation by Canada would also increase costs for domestic producers, and push import volumes lower in the process.

“Slowing import activity mitigates some of the negative net trade impact on total GDP enough to avoid a technical recession, but still produces a period of extended stagnation through 2025 and 2026,” Ercolao said.

Since the Canada-United States-Mexico Agreement came into effect in 2020, trade between Canada and the U.S. has surged by 46 per cent, according to the Toronto Region Board of Trade.

With that deal is up for review in 2026, Canadian Chamber of Commerce president and CEO Candace Laing said the Canadian government “must collaborate effectively with the Trump administration to preserve and strengthen our bilateral economic partnership.”

“With an impressive $3.6 billion in daily trade, Canada and the United States are each other’s closest international partners. The secure and efficient flow of goods and people across our border … remains essential for the economies of both countries,” she said in a statement.

“By resisting tariffs and trade barriers that will only raise prices and hurt consumers in both countries, Canada and the United States can strengthen resilient cross-border supply chains that enhance our shared economic security.”

This report by The Canadian Press was first published Nov. 6, 2024.