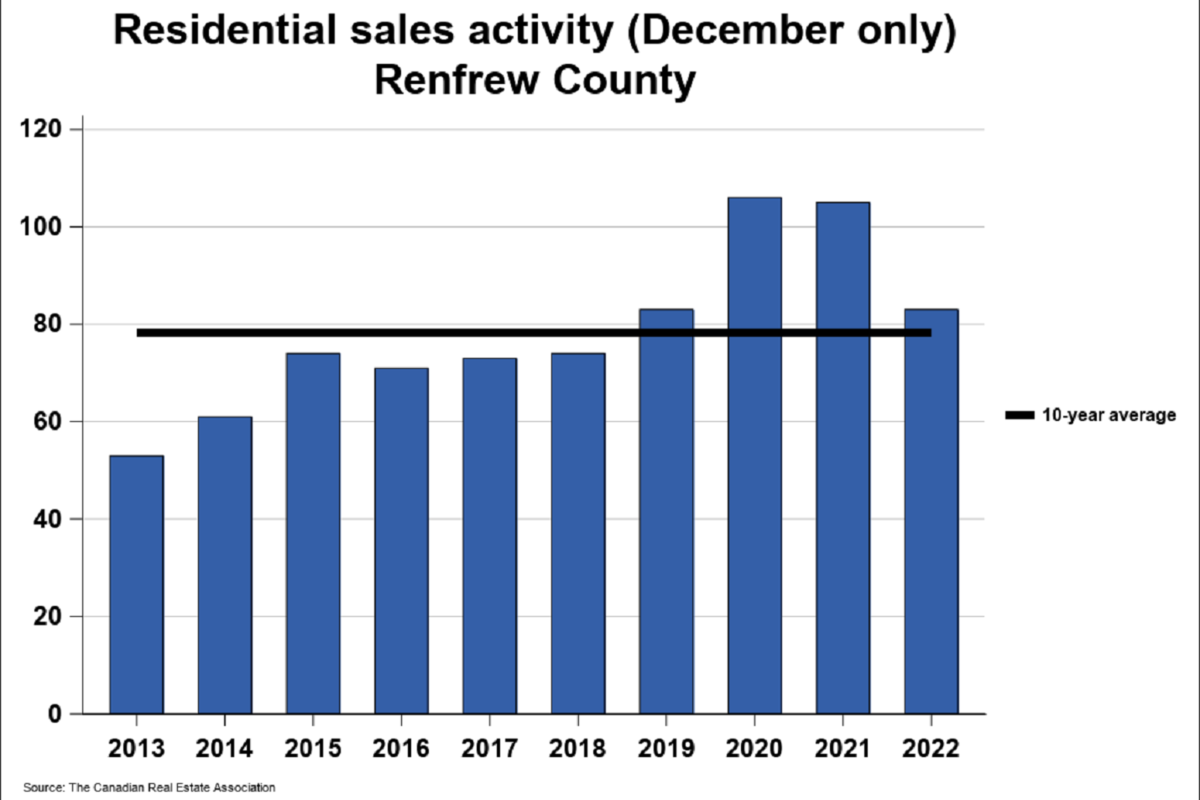

The ringing in of the new year did not bring good news to the real estate market in the Ottawa Valley as the trend of declining sales that dragged down the number of sales in 2022 continued in January with only 54 units sold in the first month of the year.

According to the newest report by the Renfrew County Real Estate Board, the 54 sales represented a decline of 48.1 per cent from January 2022. To put that number into perspective, home sales were 32 percent below the five-year average and 23.6 per cent below the 10-year average for the month of January.

One notable change from 2023 is in relation to the average sale price of a home actually declined in value compared to the numbers that were listed in 2022. The average price of homes sold in January 2023 was $421,111, down 14.2 per cent from January 2022.

This drop represents the first time in 13 months that a person selling a home in the Ottawa Valley did not see a significant profit in their final numbers. The dollar value of all home sales in January 2023 was $22.7 million, falling by 55.4 per cent from the same month in 2022.

Once again the Ottawa Valley went against the trend in terms of national real estate sales. National home sales declined by only three percent month-over-month in January compared to the 48.1 per cent registered.

Home sales recorded over Canadian MLS Systems edged back down three percent between December 2022 and January 2023, giving back all of December’s small gains and rejoining the mild downward trend observed since last summer.

Mild is definitely not a word to describe the conditions in the Ottawa Valley. The number of new listings was down by 10.5 per cent, or in real terms, 11 listings from January 2022. There were 94 new residential listings in January 2023.

This was the lowest number of new listings added in the month of January in more than three decades.

Comparatively, the actual number of national transactions in January 2023 came in 37 per cent below the second-best January ever in 2022. One trend that was similar to the national average were the January 2023 sales figure as the lowest for that month since 2009.

The stock and availability of new homes for sale is also down considerably making the choice of purchasing a home much harder for buyers. Not only are consumers still adjusting to the realities of limited supply, the average mortgage rate set by the Bank of Canada.

According to research from investment bank Keefe, Bruyette & Woods (KBW), with interest rates more than doubling in a year, many Canadians no longer qualify for pricier mortgages. Lenders are required to stress test borrowers to determine whether they can sustain payments at higher interest rates. That pressure is weighing on home buying.

Economists broadly expect that the Bank of Canada will hold off on rate cuts until the end of 2023 at the earliest, suggesting that mortgage headwinds won’t ease until next year, according to KBW analyst Mike Rizvanovic.

All these factors, combined with the newest January numbers, paint a continuation of bleak numbers for the Ottawa Valley. This is true in the area of new listings. They were 20.5 percent below the five-year average and 42.1 per cent below the 10-year average for the month of January.

Despite all the doom and gloom, there was a bit of good news contained in the most recent report. Active residential listings numbered 219 units on the market at the end of January, more than double the levels from a year earlier, jumping 133 per cent from the end of January 2022.

Active listings were 24.1 per cent below the five-year average and 59.2 per cent below the 10-year average for the month of January.

Months of inventory numbered 4.1 at the end of January 2023, up from the 0.9 months recorded at the end of January 2022 and below the long-run average of 8.5 months for this time of year. The number of months of inventory is the number of months it would take to sell current inventories at the current rate of sales activity.