VANCOUVER —

With B.C. facing a multi-billion-dollar deficit because of the COVID-19 pandemic, the premier and finance minister announced Thursday how the provincial government will spend $1.5 billion to help the economy recover.

In a news conference, John Horgan and Carole James explained the government’s plan to divide the recovery funding that was set aside in the province’s $8.25 billion pandemic response.

CTVNewsVancouver.ca is streaming the news conference LIVE NOW.

“Lives have been saved because of the sacrifices of British Columbians,” Horgan said Thursday.

“The pandemic continues to challenge us in unprecedented ways, but fundamental priorities remain the same. We need to protect people’s health, we need to keep the economy open safely and we need to support communities.”

Horgan said the economic recovery plan was built based on consultation with individuals, groups and communities.

“There was no government that had a playbook for how to deal with a global pandemic,” he said. “And when you’re building a plan for people, you have to talk to them.”

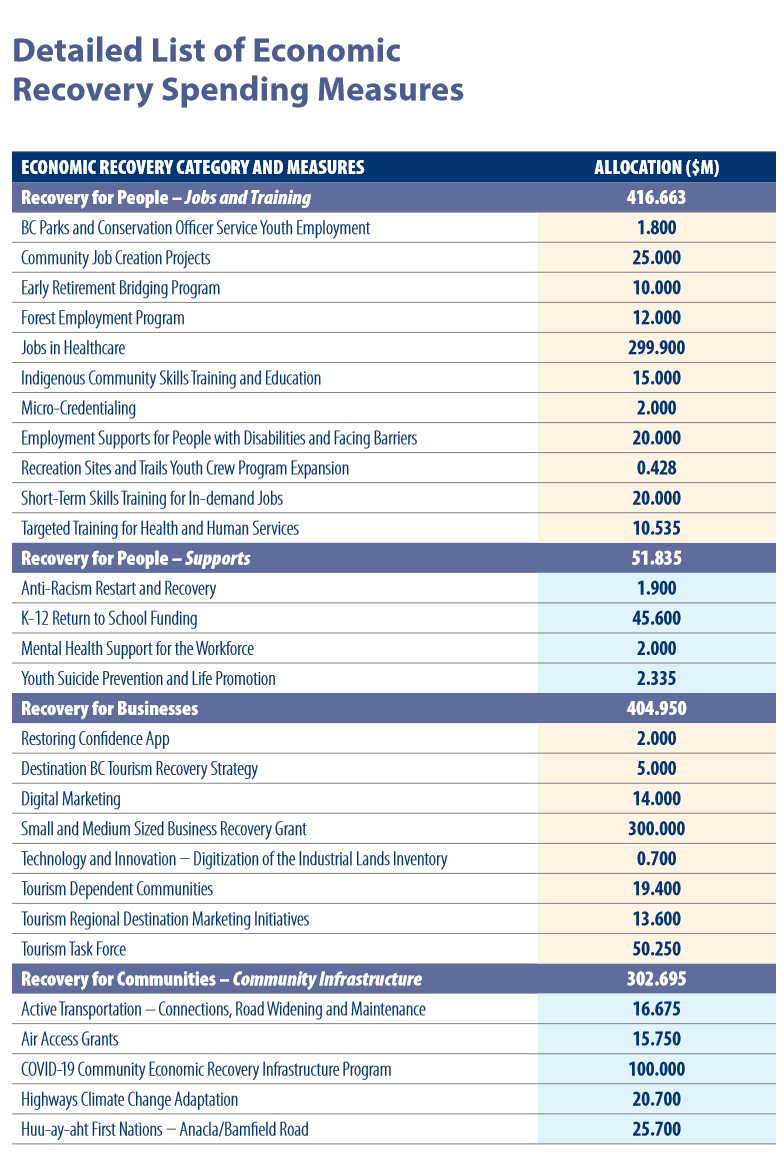

Some of the funds – about $400 million of it – is earmarked to help businesses recover with initiatives that include recovery grants for small and medium-sized businesses and a tourism task force. That task force will come up with recommendations on how tourism in B.C. can prepare for the 2021 season.

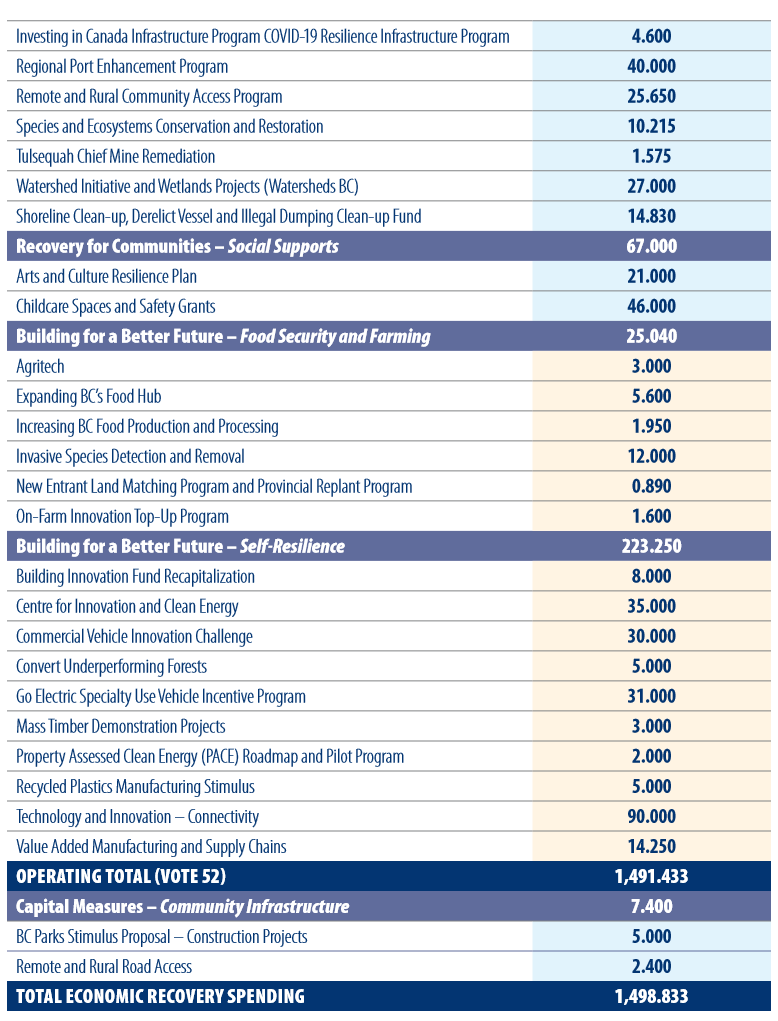

About $375 million will be distributed to communities to help local governments provide services and complete some infrastructure, like projects that are shovel-ready and initiatives to improve active transportation.

“The safe restart funds will help us address local challenges that have been made worse by COVID-19,” Horgan said.

More than $460 million is set aside for “recovery for people,” the finance ministry says, which includes previously announced funding for more health-care jobs and skills training.

The remaining $250 million is set aside for “building a better future,” which includes funding for clean energy innovation, recycled plastics manufacturing and some supports for the forestry industry.

The finance ministry also announced new tax recovery measures, totalling $660 million outside the $1.5 billion. More than a third of that covers a PST rebate for some businesses looking to invest in machinery, while the remainder is an employment incentive to encourage businesses to increase their payrolls.

Last week, James revealed that, because of COVID-19, B.C. is on track to see a $12.8-billion deficit this fiscal year.

“Our recovery, of course, will not happen overnight,” Horgan said.

“There’s a long road ahead of us and it will require a constant opportunity for us to adapt and innovate to changing circumstances.”

This is a developing story. Check back for updates.

Graphics from the Government of British Columbia