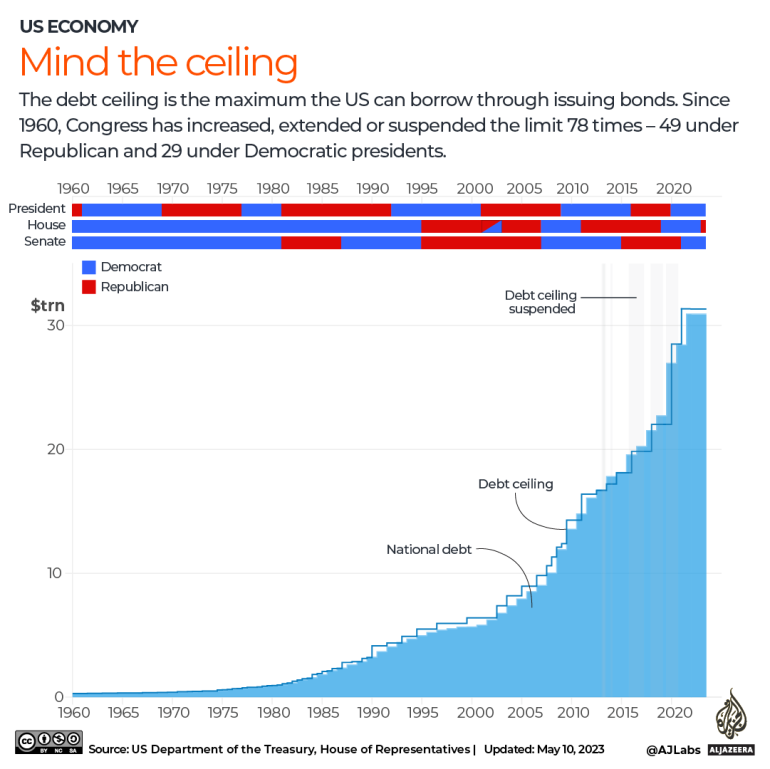

As a game of chicken plays out in Washington, DC, over whether to raise the limit on US government borrowing to avoid a default on its debt, the one thing that experts agree on is that a default would be catastrophic.

The United States hit its borrowing limit on January 19. Since then, the US Treasury has implemented a number of measures to avoid a default, but it is only a matter of days, or weeks at most, before those are exhausted and the US government is unable to pay what it owes.

Here’s an explainer on what happens if this unprecedented event takes place.

What are the chances that the US will indeed default?

No one really knows because it is “a political issue”, Lawrence J White, an economics professor at the Stern School of Business at New York University, told Al Jazeera.

“I keep hoping there will be a resolution, but this is a game of chicken, and usually somebody swerves and a head-on collision is avoided… but sometimes people go over the cliff, and that is the big worry,” he said.

To avoid a default, Congress would have to lift the debt ceiling, but Republicans are demanding spending cuts to do so. President Joe Biden, a Democrat, wants a simple vote in Congress that would only deal with raising the government’s debt limit.

Worry about the deadlock has amplified in the past few days as the so-called X-date – when the Treasury would run out of money to pay its bills – has moved up from mid-August to as early as June 1 on account of low tax collections in April, Bernard Yaros, assistant director at Moody’s Analytics, told Al Jazeera.

If the Treasury can limp along until mid-June, Yaros said, it will have a “surge” in tax receipts from businesses and individuals and close to $150bn in new extraordinary measures that will help it keep money flowing through late July or even early August.

But it is not clear it will get that breathing room.

What is the worst-case scenario?

The US goes into a weeks-long default with Republicans and Democrats digging in their heels.

Such a situation would be “a cataclysmic scenario” and be followed by a recession of the order of the financial crisis of 2008, Yaros said.

In such a scenario, the federal government would have to immediately slash its outlays and cut government spending.

As these cuts worked their way through the economy, “the hit to growth would be overwhelming,” Yaros and several Moody’s colleagues said in an analysis published in March.

Apart from this, financial markets would be in turmoil, interest rates would spike further and the strength of the dollar would decline, White said.

If the political deadlock drags out, interest rates will go even higher, dissuading people from borrowing or investing, White said.

“This will be echoed around the world,” he said. “This is not a good thing for anybody.”

A short breach

Even if the US were to fail to meet its obligations for only a number of days, there would still be consequences for the economy.

“The world will say we can’t rely on the US Treasury as much as we used to, and that will make people more reluctant to hold Treasury obligations,” White said.

“Interest rates for Treasury bills and bonds will go up and that will ultimately lead to a bigger tax burden for Americans.”

It could also fuel calls for alternatives to the US dollar, which for decades has been the unparalleled currency in international finance.

While it is unclear if credit rating agencies would downgrade Treasury debt if it fails to meet its obligations, any downgrade would set off a cascade of credit implications and downgrades on the debt of many other financial institutions, non-financial corporations, municipalities, infrastructure providers, structured finance transactions and other debt issuers, Moody’s has warned.

Those institutions that are backstopped by the US government – including mortgage financiers Fannie Mae, Freddie Mac and the Federal Home Loan Bank – would likely suffer the biggest downgrades to their ratings.

“Despite lawmakers’ quick reversal in this scenario and our assumption that the rating agencies do not engage in downgrades, significant damage will have already been done,” Moody’s said.

“The fact that we haven’t even solved this position by now is not a good thing,” White said.